You might be staring at a fixed asset register, a trial balance, or an AAT practice question and thinking the same thing many trainees think...

That matters in the roles many trainees want most. A bookkeeper may need to separate cash received from revenue earned. An accounts assistant may need to post deferred income correctly before month end. A business analyst may need to understand why reported revenue moved even when sales invoices looked strong. A data analyst may need to build reports that show contract liabilities, recognised income, and delivery progress side by side.

IFRS 15 can look technical when you first meet it. In practice, it gives you a clean way to think. What did the business promise. How much is the customer paying. When does the customer get control of each part. Once you learn to answer those questions, revenue recognition becomes far less mysterious.

Your First Step in Modern Financial Reporting

You’re in your first finance role. A client has bought a year-long package that includes advanced payroll training, ongoing bookkeeping support, and final accounts preparation. The fee has been agreed, the invoice has been raised, and the cash may even have been received.

Then comes the real question. How much revenue belongs in this month’s profit and loss account?

If you post the full amount on day one, you could overstate income. If you spread it evenly without reading the contract, you could still be wrong. Payroll training may be delivered over a short period. Bookkeeping support may be delivered month by month. Final accounts work may only be complete near the year end. The timing matters because the customer doesn’t receive everything at once.

This is the gap IFRS 15 fills. It gives finance staff a structured way to decide when revenue is earned, rather than guessing based on invoicing or cash collection. If you want a simple supporting explanation of revenue recognition in a specialist context, Alignmint’s guide to tracking nonprofit revenue is a useful extra read because it reinforces the same core idea. Revenue follows delivery, not just payment.

Why trainees get stuck

Most confusion starts with one habit. People look at the invoice before they look at the promise.

In training businesses and service firms, a single invoice can include several different services. The customer may pay upfront, but that doesn’t mean the business has delivered everything upfront. That’s why trainees need to think beyond bookkeeping entries and into contract terms.

Practical rule: Cash received answers one question. Revenue recognised answers another.

A good starting point is understanding where IFRS 15 sits within the wider reporting framework. If you need that bigger picture, this guide to financial reporting standards helps place revenue recognition inside the broader set of rules you’ll use in practice.

What this means in real jobs

In UK service-based roles, IFRS 15 shows up in everyday tasks such as:

- Month-end postings: moving part of an upfront invoice into deferred income.

- Final accounts work: checking whether income has been recognised in the right period.

- Management reporting: explaining why cash and revenue don’t match.

- Contract review: spotting that one package contains several separate promises.

- Data reporting: building schedules that track delivery against billing.

That’s why this standard matters so much early in your career. It isn’t just for technical accountants. It shapes the numbers that bookkeepers, payroll staff, accounts assistants, and analysts work with every day.

What is IFRS 15 and Who Does It Affect

IFRS 15 Revenue from Contracts with Customers was issued in May 2014 and became mandatory for UK entities for annual periods starting on or after 1 January 2018. It replaced older standards including IAS 18, and a 2017 survey by the UK’s Financial Reporting Council found that 68% of FTSE 350 companies expected a material change in the timing or amount of revenue recognised under the new rules, as noted on the IFRS 15 standard page.

Before IFRS 15, similar transactions could be treated differently. That made financial statements harder to compare. One business might recognise income earlier. Another might wait. The standard introduced a single model based on a core principle: recognise revenue when control of goods or services transfers to the customer.

What control means in plain English

Control doesn’t just mean legal ownership. In service work, it often means the customer has received the benefit of what was promised.

If a firm provides weekly bookkeeping support, the customer may consume that service as it is delivered. If a consultant writes a final report that only becomes useful when handed over at the end, control may transfer later. This is why two contracts with the same total fee can lead to very different timing of revenue.

The key question isn’t “Have we billed it?” It’s “Has the customer received the promised value yet?”

Who needs to understand it

This standard affects far more people than statutory accounts teams.

| Role | Why IFRS 15 matters |

|---|---|

| Accounts assistant | You may prepare journals for deferred and recognised income |

| Bookkeeper | You’ll often reconcile invoices, cash, and revenue timing |

| Payroll trainee | Training or support contracts can include multiple service elements |

| Final accounts staff | Cut-off and income recognition affect year-end accuracy |

| Business analyst | Reported revenue trends may reflect timing rules, not just sales activity |

| Data analyst | Revenue dashboards need delivery data, not invoice totals alone |

Where it appears in service businesses

In UK service-based organisations, IFRS 15 often affects:

- Training packages: classroom sessions, software certification, and coaching sold together

- Software implementation work: setup, migration, and user training in one contract

- Professional services: ongoing support plus one-off deliverables

- Flexible contracts: upgrades, add-ons, and discounts agreed after the original deal

For trainees, that’s why IFRS 15 is a practical skill. It helps you read contracts properly, question timing, and produce accounts that reflect what has really been delivered.

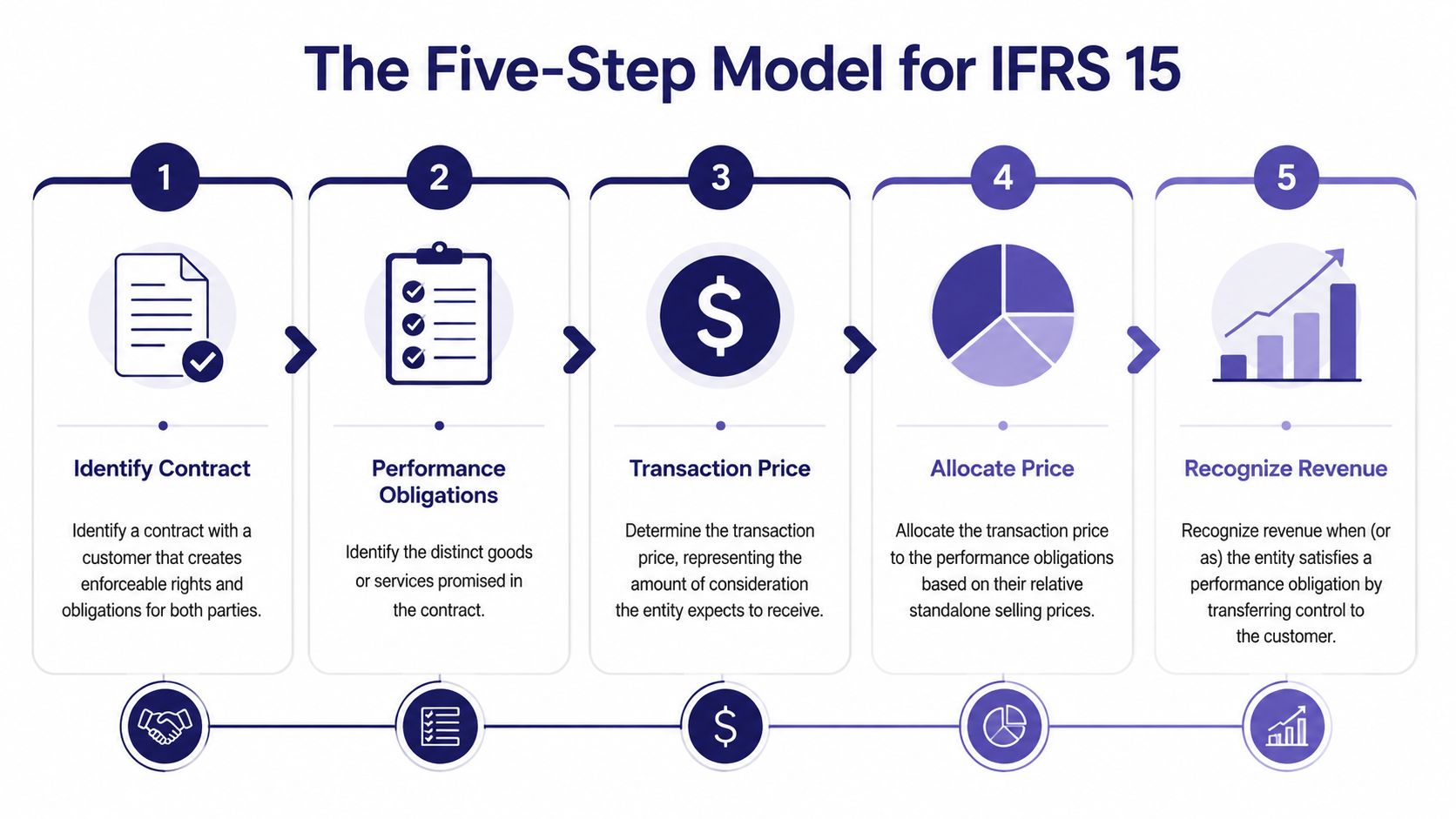

The Five-Step Model for Revenue Recognition

At the centre of ifrs 15 revenue recognition is a five-step model. It sounds formal, but it’s a practical checklist. If you can apply it calmly, you can work through most service contracts without getting lost.

Think of a company hiring a data analyst to build a custom sales dashboard. The agreement includes data cleansing, dashboard design, and a short training session for staff. One contract. Several promises.

Step 1 Identify the contract

Start with the agreement itself. You need clear evidence that both parties have approved it, that the rights and payment terms can be identified, and that the arrangement has commercial substance.

For trainees, this usually means reading more than the invoice. Check the proposal, signed order, engagement letter, or service agreement. The contract tells you what the business has promised.

Step 2 Identify the performance obligations

A performance obligation is a distinct promised good or service.

In the dashboard example, the business may have promised:

- Data cleansing

- Dashboard build

- Staff training

If those parts are distinct, they need to be considered separately. A common pitfall is treating a single invoice as a single service, even when the contract contains several separate deliverables.

Step 3 Determine the transaction price

This is the amount the business expects to receive.

Sometimes it’s simple. A fixed fee with no discounts or bonuses. Sometimes it’s less tidy. A contract may include a rebate, a success fee, or a reduction if the customer buys extra services later. When the price can change, you need judgement.

Step 4 Allocate the transaction price

Once you know the total price, you allocate it across the distinct performance obligations.

That means the dashboard fee isn’t automatically recognised in one block. Part belongs to cleansing, part to the build, and part to training. The split should reflect the stand-alone selling price of each promised element.

Memory aid: First split the contract into promises. Then split the price into those same promises.

Step 5 Recognise revenue when or as each obligation is satisfied

Timing now plays a role.

Some services are recognised over time because the customer receives and uses the benefit as the work is done. Others are recognised at a point in time because the customer only gains control when the work is completed and handed over.

For our example:

| Step | Question to ask | Dashboard example |

|---|---|---|

| 1 | Is there a valid contract | Signed analytics project agreement |

| 2 | What are we promising | Cleansing, build, training |

| 3 | What’s the total price | Agreed project fee |

| 4 | How should we split it | Allocate based on stand-alone values |

| 5 | When is each part delivered | Over time or on completion depending on the service |

Why the model works

The strength of the model is that it stops rushed assumptions.

A trainee who follows the five steps is less likely to post all income on invoice date. You’re also more likely to spot missing documentation, bundled services, and timing issues that affect month-end and year-end reporting.

When it comes to final accounts work, this model improves cut-off. For business analysis, it explains why revenue patterns don’t always follow billing patterns. For data analysis, it gives you a structure for reporting contract assets, liabilities, and recognised income in a cleaner way.

Applying IFRS 15 with Practical Examples

Theory only helps when you can turn it into entries and schedules. Two examples make this easier. One is a bundled training package. The other is a service project delivered over several months.

A useful technical benchmark for the first example comes from a training-style bundle discussed in this IFRS 15 overview. It shows that where stand-alone selling prices are £3,500 for training, £1,000 for certification, and £500 for coaching, a £5,000 bundle is allocated proportionally. The same source notes that a 2023 ACCA Global study found 68% of UK firms adjusted deferred revenue upwards by 15-25% after implementing IFRS 15 because unbundling changed the timing of income.

Example one bundled training package

A customer buys a single package for £5,000. It includes:

- Training

- Software certification

- Career coaching

The stand-alone selling prices are:

- Training: £3,500

- Certification: £1,000

- Coaching: £500

The total of the stand-alone prices is also £5,000, so in this example the allocation is straightforward:

| Service | Stand-alone selling price | Allocation |

|---|---|---|

| Training | £3,500 | £3,500 |

| Certification | £1,000 | £1,000 |

| Coaching | £500 | £500 |

The accounting point is simple. You don’t recognise the full £5,000 as revenue on the day the invoice is sent if the services are delivered later.

If the customer pays upfront, the first entry is often:

| Date | Account | Debit (£) | Credit (£) |

|---|---|---|---|

| Contract start | Bank | 5,000 | |

| Contract start | Deferred revenue | 5,000 |

As each service is delivered, you release the relevant amount from deferred revenue into income.

Journal Entries for Bundled Training Package Example

| Date | Account | Debit (£) | Credit (£) |

|---|---|---|---|

| Contract start | Bank | 5,000 | |

| Contract start | Deferred revenue | 5,000 | |

| As training is delivered | Deferred revenue | 3,500 | |

| As training is delivered | Revenue | 3,500 | |

| On certification completion | Deferred revenue | 1,000 | |

| On certification completion | Revenue | 1,000 | |

| When coaching is delivered | Deferred revenue | 500 | |

| When coaching is delivered | Revenue | 500 |

If the training runs over time, you wouldn’t release the full £3,500 at once. You’d recognise it as the training is delivered. Certification may be recognised when completed. Coaching may be recognised when the sessions are provided.

That’s the practical shift many trainees need to absorb. One invoice doesn’t mean one timing pattern.

For a wider grounding in how these entries feed into year-end work, this guide on preparing financial statements is worth reviewing alongside your revenue schedules.

Example two service project over time or at a point in time

Now take a business analyst contract. A client hires a firm to deliver a process improvement report over three months. The work includes reviewing current systems, interviewing staff, analysing workflow data, and producing recommendations.

The key judgement is timing. Should revenue be recognised across the three months, or only when the final report is delivered?

A practical way to think about it is this:

- If the customer receives and uses the benefit as the work is performed, over time may be right.

- If the customer only gains control when the final report is complete and transferred, point in time may be right.

If you can’t explain why revenue belongs in this month using the contract and delivery evidence, don’t post it yet.

In a monthly management accounts setting, this matters a lot. Suppose the team has completed review meetings and a large part of the analysis in month one and month two, but the final report is only signed off in month three. The business needs to decide whether those earlier activities satisfy a performance obligation over time or represent work leading to a final transfer.

What trainees should look for

When judging this type of service contract, check:

- The wording of the deliverable: is the promise a final report, or an ongoing advisory service?

- Customer benefit during delivery: can the client use the work as it is produced?

- Evidence of progress: timesheets, milestones, review notes, and acceptance points

- Management accounts impact: recognised revenue affects monthly profit, accrued income, and deferred balances

Accounts staff and analysts often collaborate. The accounting answer depends on contract terms, but the evidence often sits in operational data.

Handling Contract Modifications and Variable Consideration

Contracts rarely stay still. A client may add extra bookkeeping support, ask for advanced payroll training halfway through the year, or negotiate a discount linked to outcomes. Once that happens, the original revenue plan may no longer be right.

A useful UK-specific point comes from this review of IFRS 15 implementation, which reports a 22% increase in disclosed revenue judgements in FTSE 250 financial statements from 2019 to 2023. The same source says a BDO UK study found 41% of service firms reclassified long-term training contracts from point-in-time to over-time recognition after IFRS 15. That tells you where much of the difficulty sits. Timing and judgement.

When a contract changes

A contract modification happens when the parties approve a change in scope, price, or both.

Take a bookkeeping client on a standard support package. Midway through the contract, they add an advanced payroll service. You need to ask whether that extra work is distinct from the original contract and whether the extra price reflects a stand-alone selling price.

If the added service is separate and priced appropriately, it may be treated like a new contract. If not, you may need to revise the accounting for the existing arrangement.

Here’s the practical risk for trainees. If you keep using the old schedule after the contract changes, your recognised revenue can drift away from the actual service pattern.

Variable consideration in simple terms

Variable consideration means the final price isn’t fixed with certainty. Common examples include:

- Performance bonuses

- Volume discounts

- Refunds or rebates

- Price reductions linked to service levels

You cannot include every possible extra amount in revenue from day one. You need to consider whether the estimate is reliable enough and whether recognising it now could later lead to a reversal.

That’s why finance teams often stay cautious. It’s better to recognise revenue when the amount is supportable than to post an optimistic figure and reverse it later.

A short explainer can help reinforce the judgement involved:

Practical checks before posting revenue

When a contract has changed or includes a variable amount, pause and review:

-

What exactly changed

Read the revised agreement, emails, and approvals. -

Is the new service distinct

Decide whether it stands on its own or changes the original promise. -

Has the transaction price changed

Update your revenue schedule, not just the invoice total. -

Could the amount reverse later

If yes, be careful about recognising it too early.

Working habit: Keep one live revenue schedule per contract. Update it every time scope, price, or delivery timing changes.

This is one of the biggest differences between mechanical bookkeeping and stronger finance work. Strong trainees don’t just post what’s on the invoice. They ask whether the accounting still matches the contract.

Common IFRS 15 Pitfalls and How to Avoid Them

Most IFRS 15 mistakes don’t happen because the standard is impossible. They happen because people move too fast, trust the invoice too much, or skip the contract review.

One warning sign comes from a reported 2025 UK ICAEW survey of 1,200 SMEs, which found that 68% struggle with Step 4, the allocation of transaction price, and that this contributes to a 22% revenue misstatement risk and can inflate deferred revenue by up to 15% per quarter, according to this summary of SME implementation issues. For trainees, that tells you where to be extra careful. Bundled services.

Pitfall one treating one package as one promise

A package may include training, software setup, support, and coaching. If you treat all of that as one obligation without checking whether the parts are distinct, you can recognise revenue too early or too late.

How to avoid it: break the contract into each promised service before posting anything.

Pitfall two using invoice date as the revenue date

This is one of the most common errors in smaller businesses. The invoice gets raised, so the income gets posted in full.

How to avoid it: match revenue to delivery, not billing. Use deferred income where the service is still outstanding.

Pitfall three weak stand-alone selling price support

Teams sometimes know a bundle needs splitting but don’t document how they arrived at the allocation.

How to avoid it: keep evidence. Use normal list prices, recent sales of similar services, or documented pricing logic.

Pitfall four ignoring contract changes

If the customer adds services, delays delivery, or receives a discount, the original revenue schedule may no longer be valid.

How to avoid it: revisit the contract each time scope or price changes. Update journals prospectively where needed.

Pitfall five poor communication between teams

Operations may know the service hasn’t been delivered, but finance may still post income because the invoice is in the system.

How to avoid it: ask for delivery evidence. Timesheets, completion records, booking confirmations, and sign-off emails all matter.

Small revenue errors repeat quietly. By year end, they can become a big final accounts problem.

The good news is that these are teachable mistakes. If you build the habit of reading the contract, splitting obligations properly, and tracking delivery, you’ll avoid the errors that catch many early-career staff.

Your IFRS 15 Implementation Checklist for Trainees

When you review a new contract, don’t rely on memory. Use a checklist. It keeps your thinking clear and gives your manager an audit trail of your judgement.

A practical routine you can use

-

Read the full contract first

Check what was promised, how much the customer will pay, and when the services will be delivered. -

List each performance obligation

Separate training, bookkeeping support, payroll work, software setup, reporting, and coaching where they are distinct. -

Document stand-alone selling prices

Keep evidence of how each component was priced. -

Decide on timing

Ask whether each element is recognised over time or at a point in time. -

Build a revenue schedule

Track what has been billed, what has been recognised, and what remains deferred. -

Review modifications quickly

If the customer adds or removes services, update the schedule straight away. -

Watch for variable consideration

Be cautious with discounts, rebates, and bonus-related amounts. -

Check related standards where needed

If an accounting estimate or policy needs revision, this overview of International Accounting Standard 8 helps you think through changes in judgement and treatment.

The habit that matters most is simple. Don’t ask only whether money came in. Ask whether the promised service has been delivered.

If you want to build practical, job-ready confidence in revenue recognition, final accounts, bookkeeping, payroll, and finance systems, Professional Careers Training offers hands-on training with ACCA-qualified support, flexible study options, software exposure, and career coaching designed for trainees aiming to move into real UK finance roles.