The best job in the UK is not the one with the flashiest title. It is the one you can enter, build on, and turn...

If you’re training in bookkeeping, VAT, payroll support, final accounts, or moving into a business analyst or data analyst role, IAS 7 gives you a practical framework for understanding how cash moves through a business. It isn’t just for auditors or technical financial reporting teams. It shows up in real work: reconciling ledgers, reviewing payment runs, preparing year-end accounts, checking whether a business can meet payroll, and explaining trends in Xero or Sage reports.

A lot of trainees first meet IAS 7 as a rulebook. A better way to see it is as a translation tool. Profit can be affected by accruals, estimates, and timing. Cash is more immediate. A statement of cash flows helps you explain the gap between the two in a structured way that employers value.

Why Cash Flow Matters for Your Accounting Career

On your first day helping with month-end, you might open a draft cash flow statement and wonder why the company shows a profit but still seems short of cash. That confusion is normal. It’s also one of the reasons IAS 7 matters so much in real jobs.

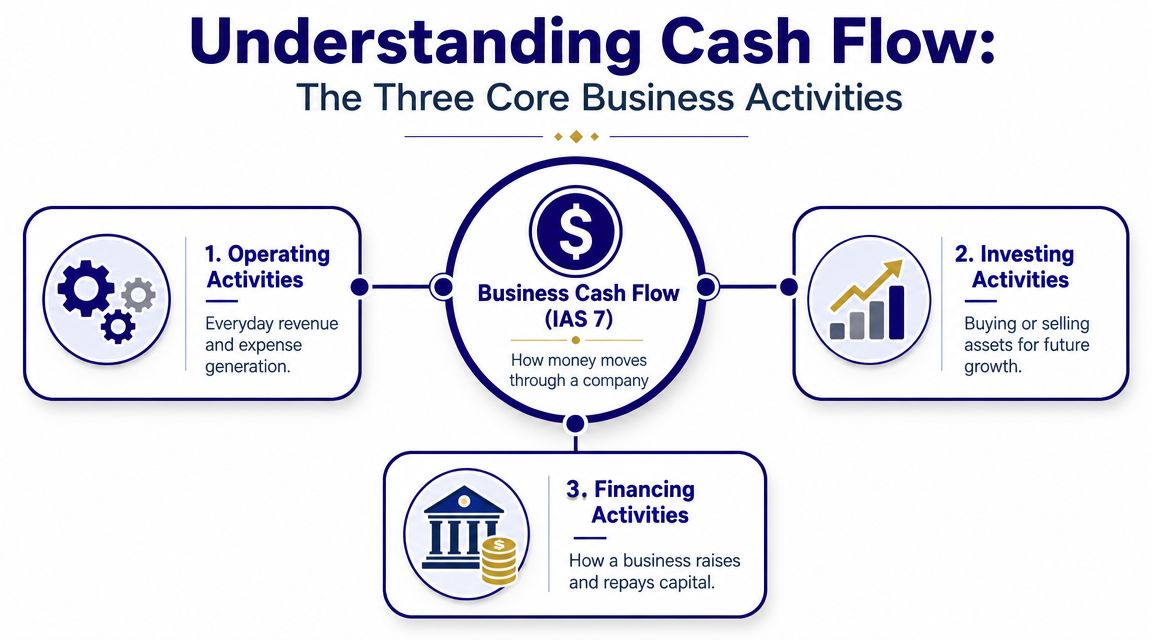

The standard has been part of IFRS reporting for a long time. The IFRS Foundation says IAS 7 was first issued in 1992 and later revised in 1994, 1998, 2004, and 2016, and it requires cash flows to be classified into exactly three activities: operating, investing, and financing in the statement of cash flows used by IFRS reporters in the UK today (IFRS Foundation overview of IAS 7).

Why employers care about this skill

If you work in bookkeeping or as an accounts assistant, people won’t only ask whether the records balance. They’ll ask things like:

- Can the business pay suppliers on time: That often comes down to cash, not profit.

- Why did bank balances fall this month: The answer may sit in stock purchases, loan repayments, or slow customer collections.

- What changed from last quarter: A cash flow statement gives a cleaner story than looking at the bank alone.

That’s why trainees who understand cash flow often become useful quickly. They can move beyond posting entries and start explaining what the numbers mean.

Practical rule: If you can explain why profit and cash are different, you’re already thinking like a stronger finance professional.

Where this shows up in day-to-day work

In Xero, Sage, and similar systems, you’ll often review reports that look straightforward until timing differences appear. A sales invoice increases revenue, but no cash arrives until the customer pays. A depreciation journal reduces profit, but no money leaves the bank. IAS 7 helps you sort those effects properly.

This also links closely to working capital. If you want a simple UK-focused primer on that area, this guide on working capital management basics for trainees is useful background.

Outside formal reporting, cash flow thinking also matters when firms look at forecasting and operations. If you want a broader practical read on how finance teams try to enhance financial health for MENA businesses, it’s a helpful example of why cash discipline matters beyond the accounts department.

The Three Core Activities of a Business

The heart of IAS 7 is simple. Every cash movement must fit into one of three buckets. If you remember that, the rest becomes easier.

It’s comparable to running a household.

Your wages and normal bills are one category. Buying or selling a car is another. Taking out a mortgage or repaying a loan is a third. A business works in a similar way.

Operating activities

Operating cash flows are the day-to-day cash flows from the principal revenue-producing activities of the business. That practical definition matters because this is the section often watched first when judging whether trading activity is generating cash.

For a trainee in a UK finance role, operating items often include cash linked to customers, suppliers, wages, overheads, and core business expenses. In software terms, the main movement behind sales ledgers, purchase ledgers, payroll postings, and VAT-related timing often feeds into the wider cash story.

A key technical point also catches many people out. Guidance used by UK trainees explains that interest and dividends can be classified in operating, investing, or financing activities if the policy is applied consistently, and each item must be shown separately. It also notes that companies must look at the nature of each separate cash-flow component, not just the headline transaction (BDO guide to IAS 7 in practice).

That means one payment can have more than one cash flow character.

- Lease payment example: The principal part may be financing, while the interest part may follow the company’s policy choice.

- Interest example: You can’t assume it always sits in operating.

- Dividend example: It must be shown separately and classified consistently.

Split mixed transactions into their real cash components. Don’t classify the whole payment by its label alone.

A short explainer can help if you want to hear this discussed in a different format:

Investing activities

Investing activities deal with cash spent on, or received from, longer-term assets and investments. Such activities typically involve buying equipment, selling machinery, or making certain longer-term investment moves.

For an accounts assistant, this often appears when reviewing fixed asset additions. If the company buys laptops, machinery, or vehicles and pays cash, that’s usually investing cash flow rather than an operating expense. The purchase may support operations, but the cash movement sits in the investing section.

This is one of the first places trainees confuse accounting treatment with cash flow classification. Capital expenditure may not hit profit immediately, but it still uses cash now.

Financing activities

Financing activities show how the business raises and repays capital. Loans received, loan repayments, and some owner-related funding movements often sit here.

In practical office work, you might spot financing cash flows when:

- The bank loan arrives: Cash in, but not trading income.

- The company repays borrowing: Cash out, but not an operating expense.

- A finance arrangement changes: Some movements may need separate review if cash and non-cash elements both exist.

If you’re training as a business analyst or data analyst, this section matters because financing cash flows can change how healthy the business looks. A company can appear comfortable on cash for a period because it borrowed more.

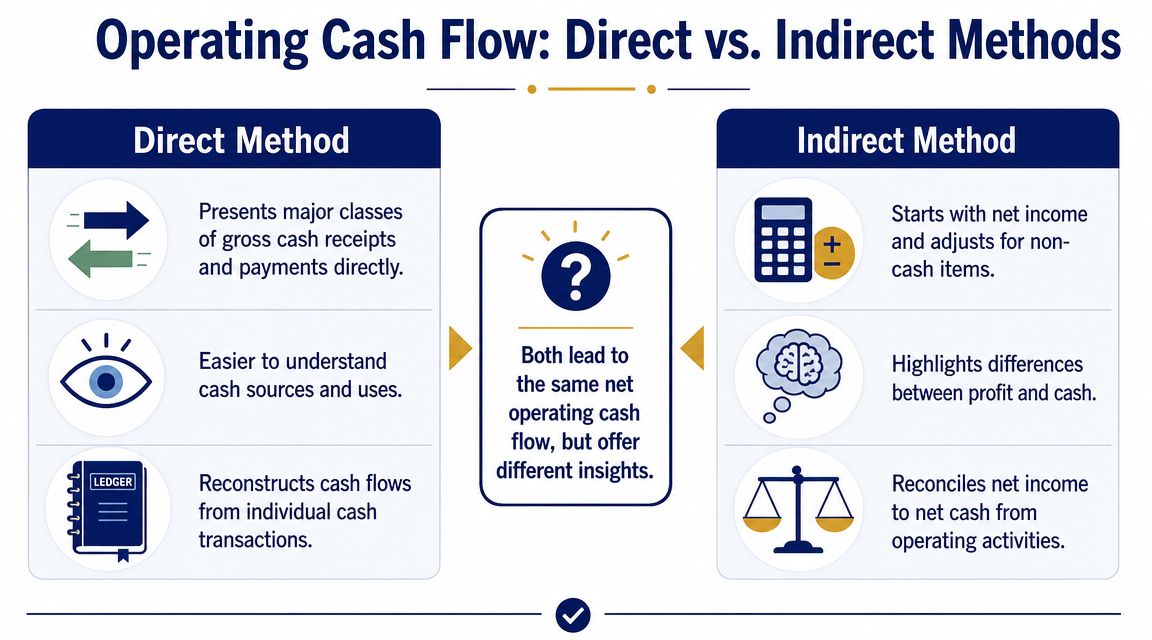

Choosing Your Approach Direct vs Indirect Methods

Most trainees first learn the cash flow statement through the indirect method, and that’s sensible because it’s what you’re most likely to see in UK IFRS reporting.

IAS 7 allows two ways to present operating cash flows. The method changes the presentation, not the underlying business reality.

What the direct method looks like

The direct method shows major classes of actual cash receipts and cash payments. In plain language, it answers questions such as:

- cash received from customers

- cash paid to suppliers

- cash paid to employees

For a beginner, this is often easier to read. It feels close to a bank analysis. If you’ve worked in bookkeeping, it can seem intuitive because it follows real cash movements.

The challenge is preparation. Pulling together gross cash receipts and payments can take more detailed reconstruction from records and systems.

Why the indirect method is more common

Guidance relevant to UK IFRS reporting notes that IAS 7 permits both the direct and indirect methods, but the vast majority of UK companies reporting under IFRS use the indirect method. It also explains why that matters. The indirect approach links the statement of cash flows to the income statement and statement of financial position through a reconciliation that analysts and lenders find useful (RSM note on cash flows and presentation options).

That’s exactly why it dominates in practice. It starts with profit and walks the reader to cash.

If your manager hands you a published set of IFRS accounts in the UK, expect to see the indirect method.

Side-by-side thinking for trainees

Here’s the practical difference in how the two methods feel at work:

| Method | Best way to think about it | Typical trainee experience |

|---|---|---|

| Direct | “Show me the actual cash in and cash out” | Easier to understand, harder to compile |

| Indirect | “Show me why profit is not the same as cash” | More common in final accounts and reviews |

If you work with Xero or Sage, the indirect method usually fits better with year-end reporting because the underlying ledgers already support a reconciliation from profit to cash. That’s useful when preparing final accounts, supporting audit files, or answering lender questions.

For businesses thinking more broadly about forecasts and budgeting, a planning mindset also helps. If you want another angle on this, this piece on 2026 financial planning for growth gives useful context for how finance teams approach future cash needs, even though IAS 7 itself focuses on reporting past movements.

Which one should you master first

Start with the indirect method. Not because the direct method is unimportant, but because the indirect method will sharpen your understanding of accruals, working capital, and non-cash adjustments.

That skill transfers well across roles:

- Bookkeeping and VAT: You’ll better understand why VAT returns and cash don’t always move together.

- Accounts assistant work: You’ll support reconciliations more confidently.

- Final accounts preparation: You’ll see how profit, balance sheet changes, and cash connect.

- Business analysis and data analysis: You’ll stop treating profit as a complete proxy for cash performance.

How to Prepare a Simple Cash Flow Statement

When trainees hear “prepare a cash flow statement”, they often expect something highly technical. In practice, a simple version follows a clear routine, especially when using the indirect method.

The easiest way to learn it is to imagine you’ve been asked to draft the operating section from a trial balance, the income statement, and comparative balance sheets in Sage or Xero. You start with profit, remove non-cash effects, then adjust for working capital movements.

Start with profit, then question it

Profit is your starting point, not your answer.

If the income statement shows profit, ask two things straight away:

- Which expenses reduced profit without reducing cash?

- Which balance sheet movements show that cash came in earlier or later than the profit entry?

That mindset changes everything. You stop copying figures and start interpreting them.

Job tip: In software, don’t rely on one report alone. Cross-check the profit and loss, balance sheet, fixed asset schedule, and aged receivables report together.

The core adjustments in the indirect method

A simple indirect reconciliation usually follows this order:

- Start with profit before tax or the chosen starting profit figure: This depends on the reporting format being used.

- Add back non-cash expenses: Depreciation is the classic example because it reduces profit but doesn’t use cash in the period.

- Adjust for working capital movements: Changes in receivables, payables, and inventory can either tie up cash or release it.

- Remove or reclassify items dealt with elsewhere: Some items belong in investing or financing rather than operating.

- Deduct cash tax paid if shown in that part of the statement: Exact presentation depends on the reporting approach.

Here’s a simple worked illustration.

Worked example using the indirect method

Assume a small business has the following movements during the period. The figures below are just a teaching example to show the mechanics.

Worked Example: Indirect Method Reconciliation

| Description | Amount (£) |

|---|---|

| Profit before tax | 50,000 |

| Add back depreciation | 8,000 |

| Increase in trade receivables | (6,000) |

| Decrease in inventory | 4,000 |

| Increase in trade payables | 3,000 |

| Net cash from operating activities before tax | 59,000 |

Now let’s make sense of each line.

Add back depreciation

Depreciation reduced accounting profit, but no cash left the bank when that journal was posted in the current period. So you add it back in the indirect method.

This is one of the first adjustments trainees learn, and it’s worth understanding properly rather than memorising.

Increase in trade receivables

If receivables increased, the business recorded revenue that hasn’t yet turned into cash. Some customers still owe money. That means cash is lower than profit suggests, so you subtract the increase.

In Xero or Sage, you’d usually check this through the aged receivables report and compare period-end balances.

Decrease in inventory

If inventory fell, the business likely sold stock that had already been bought earlier. That can release cash compared with the current period’s cost flow, so a decrease is often added.

Bookkeeping experience proves helpful. You’re linking stock records, purchases, and cost of sales to cash impact.

Increase in trade payables

If payables increased, the business has not yet paid for some costs already recognised. That preserves cash in the short term, so the increase is added.

For trainees, this often becomes clearer after reviewing supplier ledgers and payment run timing.

Where to find the figures in real work

In a training exercise, the numbers appear neatly in a question. In an office, they’re spread across reports.

Try this checklist:

- Profit figure: Pull it from the profit and loss report.

- Depreciation: Check journals, nominal ledger detail, or the fixed asset register.

- Receivables movement: Compare opening and closing trade receivables.

- Inventory movement: Use stock reports or balance sheet comparisons.

- Payables movement: Compare opening and closing supplier balances.

If your team is building better reporting packs, tools that bring data together can make review easier. This article on unified expense tracking reports is a useful example of how reporting design affects clarity, even if your own process still starts in Sage, Xero, or Excel.

For a broader training-style walkthrough, this resource on how to prepare a cash flow statement is a helpful next step.

A simple sense-check before you finish

Before you hand over a draft, ask:

- Does the direction of each working capital movement make sense

- Have I removed non-cash items from operating cash flow

- Have I accidentally included investing or financing cash movements in operating

- Does the final movement agree to the change in cash and cash equivalents

That final question is where many drafts go wrong. A cash flow statement is not just a narrative. It has to reconcile.

Avoiding Common Mistakes and Mastering Disclosures

Trainees usually cope well with the three headings. The harder part is dealing with the awkward items that don’t fit neatly on first glance.

Careful reading and a good review habit make a difference.

Mistake one: treating labels as answers

A common error is to classify cash flows based on the transaction name rather than the underlying cash-flow nature.

A lease is a good example. One payment may include a financing principal element and an interest element. If you post the full bank payment under one heading without checking the split, your cash flow statement can mislead the reader.

Another trap is assuming interest and dividends always belong in one fixed category. Policy choices may be permitted, but they must be applied consistently and shown separately.

Mistake two: putting non-cash items into the cash flow statement

Some movements matter a lot but still don’t belong in the cash flow statement itself.

If a company acquires an asset through a non-cash finance arrangement, that is important information. But it isn’t a cash flow. IAS 7 requires non-cash investing and financing transactions to be excluded from the statement and disclosed separately.

That point matters in audit files and year-end accounts because non-cash movements can still affect liabilities, assets, and users’ understanding of financing risk.

Non-cash does not mean unimportant. It means disclose it in the right place.

Mistake three: forgetting the reconciliation disclosures

IAS 7 requires more than the main statement. Guidance relevant to practice explains that disclosures include a reconciliation of liabilities arising from financing activities, separating cash changes from non-cash changes. It also notes that this has become more important with amendments effective for annual periods beginning on or after 1 January 2024 relating to supplier finance arrangements, aimed at improving transparency around liquidity and funding-like liabilities (Moore Global summary of IAS 7 disclosures and amendments).

For a trainee, that means the job isn’t done once the main cash flow statement balances.

You also need to think about:

- Cash and cash equivalents reconciliation: Does the statement tie back to the balance sheet?

- Financing liabilities reconciliation: Can users see what changed because of cash and what changed for other reasons?

- Supplier finance arrangements: Has the business disclosed enough to avoid giving a misleading picture of liquidity?

Mistake four: misidentifying cash equivalents

Cash equivalents are defined narrowly under IAS 7. Not every short-term treasury placement qualifies. If an investment is not readily convertible to known amounts of cash or carries more than an insignificant risk of changes in value, it may not belong in cash equivalents.

That can affect going concern analysis, debt monitoring, and how a business appears to lenders or management.

If you’re building your wider technical knowledge, this refresher on international accounting standard 8 can help because policy choices, consistency, and judgement often overlap in real reporting work.

Using IAS 7 Knowledge to Advance Your Career

Cash flow knowledge changes how people see your work.

A bookkeeper who understands IAS 7 doesn’t just record receipts and payments. They can explain why a busy business still feels cash tight. An accounts assistant with a good grasp of cash flow becomes more useful at month end and year end because they can support reconciliations and spot classification issues early.

For trainees in final accounts, the value is obvious. You’re not engaged in basic format completion. You’re connecting the profit and loss account, the balance sheet, and real liquidity. That’s a stronger professional skill than data entry.

It also matters outside classic accounting roles. Business analysts and data analysts often work with dashboards, trends, and management reporting. If they ignore cash flow logic, they can overstate performance by focusing too heavily on revenue or profit. IAS 7 gives them a more grounded view of operational reality.

There’s also a forward-looking reason to learn this properly. EY notes that IFRS 18 is effective for annual reporting periods beginning on or after 1 January 2027, with early adoption permitted, and that IAS 7 is one of the standards receiving consequential amendments. For UK trainees, that means learning today’s rules is only the first step. Teams also need to future-proof policies, systems, and training to avoid rework later (EY guide on IFRS 18 and consequential amendments).

The trainee who keeps up with those changes will stand out. Employers notice people who can learn the rules, apply them in software, and explain the business impact in plain English.

If you want practical, job-ready support in accountancy, software, and finance skills, Professional Careers Training offers flexible training with ACCA-qualified support, Sage and Xero learning, and career-focused help for roles such as bookkeeper, accounts assistant, payroll professional, and finance analyst.