You're in the middle of a live deadline stack, one client is asking for a VAT update, another wants year-end numbers, and your inbox keeps...

Why IAS 19 Matters for Your Accounting Career

Your first real encounter with IAS 19 often happens in a practical setting. You might be helping prepare final accounts and notice a pension note that doesn’t match the cash paid into the scheme. Or you might be in payroll and wonder why the pension amount in the accounts is not the same as the monthly deductions. That confusion matters, because the people who can explain the difference are the people managers trust with more responsibility.

IAS 19 is bigger than pensions

IAS 19 (Employee Benefits) is the core International Accounting Standard used in the UK for accounting for employee benefits. The IFRS Foundation says an entity must recognise a liability when an employee has provided service in exchange for future benefits, and an expense when the entity consumes the economic benefit of that service, as set out in the IFRS Foundation’s IAS 19 overview.

That sounds technical, but the idea is simple. If staff have earned something, the business usually needs to record it, even if cash leaves later.

That affects more than pensions. It reaches into:

- Wages and salaries recorded through payroll

- Paid holiday and other absences

- Bonuses earned before payment

- Termination benefits

- Post-employment benefits, including pensions

If you’re building your understanding of wider business accounting standards, IAS 19 is one of the standards that shows how day-to-day workforce costs flow into financial reporting.

Why trainees should care early

For an Accounts Assistant, IAS 19 helps you understand why journals don’t always follow cash. For someone in advanced payroll, it explains why payroll output is only one part of the accounting story. For a learner on a final accounts track, it helps you read notes, movements, and disclosure wording with confidence.

It also matters if you want to move into Business Analyst or Data Analyst roles. Pension and benefit costs often affect margins, forecasts, and balance sheet interpretation. If you can connect the accounting treatment to what it means for the business, you become more useful in meetings and reporting work.

Practical rule: The trainee who can explain why a number appears in profit or loss, equity, or the statement of financial position usually progresses faster than the trainee who only posts journals by routine.

There’s also a wider professional reason to learn it properly. IAS 19 is used internationally, and secondary sources describe adoption in more than 140 countries, reinforcing why it remains a global benchmark for finance teams, as noted in the IFRS Foundation summary of IAS 19.

The link above is useful because standards don’t sit alone. Once you start reading one properly, you realise financial reporting is a connected system.

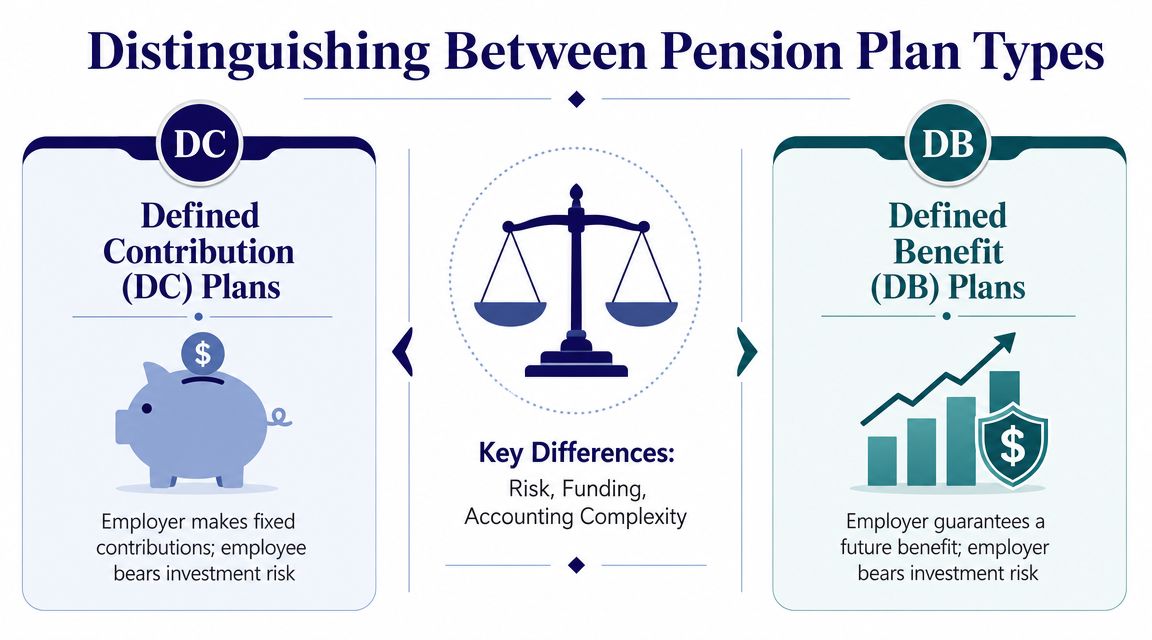

Distinguishing Between Pension Plan Types

Most IAS 19 confusion starts with one basic issue. People hear “pension” and assume all pension accounting works the same way.

It doesn’t.

The first job is to separate defined contribution plans from defined benefit plans. If you mix them up, everything else becomes harder than it needs to be.

Defined contribution plans in plain English

A defined contribution plan is the easier one to grasp. Picture it as a savings pot.

The employer agrees what it will pay in. Once that contribution has been made, the employer’s obligation is generally finished. The employee’s final retirement outcome depends on contributions, investment performance, and what happens over time.

From a trainee perspective, this usually feels familiar. You see the employer pension contribution, process it through payroll or journals, and move on.

Defined benefit plans in plain English

A defined benefit plan is very different. Think of it as a promise about the benefit itself, not just the contribution.

The employer carries more risk because it has promised a future pension outcome under the plan terms. That means the accounting has to estimate the value of that promise and compare it with the assets set aside to meet it. That’s why IAS 19 becomes far more complex here.

Defined Contribution vs Defined Benefit Plans at a Glance

| Feature | Defined Contribution (DC) Plan | Defined Benefit (DB) Plan |

|---|---|---|

| Core promise | Employer promises contributions | Employer promises a future benefit |

| Main risk | Employee bears investment risk | Employer bears more of the pension risk |

| Accounting difficulty | Usually simpler | Usually more complex |

| Need for actuarial input | Limited in routine accounting | Central to measurement |

| Typical trainee view | Similar to payroll cost processing | Requires balance sheet and disclosure understanding |

| Focus in accounts | Expense for contributions due | Net pension position and movements |

A quick way to test yourself is this:

- If the promise is the payment in, you’re usually thinking about defined contribution.

- If the promise is the retirement outcome, you’re usually thinking about defined benefit.

When a trainee says, “But we already paid into the scheme, so why is there still a pension liability?”, that usually signals they’re treating a defined benefit scheme like a defined contribution scheme.

Why this distinction matters in real jobs

In bookkeeping and VAT work, you may never do full defined benefit accounting yourself, but you still need to know when a transaction is not just a simple expense line.

In advanced payroll, the distinction helps you understand why gross pay, employer contributions, and financial statement costs do not always line up neatly.

In accounts assistant and final accounts roles, your work transitions from processing to interpretation. A manager may ask you to trace pension entries, tie note disclosures, or explain why contributions reduced cash but didn’t equal the period expense.

That’s the sort of work that moves you from data entry towards judgement.

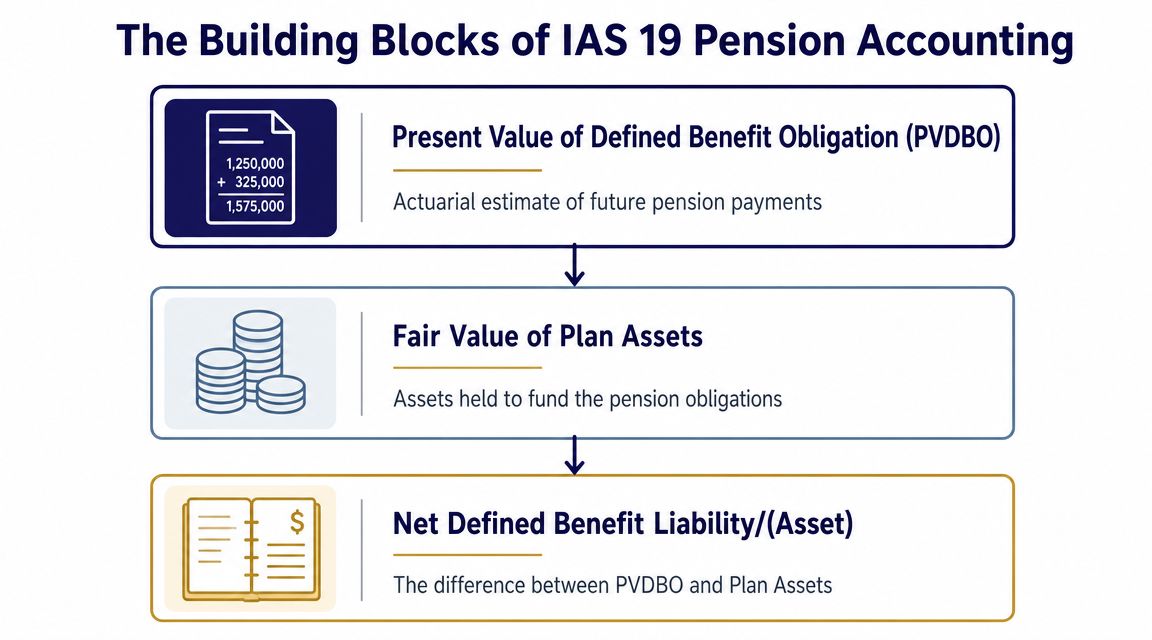

The Building Blocks of IAS 19 Pension Accounting

Once you know a pension is a defined benefit plan, the accounting becomes easier to follow if you stop thinking of it as one giant mysterious number.

Instead, break it into a few moving parts. At the centre is the net defined benefit position. Under IAS 19, UK employers with defined benefit pension schemes measure the obligation using the projected unit credit method and recognise the net defined benefit position as the present value of the obligation less the fair value of plan assets, with actuarial gains and losses recognised in other equity-affecting income rather than profit or loss, as reflected in the IAS 19 text referenced in the European Commission materialD019014-01(ANN2)_EN.doc).

Service cost

Start with service cost. This is the value of the extra pension benefit employees earn from working in the current period.

If someone works another year and that service increases the pension promise, the business has incurred a cost from that service. That cost goes through profit or loss because it relates to employee service in the period.

For trainees, this is the easiest piece to understand because it behaves like an employment cost.

Net interest

Then there’s net interest. This catches people out because nothing obvious may happen in payroll or cash terms.

The logic is that pension obligations are measured as present values. As time passes, the obligation changes. IAS 19 captures that financing-style effect through net interest. It also runs through profit or loss.

If you work in analysis, this matters because it tells you some pension cost is linked to the passage of time, not to new employee work in the year.

Remeasurements

The third block is remeasurements. Volatility often appears here.

Remeasurements come from changes in assumptions and from differences between what was expected and what transpired. For example, assumptions about discount rates or how plan assets performed may change the pension position. Under IAS 19, those actuarial gains and losses are recognised in Other Comprehensive Income (OCI) rather than profit or loss, which means the volatility shows in equity and the statement of financial position without sitting in operating profit.

A good analyst doesn’t stop at profit. Pension movements can sit outside operating profit and still change the strength of the balance sheet.

A simple way to remember the reporting split

Use this short memory aid:

- Current year work done by employees goes to profit or loss

- Time passing on the pension position goes to profit or loss

- Unexpected valuation swings go to OCI

That split matters in final accounts work. If you place all pension movements into one expense line, the statements will be wrong. If you can separate them properly, you’re already thinking at a higher level than many entry-level staff.

What this means for career growth

This is one of those topics that distinguishes processors from developing professionals.

A bookkeeper may record payroll costs accurately. A stronger accounts assistant can also understand why a defined benefit note includes a movement through OCI. A business analyst who understands this can read annual reports more intelligently. A data analyst can map pension movements separately from operating performance instead of lumping everything into one trend line.

Those are practical skills, not academic extras.

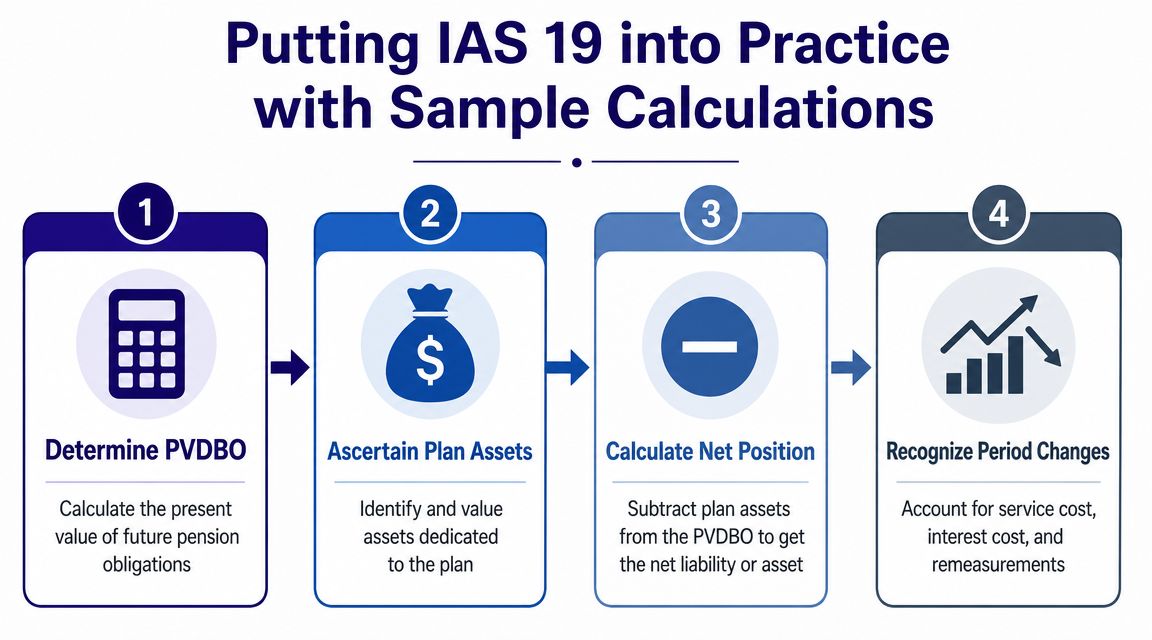

Putting IAS 19 into Practice with Sample Calculations

Theory only sticks when you can walk it through with numbers. So take a simple example and focus on the logic rather than trying to mimic a full actuarial report.

Assume a company starts the year with:

- Defined benefit obligation of £1,000,000

- Plan assets of £920,000

Its opening net liability is therefore £80,000.

During the year:

- Current service cost is £60,000

- Net interest cost is £4,000

- The employer pays contributions of £50,000 into the scheme

- A year-end actuarial loss recorded in OCI is £30,000

Here’s the video version of the topic if you prefer to hear the flow before reading the journals.

Step 1 Work out the year’s accounting charge

The amount going through profit or loss is:

- Service cost £60,000

- Net interest cost £4,000

Total charge to profit or loss: £64,000

The amount going through OCI is:

- Remeasurement loss £30,000

Step 2 Update the liability

Start with the opening net liability of £80,000.

Add:

- Profit or loss pension expense £64,000

- OCI remeasurement loss £30,000

Subtract:

- Employer contributions paid £50,000

Closing net liability: £124,000

That closing figure is what you would expect to see on the statement of financial position for the pension scheme, in this simplified example.

Step 3 Translate it into journals

This is the part trainees need for real work.

To record service cost and net interest

- Dr Staff costs or pension expense £64,000

- Cr Pension liability £64,000

To record employer contributions

- Dr Pension liability £50,000

- Cr Bank £50,000

To record actuarial loss in OCI

- Dr OCI £30,000

- Cr Pension liability £30,000

These entries show one of the key lessons in international accounting standards 19. Cash paid is not the same as pension expense.

Career checkpoint: If you can explain why contributions reduce the liability but do not automatically equal the period expense, you’re ready for stronger final accounts work.

Where learners get stuck

The most common errors are usually these:

-

Mixing cash and expense

Paying into the scheme feels like the cost, but IAS 19 separates funding from accounting measurement. -

Ignoring OCI

Trainees often expect all gains and losses to hit profit or loss. Pension remeasurements don’t. -

Forgetting the opening position

Pension accounting is movement-based. If the opening liability is wrong, the closing figure won’t make sense. -

Treating actuarial numbers as optional notes

They aren’t. They affect recognised amounts in the financial statements.

For someone on an Accounts Assistant course, this example builds confidence with journals. For a Business Analyst, it shows how reported employment cost can differ from cash outflow. For a Data Analyst, it highlights why one pension-related figure in a dataset rarely tells the full story.

Understanding Disclosures and Actuarial Assumptions

Recording the journals is only half the skill. The other half is understanding what the annual report is telling you.

IAS 19 requires companies to disclose information that helps readers understand the nature of their employee benefit obligations and the financial effects of those obligations. In UK reporting, that often means pension notes showing movements in obligations and assets, the net position, recognised amounts, and commentary on assumptions and future contributions. A useful technical overview sits in this IAS 19 employee benefits training resource.

What analysts should look for

If you’re moving towards business analysis or data analysis, don’t read a pension note as a compliance exercise. Read it as a risk and strategy note.

Focus on:

- Movement tables that explain how the opening position became the closing position

- Recognition split between profit or loss, OCI, and cash contributions

- Narrative disclosures about funding, risk, and future cash commitments

- Sensitivity to assumptions, because small changes in assumptions can shift the reported position materially

Accounting and analysis intersect. A company may report stable operating profit while pension remeasurements still alter equity and the balance sheet.

What the actuary is doing

Actuaries estimate the present value of future obligations. They use assumptions about matters such as discount rates and longevity. You don’t need to become an actuary to work with IAS 19, but you do need to understand that these assumptions drive reported numbers.

If you’re in a trainee role, your practical task may be simpler:

- tie the actuarial report to the accounts,

- check that disclosures reflect the underlying schedules,

- and make sure management understands what changed.

Pension disclosures tell two stories at once. One is the accounting result. The other is management’s exposure to future uncertainty.

That second story is why IAS 19 matters to analysts as much as accountants.

Navigating Challenges and Advancing Your Career

The hardest part of IAS 19 isn’t memorising definitions. It’s resisting the instinct to treat pension accounting like ordinary cash accounting.

A trainee usually makes one of three mistakes. They equate contributions with expense. They miss the OCI element. Or they read the pension note without connecting it to business risk. Each mistake is understandable. None of them is harmless.

The practical traps to avoid

Keep these points in mind:

- Separate funding from accounting. Cash paid into a scheme may reduce a liability without matching the period’s reported expense.

- Read beyond payroll. Payroll gives part of the picture, but IAS 19 can reach into provisions, OCI, and disclosures.

- Use the full statement set. You need the statement of financial position, profit or loss, OCI, and notes to understand the complete effect.

The future angle matters too. ICAEW notes that as UK pension schemes mature, the focus is shifting from accounting for open schemes to managing the exit from pension risk through buy-outs and de-risking, which means accountants increasingly need to explain not only the numbers but also the strategy around managing and exiting the liability, as described in ICAEW’s IAS 19 guidance tracker.

That changes the skill set employers value.

How training supports that progression

Different courses support different parts of this topic:

- Bookkeeping and VAT builds the discipline of accurate ledger work and reconciliations.

- Advanced payroll helps you understand employee-related costs and benefit flows beyond simple payslips.

- Accounts assistant training develops confidence with journals, working papers, and month-end logic.

- Final accounts training helps you place IAS 19 movements in the correct statements and notes.

- Business analyst and data analyst training helps you interpret disclosures, trends, and risk implications.

One practical option is continuing professional development for accountants, especially if you already work in finance and want to turn technical weak spots into stronger career assets. Professional Careers Training also offers IAS 19 employee benefits training as part of its accountancy training range.

If you can explain employee benefit accounting clearly, you become more than someone who processes numbers. You become someone who helps a business understand them.

If you want structured, job-focused support with topics like IAS 19, payroll, bookkeeping, final accounts, Excel, and analyst skills, Professional Careers Training offers practical training with accountancy and software-focused learning designed for trainees, career changers, and professionals building UK-ready finance skills.