You're in the middle of a live deadline stack, one client is asking for a VAT update, another wants year-end numbers, and your inbox keeps...

Your First Encounter with IAS 28

IAS 28 sits in that middle ground where you have influence over another business, but you don’t control it outright. In UK reporting under IFRS, it’s the standard used for investments in associates and joint ventures using the equity method. The investment starts at cost and is then adjusted for the investor’s share of the investee’s profit or loss and other income recognized in equity, with UK-facing guidance noting this as the core treatment for annual reporting periods beginning in 2025 and beyond according to the IFRS Foundation summary of IAS 28.

If that sounds technical, think of it this way. You’ve bought a meaningful stake in another business, so your accounting shouldn’t stay frozen at the original purchase price. If that business performs well, your investment has changed. If it performs badly, that also affects your books.

Why trainees often find this hard

Most early training focuses on clean, direct entries:

- Sales invoice posted

- Supplier bill recorded

- VAT return prepared

- Payroll journals entered

- Bank reconciled

IAS 28 doesn’t feel like that. It asks you to think about ownership, influence, reporting standards, and year-end adjustments. That’s why many trainees first meet it during final accounts work rather than day-to-day bookkeeping.

Practical rule: If a number in the accounts changes because another business made profit or loss, you’re no longer in basic bookkeeping territory. You’re in financial reporting territory.

That’s also why formal study matters. A good grounding in financial reporting standards helps you understand not just what to post, but why the treatment exists in the first place.

Where this shows up in real jobs

For an Accounts Assistant, IAS 28 may appear when supporting year-end files, reconciling investment balances, or preparing schedules for a senior accountant.

For someone working on final accounts, it matters much more. You may need to trace how the investment moved from one year to the next and explain why dividends don’t work the way many beginners expect.

For a Business Analyst or Data Analyst, the value is different. You might not post the journals yourself, but you do need to understand what that line means when reviewing company performance. A static reading of the balance sheet can be misleading if you don’t know how equity accounting works.

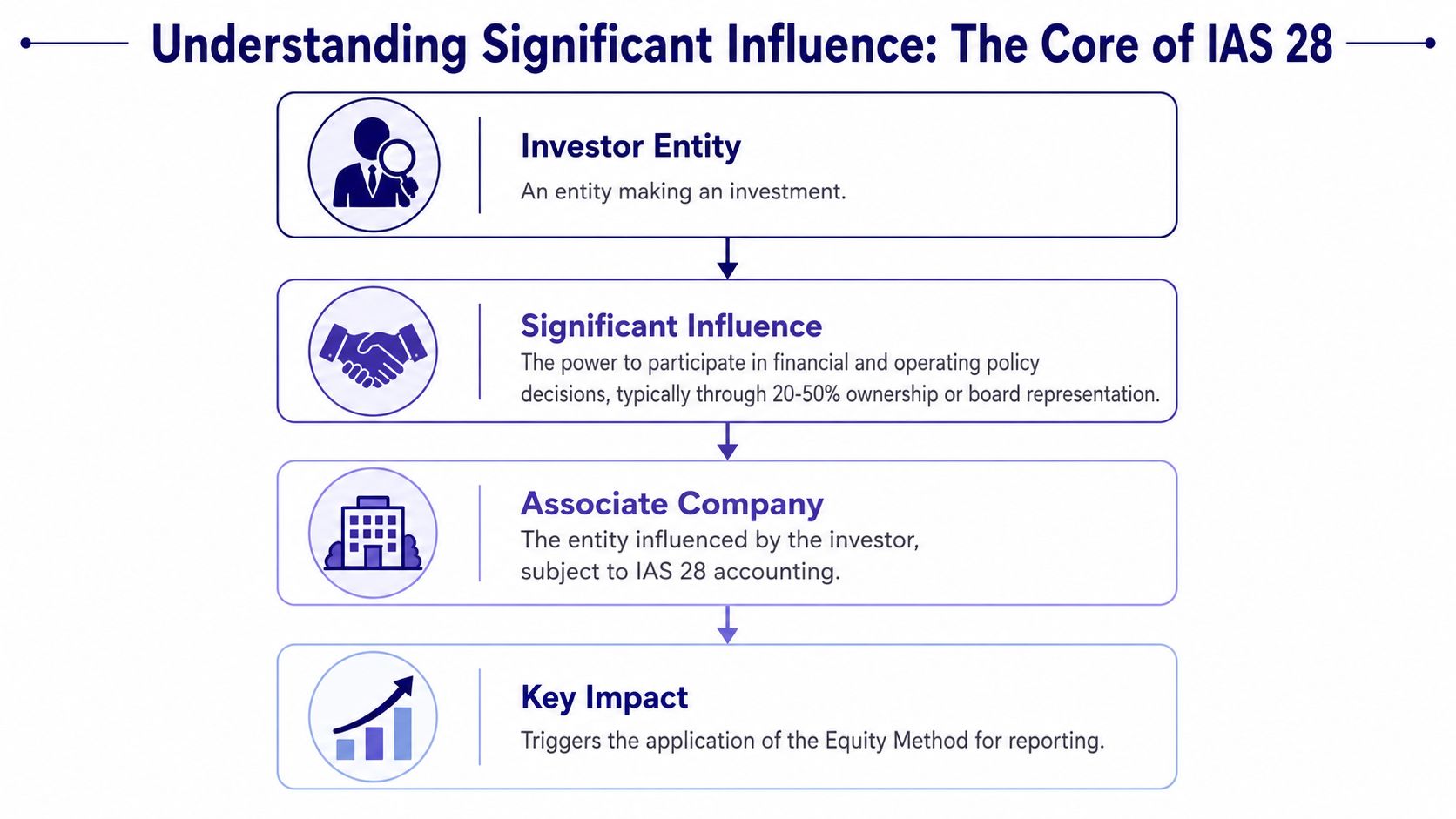

Defining Significant Influence an Associate

The heart of IAS 28 is significant influence. That phrase matters because the standard doesn’t apply just because a company owns shares. It applies when the investor can take part in important decisions without having full control.

A plain-English way to think about it

Suppose your friend runs a small company. If you buy a tiny holding and never hear from them again, you’re just an investor. If you regularly attend meetings, help shape decisions, and your opinion carries weight, you have influence.

That’s the distinction IAS 28 cares about.

An associate is generally an entity over which the investor has significant influence. It isn’t a subsidiary, because the investor doesn’t control it. But it also isn’t a passive investment.

The voting rights benchmark

A widely used practical benchmark in IAS 28 is the 20% voting-rights presumption. Holding 20% or more of the voting power is presumed to give significant influence, while holdings below 20% are generally presumed not to, unless there is other evidence. UK professional guidance also notes a rebuttable range of 20% to 50% and points to indicators such as board representation, participation in policy-making, material transactions, and interchange of managerial personnel, as explained in this IAS 28 overview from IFRScommunity-style technical guidance at IFRSideas.

That benchmark is helpful, but it isn’t a shortcut you apply blindly. The phrase presumed is doing a lot of work. Presumed means you start there, then check the facts.

What significant influence looks like in practice

Here are some signs that usually point in the right direction:

- Board involvement means the investor has a real voice in decisions, not just a financial interest.

- Policy participation suggests influence over how the business is run.

- Material transactions can show the relationship is more than arm’s length.

- Managerial interchange points to a continuing operational link.

A trainee often gets confused here by mixing up influence and control. Keep the distinction simple:

| Relationship | What it means in plain language | Typical accounting direction |

|---|---|---|

| Passive investment | You own shares but don’t influence decisions | Not IAS 28 |

| Associate | You have a seat at the table, but not the final say | IAS 28 equity method |

| Subsidiary | You control the business | Consolidation rules |

If you can join the conversation but can’t dictate the outcome, you’re usually closer to significant influence than control.

This matters in final accounts because getting the classification wrong means the whole accounting treatment can go wrong with it.

Mastering the Equity Method Step by Step

The equity method sounds intimidating until you stop treating it like a formula and start treating it like a running balance.

Start with the original cost

When the investment is first recognised, you record it at cost. That gives you your opening carrying amount.

Think of this as the starting size of a pot. At this point, nothing clever has happened yet. You’ve put money into the investment.

Add your share of profit

If the associate makes a profit, the investor recognises its share of that profit. This increases the carrying amount of the investment.

This is the part many trainees miss. You’re not waiting for cash to arrive before recognising the effect. The associate’s profit changes the value of what you own.

Subtract your share of losses

If the associate makes a loss, your share reduces the carrying amount. The investment balance moves down because the underlying business has weakened.

That’s why equity accounting feels different from basic share investing in a bookkeeping exercise. The balance doesn’t stay still.

Adjust for dividends

Dividends often confuse beginners because they look like income. Under the equity method, they usually reduce the carrying amount of the investment rather than being treated as fresh revenue in the same way a simple investment income entry might be treated in other contexts.

Why? Because you’ve already reflected your share of the associate’s results through the equity method. The dividend is more like money being taken out of the pot.

Include other comprehensive income

There’s another moving part. If the associate reports items recognized directly in equity, the investor adjusts the carrying amount for its share of those items as well.

For trainees, the main lesson is this: IAS 28 doesn’t just follow profit. It follows the investor’s share of the associate’s broader reported performance.

A simple memory aid

Use this sequence when reviewing year-end workings:

- Start with opening carrying amount.

- Add or subtract your share of profit or loss.

- Adjust for your share of items recognized directly in equity.

- Reduce for dividends received.

- Review for any further issues, such as impairment.

Think of the investment balance as a living figure, not a fixed asset cost that sits untouched year after year.

Why this matters for vocational roles

In a bookkeeping and VAT role, you may not prepare the full IAS 28 workings every day, but you do need the discipline of accurate posting and reconciliation. That habit carries straight into more advanced reporting.

In advanced payroll, the direct link is weaker, but the core skill is the same. You learn to follow rules, understand why entries move between statements, and respect period-end accuracy.

In accounts assistant work, your role often expands. You stop being the person who only enters data and become the person who can support year-end adjustments and explain them.

For final accounts preparation, the equity method is one of those topics that proves whether someone understands the story behind the numbers.

Practical Journal Entries for IAS 28

Once the theory settles, the journals become much easier. The key is to remember what the investment account is doing. It isn’t just recording a purchase. It’s tracking an ongoing stake in another business.

If you want a refresher on the mechanics of debits and credits before tackling more advanced entries, Smart Receipts’ journal entry guide gives a useful plain-language reminder of how journal structure works.

The journal logic before the table

A trainee usually asks four questions:

- Where does the initial purchase go?

- What happens when the associate makes profit?

- What if it makes a loss?

- Why do dividends reduce the investment instead of creating income in the usual way?

The answer is that the investment account acts almost like a control account for your share in the associate.

IAS 28 equity method journal entries

| Transaction | Account to Debit (Dr) | Account to Credit (Cr) | Impact |

|---|---|---|---|

| Initial purchase of investment | Investment in Associate | Bank or Cash | Creates the investment at cost |

| Recognition of share of profit | Investment in Associate | Share of Profit from Associate | Increases asset and increases profit reported by investor |

| Recognition of share of loss | Share of Loss from Associate | Investment in Associate | Reduces profit and reduces carrying amount |

| Dividend received from associate | Bank or Cash | Investment in Associate | Increases cash and reduces carrying amount |

| Share of other comprehensive income | Investment in Associate | Share of OCI from Associate | Increases carrying amount and records investor’s share of OCI |

How to read the entries like an accountant

Initial recognition

You debit Investment in Associate because the business now holds an asset. You credit Bank because cash has gone out.

This part feels familiar. It’s no different in shape from buying many other assets.

Share of profit

You debit the investment because your stake is now worth more on the books. You credit a profit-related line because your share of the associate’s result belongs in your reporting.

This is often the first point where trainees realise IAS 28 isn’t about cash. It’s about participation in results.

Share of loss

Here the direction flips. The investor recognises the effect of the associate’s loss, so the expense side is debited and the investment is reduced.

If you’re working in Sage, Xero, or QuickBooks, you may not always post this through routine day books. It may come through a period-end journal prepared from a year-end working paper.

Dividends received

This is the one that catches people out. Cash comes in, so bank is debited. But the credit goes to the investment account, not ordinary income in the way a beginner might expect.

Why? Because the profit element has already fed into the carrying amount through the equity method.

Common trainee mistake: treating dividends from an associate as if they were ordinary investment income without checking whether the equity method already captured the underlying result.

A useful working style for Accounts Assistants

When you prepare or review these journals, keep a short movement schedule beside them:

- Opening carrying amount

- Plus share of profit or minus share of loss

- Plus or minus OCI movement

- Less dividends

- Closing carrying amount

That style of schedule is excellent practice for final accounts work. It also helps business analysts who need to understand how a reported balance moved across periods.

Handling Impairment and Derecognition

Even when the equity method has been applied correctly, there’s another question to ask. Has the investment fallen in value so far that the carrying amount is no longer supportable?

Impairment is a separate check

A good everyday analogy is a car. You might keep a sensible running value for it based on normal use, but if it suffers serious damage or the market turns sharply, you need another look at its value.

That’s how impairment works here. It isn’t the same as your regular share-of-profit or share-of-loss update. It’s an additional review.

For UK reporters, impairment under IAS 28 is assessed on the net investment in the associate or joint venture, not just the equity-accounted line in isolation. The carrying amount is compared with recoverable amount using IAS 36 principles, and an impairment loss is recognised if carrying amount exceeds recoverable amount. Technical guidance also notes indicators such as significant financial difficulty of the investee and adverse market, economic, technological, or legal changes, with reversal only if recoverable amount later increases, as explained in KPMG’s technical discussion of impairment for equity method investments.

What this means in practical terms

A trainee sometimes assumes that if the associate made a loss, that’s the end of the story. It isn’t always. The investor may need both:

- Normal equity method loss recognition

- A separate impairment assessment

That can make reported results more volatile. It can also reduce the balance sheet value faster than a beginner expects.

Warning signs to watch for

If you’re supporting final accounts, these are the kinds of issues that should make you pause:

- Financial distress at the associate level

- Market deterioration affecting the associate’s operations

- Legal or technological change that harms future recoverable value

- Persistent bad results that suggest the carrying amount may be too high

A short explainer can help reinforce the idea:

Derecognition in simple terms

Derecognition happens when the investor disposes of the stake or the relationship changes so much that IAS 28 no longer applies. In plain English, the accounting changes because the nature of the investment has changed.

For a Business Analyst, this matters because classification affects trend analysis. For a Data Analyst, it matters because a movement in reported performance may reflect an accounting trigger, not just a trading event. For an Accounts Assistant, it matters because disposal and reclassification often require precise supporting journals and clean audit trails.

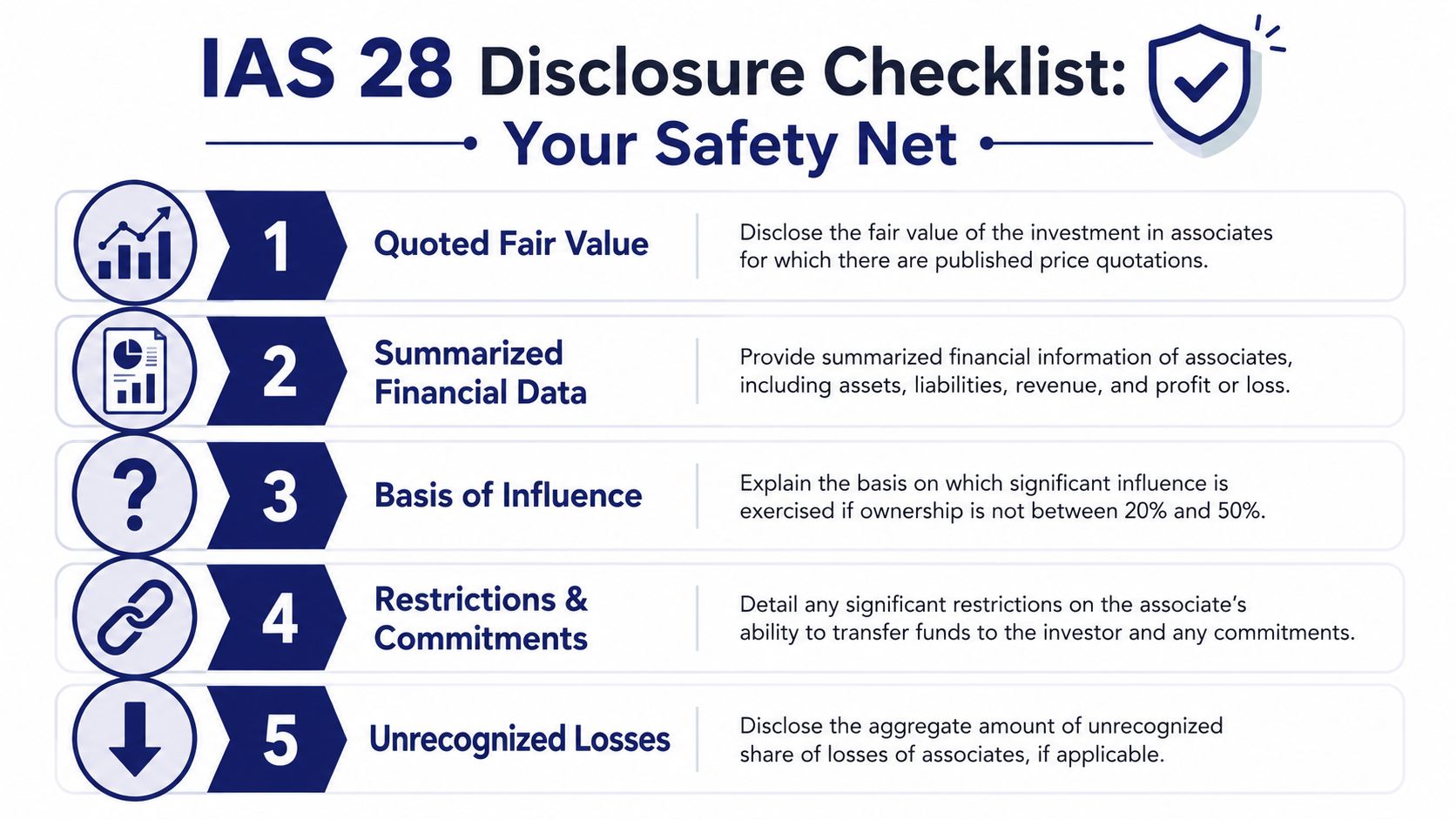

Disclosure Rules and Avoiding Common Mistakes

Getting the postings right is only part of competent reporting. The notes to the accounts matter too, because users need context for the numbers they’re reading.

A trainee-friendly disclosure checklist

When you review disclosures for an associate, think in terms of what a reader would need to understand:

- What the investment is and why it’s treated under IAS 28

- How influence is justified if the facts aren’t obvious

- What financial information helps the reader understand the associate

- Whether restrictions or commitments affect the investor

- Whether losses or value issues need extra explanation

This mindset is useful beyond IAS 28. It’s the same discipline you need when learning note disclosures under other standards, including International Accounting Standard 8 guidance for accounting policies and changes.

The mistakes that keep appearing in trainee work

Confusing dividends with revenue

This is probably the most common error. Under equity accounting, dividends generally reduce the carrying amount rather than being treated as a fresh slice of income in the ordinary way.

Mixing up associate accounting with consolidation

Some trainees try to combine line-by-line figures as if the investee were a subsidiary. That isn’t what IAS 28 requires.

Forgetting that impairment is separate

A correct equity-method movement doesn’t remove the need to consider impairment where warning signs exist.

Focusing on the percentage alone

The ownership benchmark is useful, but the actual facts of influence still matter. Good accounting work doesn’t stop at the headline percentage.

Strong final accounts work comes from asking, “What is this relationship in substance?” not just “What box can I tick?”

A good review habit

Before signing off any IAS 28 working paper, ask:

| Check | Why it matters |

|---|---|

| Is the entity really an associate? | Classification drives the whole treatment |

| Does the movement schedule reconcile? | The balance must tie to the journals |

| Have dividends been treated correctly? | This is a frequent posting error |

| Are there impairment indicators? | Losses alone may not tell the full story |

| Do the notes explain the position clearly? | Users need more than a single line item |

That’s the sort of review discipline employers notice quickly.

Build Your Career with Advanced Accounting Skills

Understanding International Accounting Standards 28 shows that you can handle more than routine processing. You can read the relationship between businesses, follow complex reporting logic, and support year-end accounts with confidence.

That has direct career value. An employer looking for an Accounts Assistant wants someone who can move beyond data entry. A role in final accounts needs someone who can follow accounting treatment through to disclosure. A Business Analyst or Data Analyst benefits from knowing when reported figures reflect business performance and when they reflect accounting method.

The gap between “I’ve heard of IAS 28” and “I can work with it” usually closes through structured practice. That means learning how standards translate into journals, reconciliations, software entries, review files, and commercial interpretation. If you’re building a finance career, it helps to keep developing across bookkeeping and VAT, advanced payroll, accounts assistant skills, final accounts, and analytical tools together rather than in isolation.

For broader career-focused study options in accountancy training, you can explore training for accountant roles and related pathways. The strongest candidates are usually the ones who combine technical understanding with practical software work, organised files, and the confidence to explain what the numbers mean.

A solid grasp of IAS 28 won’t just help you pass an exam question or follow a year-end journal. It helps you think like someone ready for the next level of responsibility.

If you want practical, job-ready support in bookkeeping, VAT, payroll, final accounts, business analysis, or data analysis, Professional Careers Training offers flexible study with 1-to-1 support from ACCA-qualified trainers, software training in Sage, Xero and QuickBooks, and career support including CV preparation, LinkedIn optimisation and job-hunting guidance.