UK tax planning has become more operational, less theoretical. HMRC says the UK tax gap was £39.8 billion in 2022/23, and small businesses accounted for...

In a first finance job, nobody expects you to know everything on day one. They do expect you to understand the logic behind financial decisions. If a manager asks why a department overspent, or whether a training project is affordable, you need more than software clicks. You need to know how numbers are built, checked, and controlled.

That’s why costing and budgeting matter so much. They sit behind everyday work in Sage and Xero, from posting supplier invoices to reviewing departmental spend, checking payroll totals, preparing VAT records, and helping managers plan ahead.

Why Every UK Career Needs Costing and Budgeting Skills

A new trainee in an office often sees budgeting as something senior people do in meetings. Then the important work begins.

An Accounts Assistant may need to code invoices correctly so spending lands in the right budget line. A Bookkeeper may need to separate fixed costs from variable ones. A payroll trainee may need to understand why labour costs moved. A Business Analyst may need to compare planned spend with actual results and explain the gap in plain English.

Start with ordinary life

Basic budgeting skills are commonly applied at home, even if they aren’t formally recognized. Rent or mortgage, utilities, food, travel, and phone bills usually come before leisure spending. That’s the same logic businesses use. Some costs are unavoidable. Some rise and fall with activity. Some look small on their own but create pressure when added together.

In the UK, this isn’t a small issue. The Office for National Statistics reports that average weekly household expenditure in the Financial Year Ending 2023 was £646.40, and housing, fuel and power was the largest category at £131.60 per week, or roughly 20.4% of average spending according to this UK household expenditure summary. That tells you something important. Strong budgets are usually built around recurring essentials first, not nice-to-haves.

Practical rule: If you can identify the costs that must be paid first, you’re already thinking like a finance professional.

Why employers care

Employers don’t just want someone who can enter figures. They want someone who understands what the figures mean.

That matters across several training routes:

- Bookkeeping and VAT: You need clean records so costs are classified properly and reports are reliable.

- Advanced payroll: You need to understand how wages, overtime, and staffing decisions affect overall cost control.

- Accounts assistant work: You’ll often help track budget lines, supplier spend, and month-end variances.

- Final accounts: You need to know which costs belong in which period and how they affect reported performance.

- Business analyst and data analyst roles: You’ll turn financial data into decisions, forecasts, and recommendations.

The first-job reality

In Sage or Xero, costing and budgeting show up in ordinary tasks. You might review nominal codes, compare this month to last month, or check whether a purchase fits the approved plan. It can feel technical at first, but the thinking is straightforward.

A budget answers, “What can we afford and approve?”

A cost answer begins with, “What will this take?”

That distinction helps you sound more confident in interviews and more useful in the workplace.

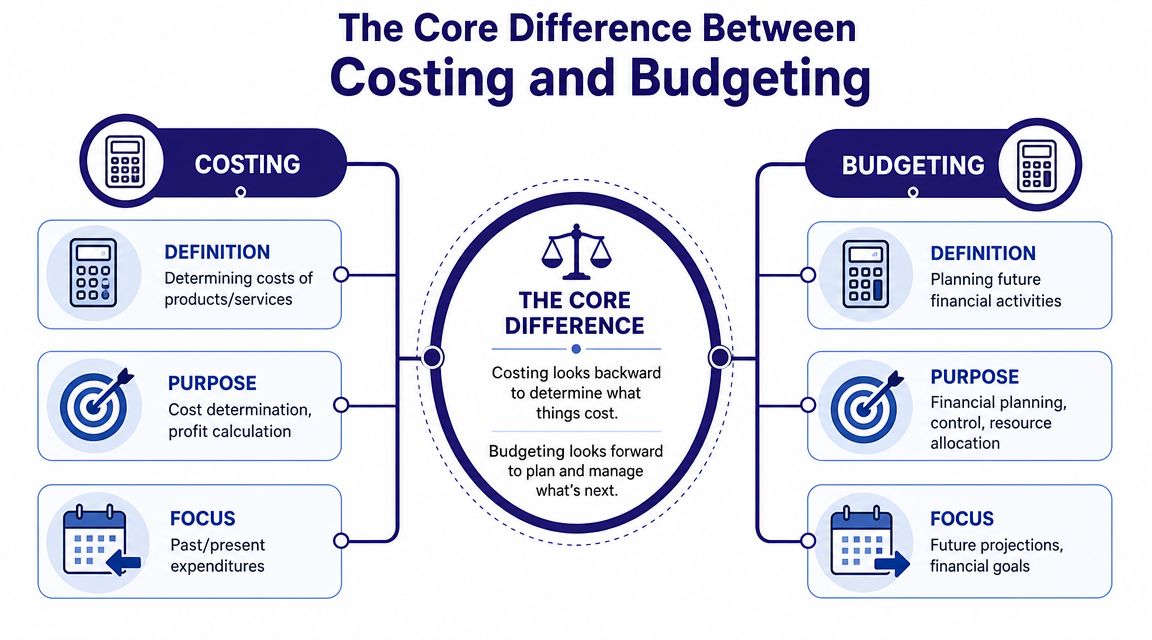

The Core Difference Between Costing and Budgeting

Many trainees use the two words as if they mean the same thing. Recruiters and finance managers usually don’t.

A simple road trip example

Think about planning a road trip.

You work out fuel, food, parking, train fares, and hotel costs. That’s costing. You’re estimating what each part is likely to cost.

Then you decide the most you’re willing or allowed to spend overall. That’s budgeting. You’re setting a spending limit and control point.

Costing gathers the pieces. Budgeting turns those pieces into a decision.

The professional meaning

In practice, cost estimating predicts likely project spend, often using methods such as three-point estimating and bottom-up estimating, while budgeting converts that estimate into an approved funding ceiling, as explained in this overview of cost estimating vs budgeting. The same source notes that for labour-heavy work, labour can represent 30% to 50% of construction project costs, which shows why even small changes in pay rates or staffing assumptions can move the whole budget.

That matters in office roles too, even outside construction. If you work in payroll, staffing is not just an HR issue. It’s a major cost driver. If you work in business analysis, labour assumptions can change the outcome of a proposal. If you work in accounts, poor estimates create bad budgets, and bad budgets create messy month-end explanations.

Where trainees usually get confused

Here are the most common mix-ups:

- Calling a quote a budget: A supplier quote is one input. It isn’t the budget by itself.

- Treating the budget as a guess: A proper budget should be approved, monitored, and updated when needed.

- Ignoring uncertainty: The first estimate is rarely the final answer.

- Skipping assumptions: If nobody records the basis of the estimate, later comparisons become harder.

Good costing asks, “What is this likely to cost?” Good budgeting asks, “What are we approving, controlling, and reviewing?”

In Sage and Xero, this difference becomes practical fast. Costs appear in ledgers, invoices, bills, payroll journals, and purchase records. Budgets appear in reporting, departmental control, and variance checks. One feeds the other.

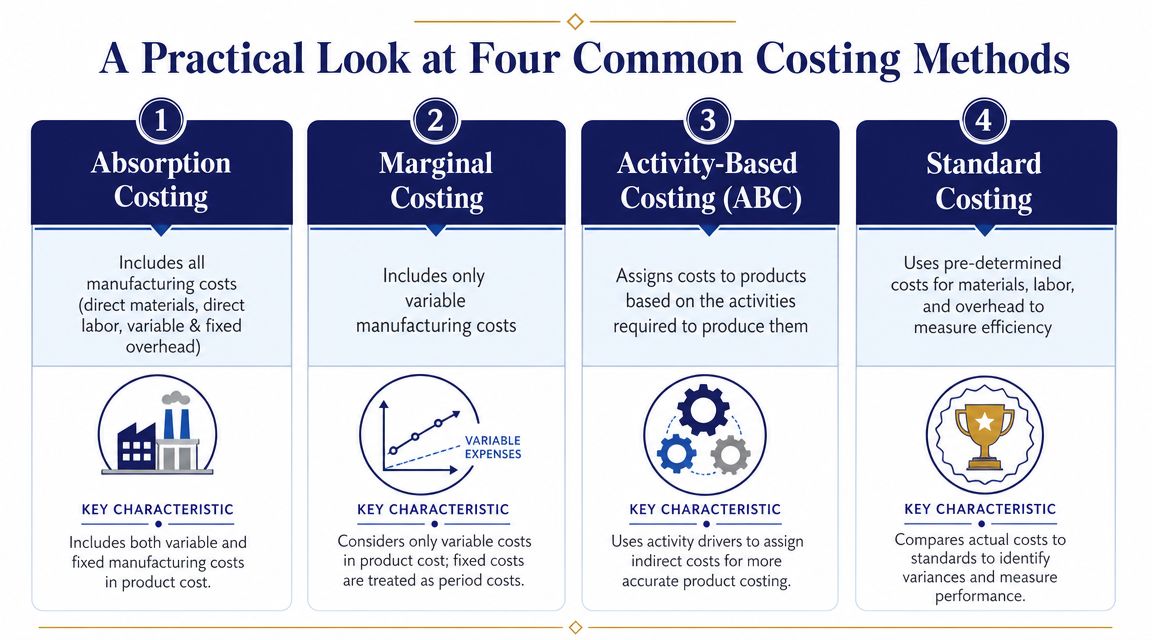

A Practical Look at Four Common Costing Methods

Different jobs need different costing lenses. You don’t need to memorise textbook definitions word for word, but you do need to recognise what each method is trying to show.

Four methods in plain English

Absorption costing includes direct costs and a share of overheads. It’s useful when you need a fuller picture of what a product or service has cost overall.

Marginal costing focuses on variable costs. It helps with short-term decisions, such as whether taking on extra work is worth it.

Activity-based costing links overheads to the activities that create them. It’s helpful when overheads are complex and managers want to know what is really driving cost.

Standard costing uses expected costs as a benchmark. Teams then compare actual results against that standard and investigate the difference.

For a trainee who wants deeper background, this guide to what cost accounting is helps connect the theory to workplace reporting.

Comparison of Costing Methods

| Method | Core Principle | Best For | Relevant Role |

|---|---|---|---|

| Absorption Costing | Includes direct costs and allocated overheads | Full product or service costing and financial reporting support | Accounts Assistant, Bookkeeper |

| Marginal Costing | Focuses on variable costs for decision making | Short-term choices, pricing discussions, contribution thinking | Business Analyst, Management Accounts Trainee |

| Activity-Based Costing | Traces overheads to activities that cause them | Complex operations with many support costs | Data Analyst, Business Analyst |

| Standard Costing | Compares expected costs with actual costs | Efficiency checks and variance review | Accounts Assistant, Finance Trainee |

Which one fits your route

If you’re training in bookkeeping or final accounts, absorption costing is often the easiest starting point because it encourages you to think beyond the obvious invoice and include wider production or service costs.

If you’re moving into business analysis, marginal costing sharpens commercial judgement. It helps you ask, “What changes if we do one more unit, one more client job, or one more campaign?”

If you’re interested in data analysis, activity-based costing is a strong bridge between numbers and operations. It asks where effort, support time, and overhead come from.

If you’re doing advanced payroll or helping with departmental reporting, standard costing supports variance thinking. You compare what was expected with what happened, then explain why.

Choosing the Right Budgeting Style for Your Goal

Not all budgets are built in the same way. Some are steady and cautious. Some are demanding. Some need regular updates because conditions change.

The safe option and the blank-page option

Incremental budgeting is the safe bet. You start with last period’s budget or actuals and adjust from there. It’s familiar and quick. It also carries old habits forward, including waste.

Zero-based budgeting starts from scratch. Every cost must earn its place. This approach is useful when a business is restructuring, reviewing spending closely, or trying to challenge long-standing assumptions.

For trainees, the key difference is this. Incremental budgeting asks, “What should we change?” Zero-based budgeting asks, “Why are we spending this at all?”

Budgets that move with reality

Rolling budgets are more dynamic. Instead of fixing one annual plan and leaving it untouched, teams update the forecast regularly as conditions change. That matters when prices, staffing needs, or timelines shift.

Flexible budgets adapt to different levels of activity. If sales, production, or service demand change, the budget adjusts too. This is useful in seasonal businesses and busy operational environments.

The UK’s move towards evidence-based budgeting is reflected in the creation of the Office for Budget Responsibility in 2010, and its forecasting role shows that modern budgeting is tied to assumptions, scenario thinking, and fiscal credibility. A March 2024 projection noted that government debt would remain above 90% of GDP for several years, while the fiscal deficit for 2024-25 was forecast at 3.1% of GDP, as discussed in this article on statistical analysis in budget reporting.

That national example matters because it mirrors workplace logic. Good budgets aren’t wish lists. They’re tested against evidence.

If you want a practical bridge into planning methods used in finance teams, this introduction to budgeting and forecasting is a useful next read.

A budget style is only “right” if it fits the decision you need to make and the level of uncertainty you face.

A quick way to choose

Use this simple guide:

- Pick incremental when the business is stable and changes are small.

- Choose zero-based when leaders want to challenge every spend line.

- Use rolling budgets when prices or plans change often.

- Use flexible budgets when activity levels rise and fall.

That decision skill is valuable in accounts, payroll support, management reporting, and analyst roles.

How to Prepare a Simple Budget from Scratch

A first budget often feels harder than it is. The trick is to stop treating it like one big number. Build it in pieces.

A simple example

Say a small firm wants a three-month marketing campaign. A trainee is asked to help prepare the budget.

The first question isn’t, “What figure should we type in?” It’s, “What are we trying to achieve?” If the purpose is lead generation, brand awareness, or event promotion, the cost lines may differ.

Build the budget step by step

-

Define the goal

Be clear about the purpose, timescale, and owner. A vague budget usually creates vague reporting later. -

Gather cost inputs

Pull historical actuals if they exist. Ask suppliers for quotes. List expected items such as design, ad spend, software, contractor time, printing, travel, or internal staff support. -

Separate fixed and variable costs

Fixed costs may stay the same through the campaign period. Variable costs may rise if activity increases. -

Add contingency thinking

Some guides still treat budgets as static annual exercises, but UK organisations increasingly need rolling forecasts and contingency planning because of persistent cost pressure, as noted in this guidance on cost budgeting and uncertainty. -

Get approval and record assumptions

Write down what the budget includes, what it excludes, and which assumptions matter most.

A useful companion resource for trainees who want another practical angle is this guide on how to budget projects effectively, especially if you’re trying to connect budgeting to real project work.

Later in the process, it helps to see a visual explanation of how the pieces fit together:

What to watch for

Beginners often miss hidden effort. Internal staff time, training, setup work, and review time can all affect the final figure.

That’s why a budget shouldn’t be left untouched after approval. If supplier prices move or scope changes, the forecast should move too. In your first role, that habit makes you far more useful than someone who just updates a spreadsheet after the fact.

Using Software for Real World Financial Control

Software turns costing and budgeting from theory into routine work.

In a finance office, Sage and Xero don’t replace judgement. They give structure to it. They help you record actuals, compare them to the plan, and spot problems early.

What this looks like in Sage and Xero

In Sage, trainees often work with nominal codes, supplier records, departmental reporting, and variance checks. You might run a report to compare actual spend against the budget and then investigate differences.

In Xero, you’ll commonly see budget data linked to reporting, account categories, and management review. You may help reconcile transactions, post bills, and prepare reports that show whether spending is in line with expectations.

Variance analysis becomes practical. The idea is simple. Compare budgeted figures with actual figures, then ask why the gap exists. Was the estimate weak? Did prices rise? Was activity higher than planned? Was a cost posted to the wrong place?

Budgeting beyond the purchase price

A professional budget should be built from historical actuals, vendor quotes, and total cost of ownership, not just headline purchase price, according to this guide on IT budgeting and TCO. It also notes that UK organisations often separate technology spend into categories such as hardware, software, staffing, outsourcing or consulting, maintenance, and projects.

That lesson applies well beyond IT.

If a business buys payroll software, for example, the full cost may include setup time, training, support, maintenance, and future renewal. A Business Analyst should think that way. So should an Accounts Assistant who’s helping code costs correctly.

If your work involves staff spending and receipts, it’s also worth reviewing options for HMRC compliant expense tools so you can see how expense capture fits into wider financial control.

For trainees comparing systems and workflow expectations, this overview of software for business accounts gives a helpful picture of where Sage, Xero, and related tools fit in early-career roles.

The best software users aren’t the fastest clickers. They’re the people who know what the report is trying to prove.

Role by role

- Bookkeeper: Keep coding clean so reports tell the truth.

- Payroll trainee: Understand how staffing costs flow into monthly reporting.

- Accounts Assistant: Reconcile, review, and support variance explanations.

- Business Analyst: Test options using full-cost thinking.

- Data Analyst: Turn messy cost data into patterns managers can act on.

Boosting Your Employability with These Core Skills

Employers notice candidates who can connect numbers to decisions.

If you can explain the difference between a cost estimate and a budget, classify costs sensibly, think about overheads, and use Sage or Xero to review actuals against plan, you already sound more work-ready than many applicants.

What recruiters want to hear

In interviews, strong candidates usually speak clearly about practical tasks.

You don’t need to pretend you’ve run a whole finance department. You do need to show that you understand everyday control points.

Try framing your skills like this:

- Accounts Assistant: “I can track spend against budget, investigate coding issues, and support month-end reporting.”

- Bookkeeper: “I understand the importance of accurate posting, VAT-ready records, and separating direct and indirect costs.”

- Advanced payroll candidate: “I know labour costs can materially affect budgets, so I pay attention to changes in wages, overtime, and staffing assumptions.”

- Business Analyst: “I look beyond upfront cost and think about full ownership cost, operational impact, and forecast changes.”

- Data Analyst: “I can organise cost data, identify trends, and help explain variances in a clear way.”

Common mistakes that weaken a trainee profile

A common budgeting mistake is focusing only on direct monthly spending while ignoring indirect costs, overheads, future replacements, and training, as explained in this discussion of budget and costing frameworks. Employers value candidates who can see the fuller picture.

Watch out for these pitfalls:

- Confusing costing with budgeting: That makes your answers sound less precise.

- Ignoring indirect costs: This creates unrealistic plans.

- Forgetting regular review: A budget without follow-up quickly loses value.

- Relying only on software output: Reports still need human interpretation.

Simple ways to build proof

You can build evidence of skill even before landing the job.

- Create a small Excel budget: Use a mock department, training event, or household plan.

- Review a variance: Compare planned and actual spend on any small project and write a short explanation.

- Practise in Sage or Xero: Learn how coding choices affect reports.

- Document your reasoning: Employers like trainees who can explain not just what they did, but why.

If you’re curious about how online accounting platforms are changing day-to-day finance work, you could also explore renn’s platform as part of your wider research into digital accounting workflows.

Costing and budgeting aren’t just exam topics. They’re employability skills. They help you speak the language of finance, support better decisions, and add value from your first week in the role.

If you want guided, job-ready training in bookkeeping, VAT, payroll, final accounts, business analysis, or accounting software, Professional Careers Training offers flexible learning with 1-to-1 support from qualified trainers, official Sage and Xero certification options, software support, and practical career help including CV preparation, LinkedIn optimisation, and job search guidance.