You open your laptop after work, look at your job goals, and feel that familiar tension. You know you should keep your skills up to...

You might be staring at a fixed asset register, a trial balance, or an AAT practice question and thinking the same thing many trainees think at first: I understand that an asset loses value, but how do I calculate that properly in the accounts? That moment matters more than many realise.

Depreciation sits right in the middle of everyday finance work. An Accounts Assistant needs it for month-end journals. A bookkeeping trainee needs it to understand final accounts. Someone moving into business analyst or data analyst work needs it to interpret asset-heavy businesses without misreading profit. If you're learning Sage, Xero, or QuickBooks, you also need enough manual knowledge to spot when a software setup is wrong.

Many learners often encounter difficulties. Textbooks often give you a formula, then move on. Real work doesn't. Real work asks you to decide which method fits the asset, enter the right values into software, post journals correctly, and explain the effect on profit and net book value in plain English.

Your Practical Guide to Asset Depreciation

If you're training for a role in bookkeeping, final accounts, advanced payroll support, or an Accounts Assistant post, depreciation won't stay theoretical for long. It shows up in purchase records, month-end routines, software setup, and exam questions. It also affects how managers read profit figures.

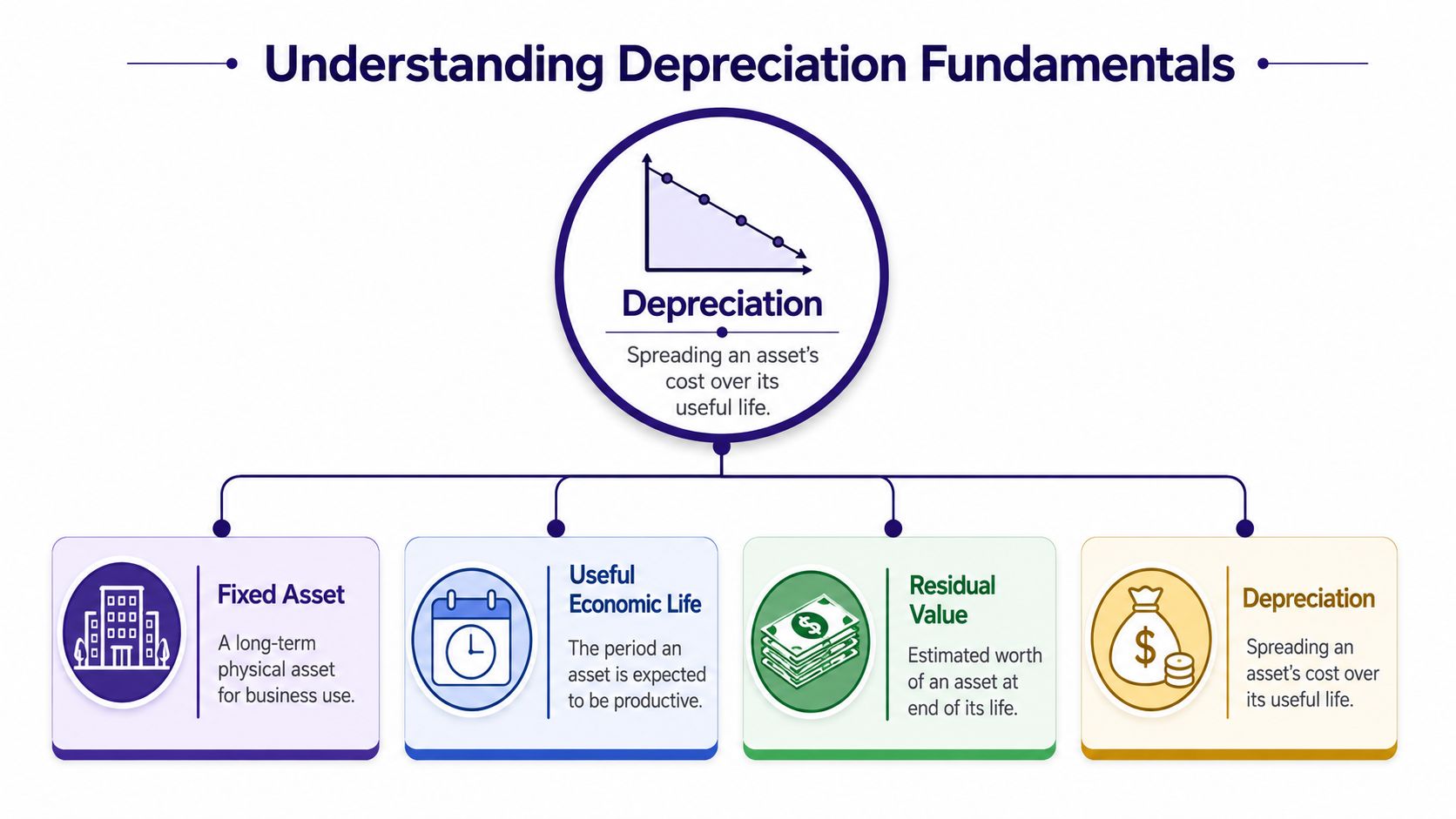

Depreciation is an accounting way of spreading the cost of a fixed asset over the period the business expects to use it. The key phrase there is spreading the cost. If a business buys a van, computer, or piece of machinery, it usually wouldn't make sense to treat the whole cost as belonging to one single period if the asset will support the business for years.

That matters in day-to-day work because finance staff don't just record payments. They help present a fair picture of performance. If you work in an Accounts Assistant role, you're often the person checking invoices, coding asset purchases, preparing journals, and reviewing reports before a senior accountant signs them off.

Why trainees often find it confusing

There are usually three reasons:

- The cash payment and the expense aren't the same thing. A company may pay for an asset upfront, but the accounting charge is spread over time.

- The language sounds technical. Terms like residual value and net book value can feel abstract until you see them applied.

- Software hides the logic. Xero or Sage can automate the posting, but the software only works well if the setup is right.

Practical rule: If you can explain depreciation to a non-accountant in one minute, you're much less likely to make errors when posting it.

This topic also links directly to training routes. In bookkeeping and VAT courses, depreciation helps you understand the difference between capital and revenue spending. In final accounts training, it affects both the profit and loss account and the balance sheet. In business analyst and data analyst training, it sharpens your ability to read financial data with more context.

What good understanding looks like

A strong trainee can usually do four things with confidence:

- Identify the asset and decide whether it should be depreciated.

- Choose the method that best reflects how the asset is used.

- Calculate the charge manually.

- Check the software output and explain the journal entry.

That combination is what employers value. It shows you aren't just clicking buttons. You're thinking like a finance professional.

Understanding the Building Blocks of Depreciation

Before you calculate anything, you need the terms to be clear. Most mistakes happen here, not in the arithmetic.

The four terms that matter most

A fixed asset is a long-term asset the business uses in operations, such as a van, laptop, office equipment, or machinery. It isn't bought for resale. It's bought to help the business earn income over time.

Useful economic life means the period the business expects the asset to be productive. This isn't always the same as the physical life. A laptop may still switch on after years, but the business may replace it earlier because it no longer performs well enough.

Residual value is the estimated amount the business expects to recover at the end of the asset's useful life. You might also hear the term salvage value. Think of it as the likely trade-in or resale value at the end.

The depreciable amount is the part of the asset's cost that will be charged as depreciation. In simple terms, it is the cost less the residual value.

A simple way to picture it

Think about a business buying a mobile phone for staff use. It has:

- A starting cost when purchased

- A working period when it gives useful service

- A possible value at the end if sold or traded in

That same logic applies to larger assets. A delivery van works in exactly the same accounting pattern, just with bigger numbers and more impact on the accounts.

If you want a stronger grounding in the wider accounting basis behind timing of income and expenses, this explanation of what is accrual accounting is useful because depreciation only makes sense when you understand that accounting doesn't just follow cash movements.

Why these estimates matter in practice

These values aren't random. They are business estimates, and they shape reported profit. If a business uses a long useful life, the annual depreciation charge will usually be lower. If it uses a short useful life, the annual charge will usually be higher.

That is why trainees need judgement as well as maths. In software, you'll often enter cost, purchase date, useful life, and method into the fixed asset register. If any one of those fields is wrong, the journals can be wrong every month after that.

A clean depreciation calculation starts with good assumptions, not clever formulas.

For learners moving towards final accounts work, it also helps to understand how accounting estimates are treated more broadly. This training resource on International Accounting Standard 8 is helpful because it builds your judgement around estimates, policies, and changes in accounting treatment.

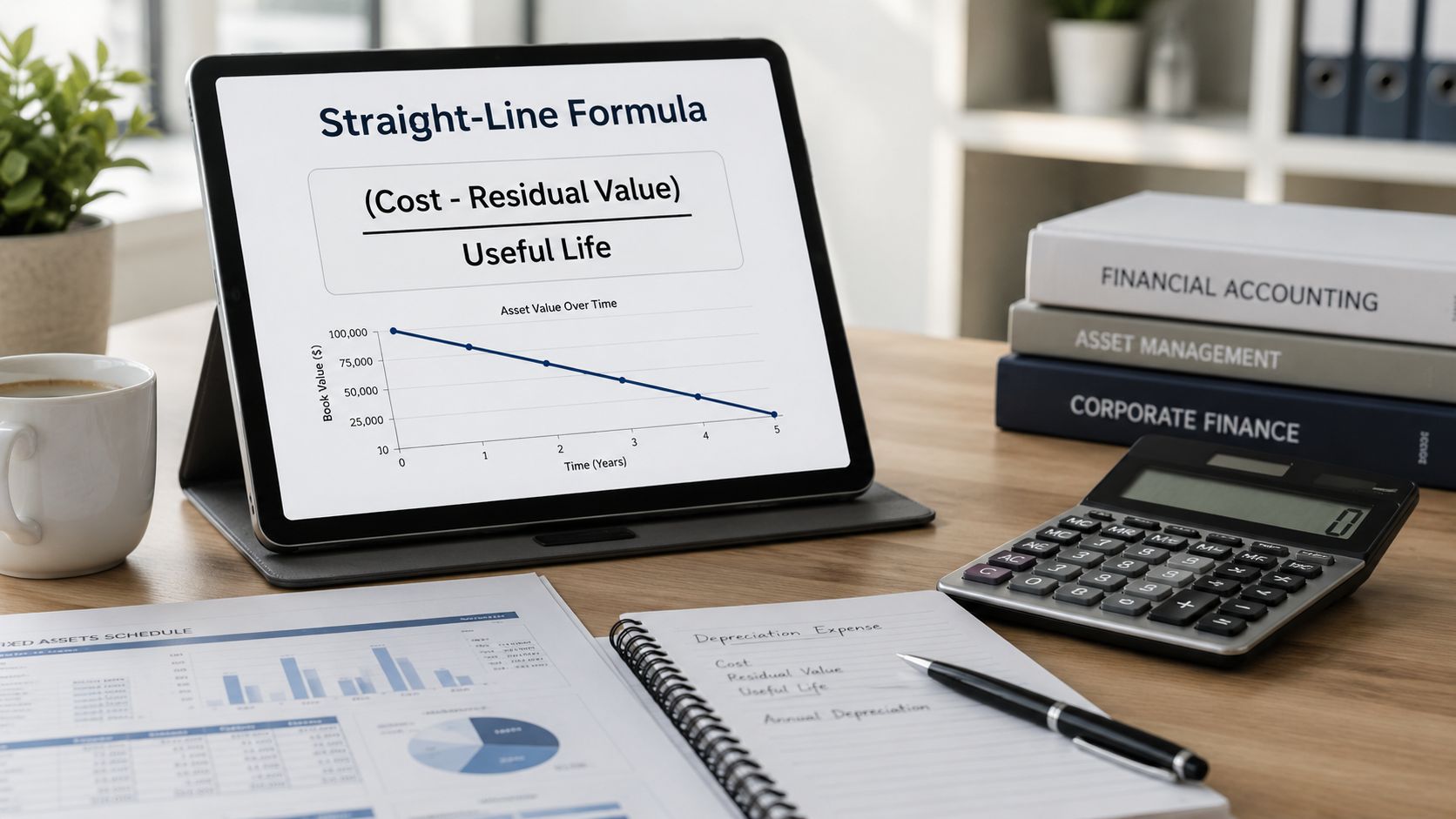

Calculating Depreciation with the Straight-Line Method

The straight-line method is the one most trainees meet first, and for good reason. In the UK, it is the most widely applied accounting technique for fixed assets. It creates equal annual charges using (Cost – Residual Value) / Useful Life, and Clear Books explains that FRS 102 requires systematic depreciation based on useful life and residual value reviewed annually, with a worked example of a £40,000 van, a 10-year useful life, £4,000 salvage value, and exactly £3,600 depreciation each year for 10 years, totalling £36,000 before the asset reaches residual value.

The formula in plain English

Straight-line is simple. You take:

- The original cost

- subtract the residual value

- then divide by the useful life

That gives you the same depreciation charge each year.

This is why many small businesses like it. It is easy to budget for, easy to explain, and easy to follow in bookkeeping and final accounts work.

Worked example using the verified UK van example

Use the figures above:

| Item | Amount |

|---|---|

| Cost | £40,000 |

| Residual value | £4,000 |

| Depreciable amount | £36,000 |

| Useful life | 10 years |

| Annual depreciation | £3,600 |

The maths is:

(£40,000 – £4,000) / 10 = £3,600 per year

That means the business records £3,600 as depreciation expense each year for 10 years.

What the schedule looks like

A schedule helps trainees see what is happening to the asset over time.

| Year | Annual depreciation | Accumulated depreciation | Net book value |

|---|---|---|---|

| 1 | £3,600 | £3,600 | £36,400 |

| 2 | £3,600 | £7,200 | £32,800 |

| 3 | £3,600 | £10,800 | £29,200 |

| 4 | £3,600 | £14,400 | £25,600 |

| 5 | £3,600 | £18,000 | £22,000 |

| 6 | £3,600 | £21,600 | £18,400 |

| 7 | £3,600 | £25,200 | £14,800 |

| 8 | £3,600 | £28,800 | £11,200 |

| 9 | £3,600 | £32,400 | £7,600 |

| 10 | £3,600 | £36,000 | £4,000 |

Notice the pattern. The expense is constant. The net book value falls steadily. It stops at the residual value, not at zero.

A quick visual walk-through can help fix the logic in your mind:

Why this method is popular in real jobs

For an Accounts Assistant, straight-line is often the easiest method to maintain month after month. It also makes reviews easier because unusual changes stand out quickly.

When your depreciation charge stays consistent, month-end variance checks become easier and mistakes are easier to spot.

In AAT and bookkeeping training, this method is often the first one tested because it reinforces core ideas clearly. In software, it is also usually one of the simplest methods to set up. You enter the cost, useful life, residual value, and start date, and the system handles the recurring journal pattern.

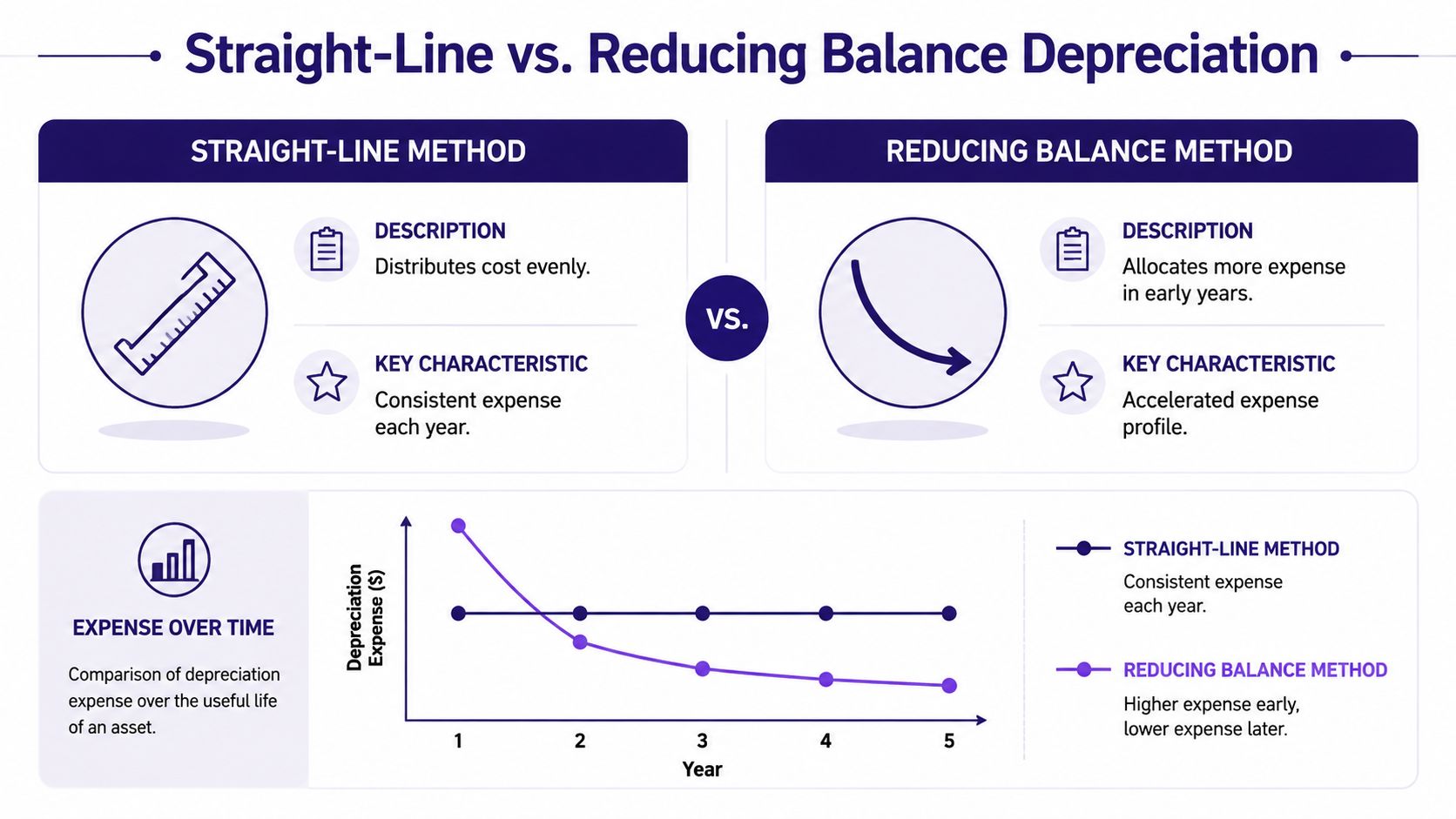

Using the Reducing Balance Depreciation Method

Not every asset loses value evenly. Some assets are more useful when new and lose value faster in the earlier years. That is where the reducing balance method becomes more suitable.

The UK-specific reducing balance method applies a fixed percentage to the opening net book value. Xero's UK guide gives an example using a £5,000 asset, with £2,000 depreciation in year one, £1,200 in year two, and smaller amounts after that, and notes that this front-loads expense for assets such as IT hardware that lose value more quickly.

How the formula works

The logic is different from straight-line. Instead of charging the same amount every year, you apply a rate to the opening net book value.

The basic form is:

Net book value × depreciation rate

That means the expense gets smaller over time because the net book value gets smaller over time.

Worked example from the verified data

Use the verified pattern:

| Year | Opening net book value | Depreciation | Closing net book value |

|---|---|---|---|

| 1 | £5,000 | £2,000 | £3,000 |

| 2 | £3,000 | £1,200 | £1,800 |

After that, the charges keep reducing because each year's calculation is based on a lower opening value.

This creates a very different shape from straight-line. Under straight-line, the expense stays level. Under reducing balance, the charge is heavier earlier and lighter later.

When this method makes more sense

Think about specialist technology, computers, or equipment that becomes outdated quickly. A new asset may deliver more value in the first part of its life, then less later as wear, efficiency loss, or obsolescence sets in.

That is why reducing balance can be a better match in some businesses. It aligns the accounting charge more closely with the asset's pattern of usefulness.

A simple comparison makes the difference easier to grasp:

- Straight-line works well when the asset gives a fairly even level of benefit over time.

- Reducing balance works well when the asset gives stronger benefit in the early years.

- Management impact differs too. Reducing balance leads to higher early depreciation charges and lower later charges.

What trainees should watch for

Learners often make one recurring mistake here. They apply the percentage to the original cost every year. That would be wrong for reducing balance. The percentage is applied to the opening net book value, not the original cost after year one.

Exam tip: If the annual depreciation figure keeps changing, check whether the question is using opening net book value rather than original cost.

This method appears often in bookkeeping and final accounts training because it teaches you to read the balance sheet more carefully. It also sharpens your thinking for analyst roles. If you compare companies with different depreciation methods, the profit pattern can look different even when the underlying asset base is similar.

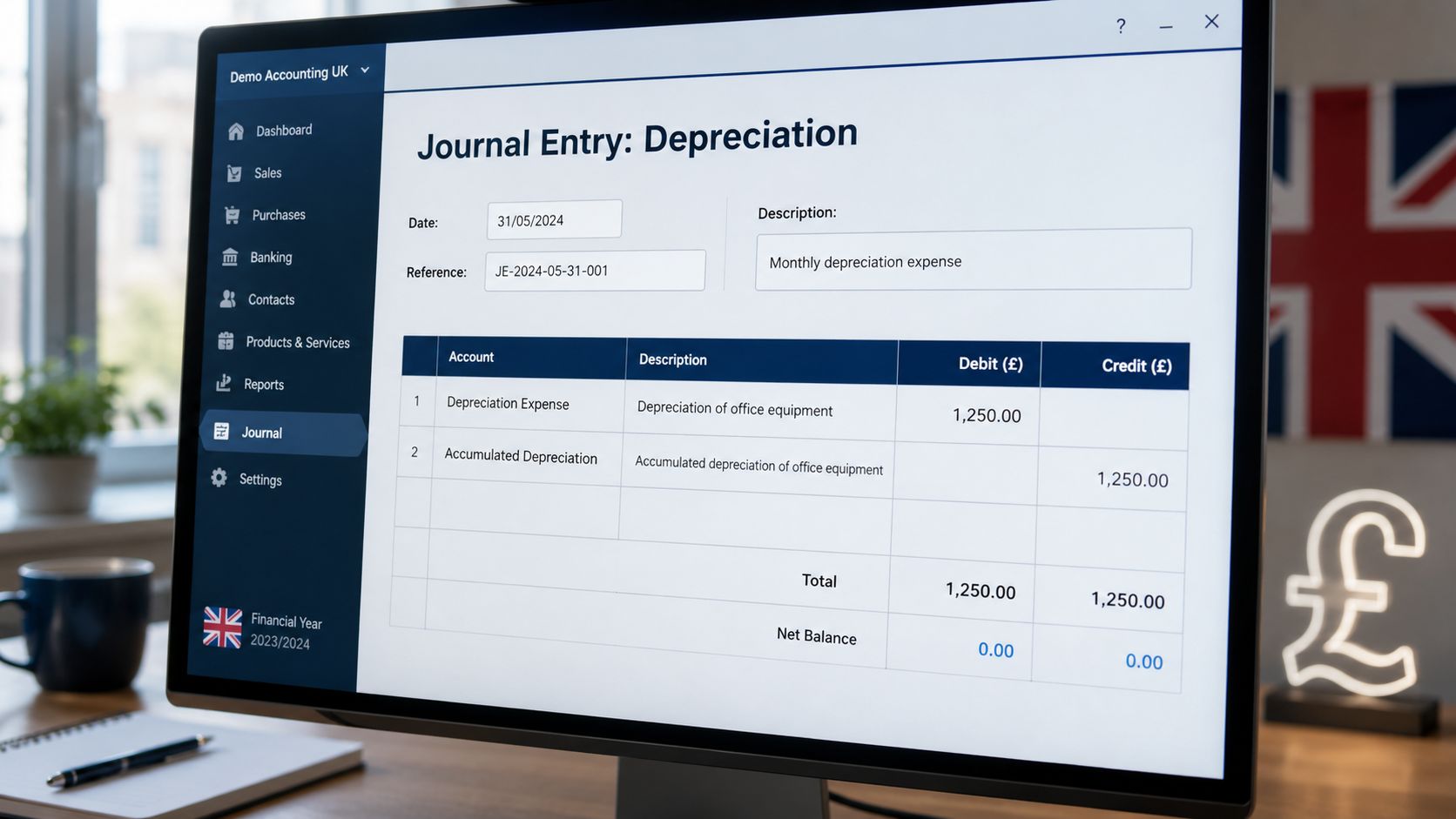

Recording Depreciation and UK Tax Considerations

Once you can calculate depreciation, the next job is recording it properly. Here, theory becomes bookkeeping.

The standard journal entry is:

- Debit Depreciation Expense

- Credit Accumulated Depreciation

That debit goes to the profit and loss account. It reduces profit for the period. The credit goes to the balance sheet as accumulated depreciation, which sits against the asset and reduces its carrying amount.

What the journal is doing

It helps to split the accounting effect into two views:

| Where it appears | Account | Effect |

|---|---|---|

| Profit and loss | Depreciation expense | Reduces profit |

| Balance sheet | Accumulated depreciation | Reduces asset carrying value |

That is why depreciation matters so much in final accounts training. It doesn't just change one report. It changes both.

Depreciation is not the same as tax relief

This point is essential for UK trainees. Accounting depreciation is used for preparing the accounts. Capital allowances are used for tax. They are not the same thing.

You may hear people mention Annual Investment Allowance and other tax treatments in practice. That is part of tax computation, not the depreciation journal itself. As your role develops, you'll need to understand both systems and keep them clearly separate.

For anyone who wants to see where this knowledge can lead, specialist roles in capital allowances are a real career path. This Associate Director job at Grant Thornton gives a useful sense of how technical asset knowledge can develop into a more advanced specialism.

Why VAT and digital compliance still matter here

Depreciation itself isn't a VAT calculation, but the asset purchase and the records around it often sit inside the same finance workflow. In the UK, the VAT registration threshold is £90,000, and businesses above that level must register for VAT and comply with Making Tax Digital requirements, including digital VAT submissions through approved software, as explained in this VAT training overview.

That matters because many Accounts Assistants handle both asset records and VAT routines. If you're processing fixed asset purchases, you also need to understand how those entries fit into the wider bookkeeping system.

To strengthen that bigger picture, this guide on how to prepare financial statements is a helpful follow-on resource because it shows how journals like depreciation feed into the year-end accounts.

Automating Depreciation in Xero Sage and QuickBooks

Manual calculation teaches the logic. Software applies it consistently. In practice, you need both.

Modern accounts teams often use Xero, Sage, and QuickBooks to maintain a fixed asset register and post depreciation automatically. The workflow is usually straightforward once you understand the accounting behind it.

What you typically enter in software

Most systems ask for the same core details:

- Asset cost at purchase

- Purchase or in-service date

- Depreciation method

- Useful life or depreciation rate

- Residual value, where relevant

Once that setup is complete, the system calculates the recurring depreciation and posts the journals according to the schedule.

Why manual understanding still matters

Automation doesn't remove the need for judgement. It just speeds up the posting.

If the useful life is wrong, the software will process the wrong number perfectly every month. If the method is wrong, the reports will still look polished. That is why employers value trainees who can test the output rather than accepting it as presented.

A good practical habit is to do a manual check for one period and compare it to the software result. That helps you catch setup errors early.

The digital skills employers expect

Making Tax Digital for VAT requires businesses to keep digital records and submit VAT returns through HMRC-approved software such as Sage, Xero, or QuickBooks, and FC Training notes that these tools are built into UK professional careers training, with the first MTD VAT submission deadline for eligible businesses falling on 7 August 2026.

That doesn't mean depreciation and VAT are the same task. It means modern finance roles are increasingly software-led. An Accounts Assistant, business analyst, or data analyst who understands both accounting logic and digital systems is far more useful than someone who knows only one side.

If you're building hands-on software confidence, this walkthrough on how to use Xero accounting software is a useful practical companion.

Next Steps for Your Accounting Career

Depreciation looks like a narrow topic at first. It isn't. It connects bookkeeping, final accounts, management reporting, software setup, and analytical thinking.

If you're aiming for an Accounts Assistant role, you need to calculate it, post it, and explain it. If you're moving into business analyst or data analyst work, you need to read it properly so you don't misinterpret trends in profit and asset values. If you're studying bookkeeping and VAT or advanced payroll, it strengthens your confidence with double entry and month-end processes.

Why exam success depends on practical understanding

Under the AAT framework, Accounts Assistant qualifications require practical competence in bookkeeping, VAT returns, and payroll, and AAT states that assessments include VAT calculations, tax point decisions, and application of the 20% standard, 5% reduced, and 0% exempt VAT rates in scenarios designed to reflect real work, including final accounts and financial data interpretation.

That tells you something important. Employers and awarding bodies both expect applied knowledge, not memorised definitions.

Three short practice prompts

Try these on paper before using a calculator:

Straight-line practice

A business buys an asset for £40,000, expects a £4,000 residual value, and plans to use it for 10 years. What is the annual depreciation charge?Reducing balance practice

An asset has an opening net book value of £3,000 at the start of the year. If the depreciation charge for that year is £1,200, what is the closing net book value?Journal practice

When you record depreciation for the period, which account is debited and which account is credited?

Write out the full answer, not just the number. That habit builds exam technique and workplace confidence.

The trainees who progress fastest are usually the ones who practise the journal entry as often as the formula.

Building a route into the job market

If you're still mapping your career options, this Snyp's guide for UK accounting is a useful read because it shows the kinds of roles and entry routes learners often consider when moving into the profession.

Structured training helps because it turns isolated topics into a joined-up skill set. Depreciation makes much more sense when you learn it alongside bookkeeping and VAT, final accounts, payroll processes, and software work in Xero, Sage, and QuickBooks. That mix is what turns study into job readiness.

If you want guided support with bookkeeping and VAT, accounts assistant training, final accounts, advanced payroll, or practical software skills in Sage, Xero, and QuickBooks, Professional Careers Training offers flexible training with 1-to-1 support from ACCA qualified Chartered Accountants and CPD approved trainers, plus software support, official certification pathways, and recruitment-focused help with CV preparation, LinkedIn optimisation, and job search strategy.