You've got the degree. You've done the exams. You know what accruals, control accounts, variance analysis, and ratio interpretation mean. Then you open job boards...

Your first Companies House deadline often feels bigger than it should. You've got bookkeeping records to tidy, VAT dates to watch, payroll questions landing in your inbox, and then someone asks, “Have the accounts been filed yet?” That's the moment many trainees realise compliance isn't a side task. It's part of the job.

If you want to work in bookkeeping, as an accounts assistant, in final accounts, or move into business analyst or data analyst roles, Companies House filing is worth learning properly. It teaches accuracy, deadlines, document handling, software use, and data checking. Those are the habits employers look for because they reduce risk and keep businesses organised.

Why Mastering Companies House Filing Boosts Your Career

A trainee in their first office role usually starts with the basics. They post invoices, reconcile bank entries, check ledgers, and help prepare VAT records. Then a manager asks them to help with a Companies House filing. At that point, the task stops being theoretical. The filing has a legal deadline, the figures must match the records, and one wrong choice can create delays or penalties.

That pressure is why this skill matters so much. It sits at the point where bookkeeping turns into compliance work.

Why employers value this skill

The scale of UK company activity is enormous. In the financial year ending March 2025, the total Companies House register size reached 5,427,787 companies, which shows how much demand there is for people who can handle compliance accurately and efficiently, according to Companies House register activity statistics.

A business owner might see filing as an annual obligation. An employer sees it differently. They see a process that needs someone who can:

- Read financial information clearly and spot gaps before submission

- Keep to deadlines without constant supervision

- Use filing systems and software with confidence

- Handle changes properly when directors, addresses, or share details are updated

- Protect data quality so reports are reliable later

Those are transferable skills. They support bookkeeping and VAT work, accounts assistant duties, final accounts preparation, and analytical roles where clean business data matters.

How filing knowledge strengthens your training path

A good training route doesn't treat Companies House filing as a separate topic. It links it to the work you'll perform. In bookkeeping and VAT study, you learn how source records feed into reports. In final accounts training, you learn how year-end figures are structured. In accounts assistant work, you learn how to gather the right evidence and support senior staff. In business analysis and data analysis, you learn why consistent records matter before anyone can produce useful insight.

Career point: A trainee who can explain both the filing step and the reason behind it is more useful than someone who only knows which button to press.

If you're still deciding where to start in finance, this practical side of compliance often helps people choose a path. It gives structure to the theory covered in guidance on getting into accounting, and it shows how daily finance tasks connect to formal reporting.

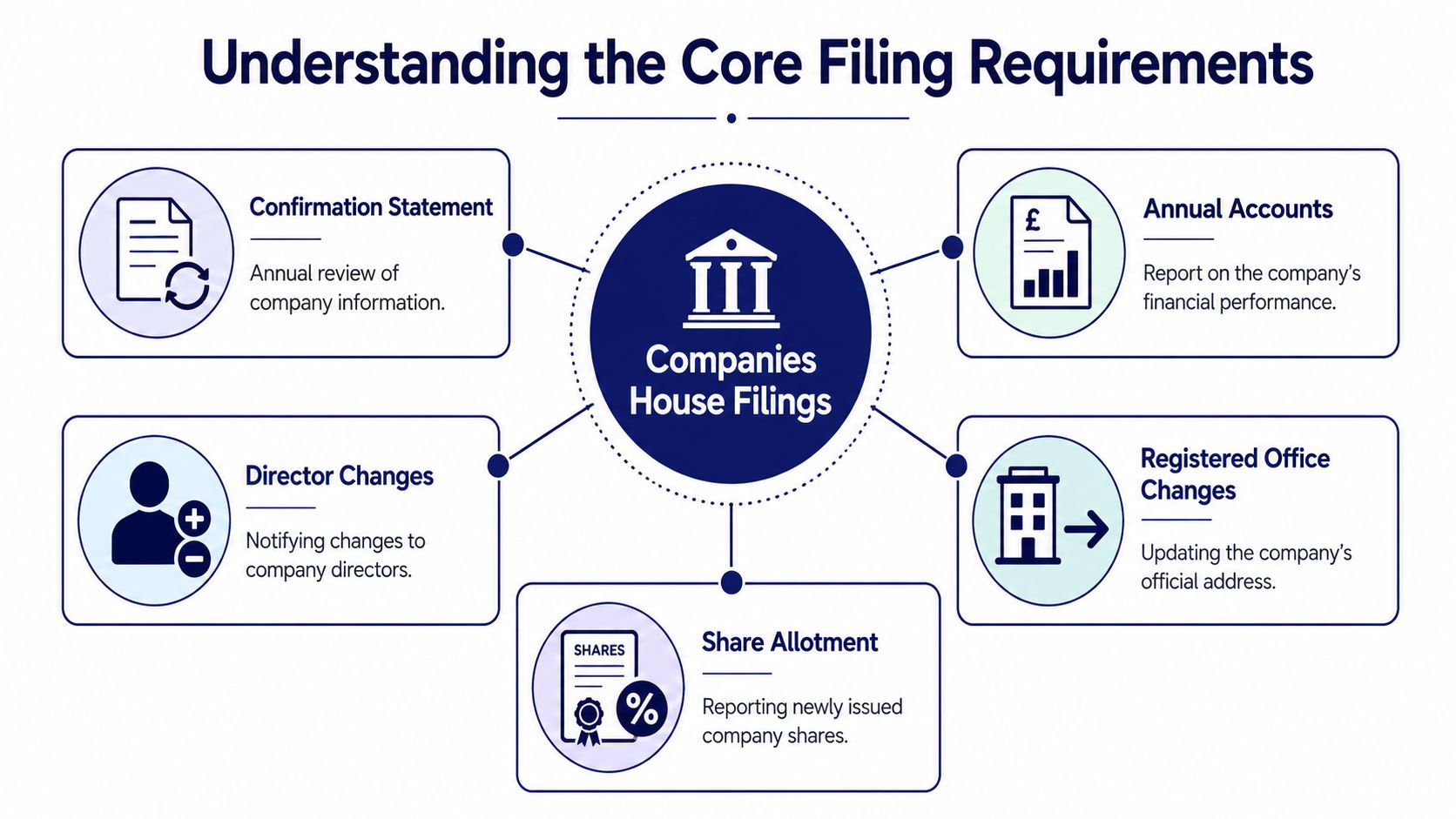

Understanding the Core Filing Requirements

Most learners get confused because they hear “Companies House filing” as if it's one document. It isn't. It's a group of obligations. Some happen every year. Others happen only when company details change.

The easiest way to understand it is to link each filing to its purpose and the job role that usually supports it.

The main filings most trainees encounter

Confirmation Statement

This confirms that the company information on the public register is up to date. It isn't mainly about profit or tax. It's about company identity and ownership details. An accounts assistant or office administrator may help gather the information, while a director approves what's submitted.

Annual Accounts

Within Annual Accounts, many trainees first feel the link between bookkeeping and statutory reporting. The company's records need to be complete enough for accounts to be prepared in the correct format. That's why final accounts training matters. It teaches you how ledgers become financial statements.

Director changes

If a director is appointed, resigns, or their details change, the company needs to notify Companies House using the correct route. This is a governance task, but finance teams often notice the change first because they handle records, payroll setup, or expense approvals.

Registered office changes

This sounds simple, but it matters. The registered office is the official company address for notices and formal correspondence. If it's wrong, important documents can go to the wrong place.

Share allotment

When a company issues new shares, that change must be reported properly. This tends to involve company administration, but anyone in accounts or business analysis should understand what it means because it affects ownership and company records.

A useful way to reinforce this knowledge is by studying how to prepare financial statements, because it helps you see how filing obligations connect to real accounting work.

Where VAT knowledge fits in

Many trainees think VAT belongs only to HMRC and not to Companies House work. In practice, the skills overlap. When you prepare accounts, you need disciplined records. VAT training builds that discipline.

Businesses must submit VAT returns and payments on time, typically one month and seven days after the accounting period ends, and the standard 20% VAT rate applies to most goods, as explained in VAT training guidance.

That matters because a bookkeeper who understands VAT timing and record quality is usually better prepared to support year-end accounts too.

Here's a simple way to think about the link:

- Bookkeeping and VAT training builds record accuracy

- Accounts assistant training builds document handling and reporting support

- Final accounts training builds understanding of year-end presentation

- Advanced payroll training builds confidence with regulated deadlines and data accuracy

- Business analyst and data analyst training builds skill in checking, structuring, and interpreting company information

A short explainer can help if you prefer visual learning before reading the rules in detail.

Filing work looks administrative from the outside. In practice, it trains judgement, sequencing, and accountability.

The Filing Process A Step-By-Step Walkthrough

It is 4:30 pm on a filing deadline day. The accounts are drafted, but nobody can find the authentication code, the accounting period has not been checked, and the person preparing the submission is still unsure which account type applies. That kind of pressure is rarely caused by the website itself. It usually starts earlier, in the preparation stage.

For trainees, Companies House filing transforms from an admin task into a career skill. A good filer follows a sequence, understands why each check matters, and can explain the risk if a step is missed. That is the kind of judgement employers notice in bookkeeping, accounts support, and finance analysis roles.

Start with the records, not the portal

Online filing is the final stage. The actual work begins in the records.

Before anyone logs in, the bookkeeping should be complete, the year-end figures should agree to the underlying records, and the balance sheet and related disclosures should match the filing route the company is allowed to use. Filing with weak records is like building from the roof down. The submission may go through, but the logic underneath is unstable.

A frequent training issue is account type selection. A learner may know the numbers but still choose the wrong category, such as micro-entity accounts where a different option applies. Final accounts training helps here because it teaches you how presentation follows the reporting framework. In other words, you are not only entering figures. You are classifying them correctly for a legal purpose.

Get access in place early

Access problems can stop an otherwise accurate filing.

To file online, directors need access through GOV.UK One Login, which is set to become mandatory from 13 October 2025, and filings use a 6-character alphanumeric company authentication code, according to the official online filing guidance.

If you support a client or your employer, ask for the authentication code well before the deadline window. This small habit shows professional discipline. It is also the same habit used in payroll, VAT, and month-end work. Controlled access, clear ownership, and early checks reduce last-minute errors.

A practical filing sequence looks like this:

- Confirm the accounting reference date so the filing period is correct.

- Finish the bookkeeping and year-end accounts before starting the submission.

- Check login access and the authentication code in advance.

- Select the correct account type before entering or uploading figures.

- Review the submission carefully before sending it.

That order matters. It saves time because each step depends on the one before it.

Use the online route as your standard process

Online filing is usually the working method trainees should expect to use. It is faster than paper, easier to track, and better suited to modern accounting workflows. Companies House also expects a stronger digital filing process over time, with a mandatory move to iXBRL via commercial software planned from 1 April 2028.

That has a clear training implication. Software knowledge belongs inside compliance work.

If you can prepare records, check classifications, and submit through approved software, you become more useful than someone who only understands manual filing steps. Bookkeepers need that skill to keep records submission-ready. Accounts assistants need it to support directors and practice managers. Business analysts benefit too, because filing depends on structured, consistent data.

Keep the deadline visible from the start

Accounts must be filed on time. For a private company, the usual deadline is 9 months after the financial year end. Late filing can trigger automatic penalties, and repeated late filing can increase the cost.

| How Late | Penalty |

|---|---|

| Up to 1 month late | £150 |

| 1 to 3 months late | £375 |

| 3 to 6 months late | £750 |

| More than 6 months late | £1,500 |

Strong trainees do not treat the deadline as a date to remember at the end. They treat it as a date to plan backwards from.

For example, if the filing deadline is at the end of December, a careful preparer will ask much earlier: when will bookkeeping be complete, when will the accounts be reviewed, who approves them, and who holds the authentication details? That is how filing turns into risk control. It also explains why this topic fits so well with bookkeeping courses, final accounts training, and data-focused finance roles. The process teaches sequencing, accuracy, and accountability all at once.

Why this walkthrough matters in practice

Each step in the filing process builds a skill employers can use:

- Bookkeeping roles need records that support filing without guesswork.

- Accounts assistant roles need document control, review discipline, and deadline tracking.

- Final accounts roles need confidence in classification, disclosure, and presentation.

- Payroll and other compliance roles use the same habits of timing, identifiers, and accuracy.

- Business analyst and data analyst roles benefit from structured data, validation, and consistency checks.

That is why Companies House filing deserves serious attention in training. It teaches you how to prepare information, test it, and submit it in a way that stands up to scrutiny.

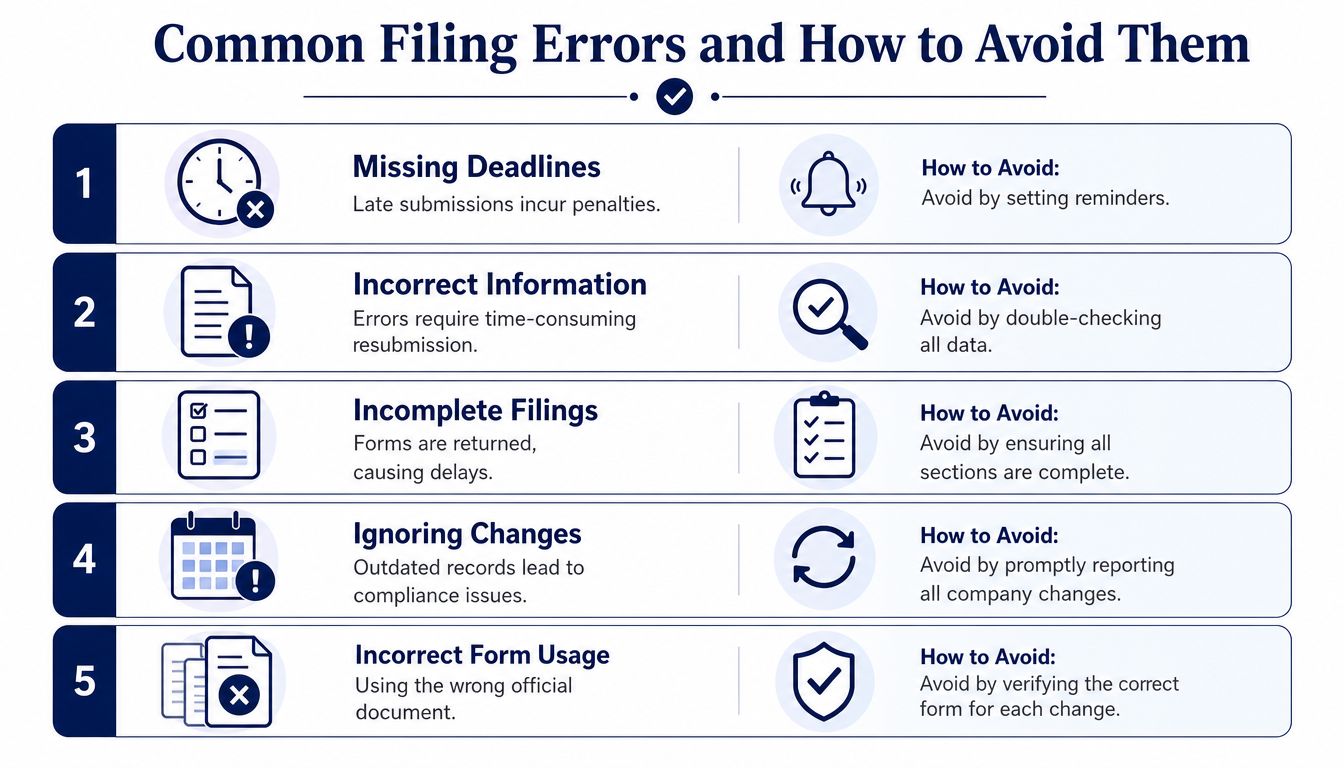

Common Filing Errors and How to Avoid Them

Most filing mistakes aren't caused by complex law. They happen because someone assumes a detail is obvious, skips a check, or uses old information. Good training helps you catch those errors before submission.

Errors that usually catch beginners

One classic mistake is using the wrong accounting period. A trainee may open the working papers from last year and assume the dates roll forward neatly. They don't always. If the accounting reference date has changed, the whole filing can be wrong from the start.

Another common error is picking the wrong filing type. This often happens when the preparer knows the bookkeeping but doesn't yet understand the reporting framework. The result is confusion, rejected work, or a need to recheck the entire submission.

Authentication issues also waste time. The company authentication code may be missing, entered incorrectly, or held by someone who is away when the filing is due. This doesn't sound technical, but it can stop the process completely.

A professional approach to prevention

The best trainees build small checks into their routine:

- Check dates first so the filing period and deadline match the company records.

- Confirm the company category before preparing or selecting the accounts format.

- Test access early rather than on the day of submission.

- Review company changes such as directors or addresses before assuming the register is current.

- Read the final screen carefully because many errors are visible just before submission.

These are the habits that separate a careful accounts assistant from someone who only follows instructions.

A filing error often starts weeks earlier, when nobody checked the underlying records.

Why structured training helps

Courses in bookkeeping and VAT teach the discipline of reconciliations and cut-off checks. Final accounts training teaches how classifications affect presentation. Advanced payroll teaches deadline awareness and the need for exact employee and company data. Business analyst and data analyst training sharpen another valuable habit, which is testing whether the data structure makes sense before relying on it.

That mix matters because companies house filing isn't only about forms. It's about control.

A simple error review can look like this:

| Error | Likely cause | Better habit |

|---|---|---|

| Wrong filing period | Old working papers reused without review | Check accounting reference date first |

| Wrong accounts type | Weak understanding of company status | Confirm filing basis before preparation |

| Failed login or code issue | Access left until deadline week | Test credentials early |

| Outdated company details | Internal changes not reported promptly | Reconcile register details before filing |

| Incomplete submission | Rushed final review | Pause and validate every screen |

Using Accounting Software for Seamless Filings

Modern compliance work sits inside software. A trainee who can use Xero, Sage, or QuickBooks well isn't just posting transactions faster. They're building the records that support filing, VAT work, management reporting, and year-end preparation.

That's why digital skills matter so much in bookkeeping and VAT training. They affect what happens long before a Companies House submission is made.

Why software knowledge now matters more

The UK's Making Tax Digital (MTD) initiative mandates that VAT-registered businesses keep digital records and submit VAT returns using approved software, which is why learners often take focused training such as the Making Tax Digital bookkeeping and VAT course.

Once you understand that, the wider picture becomes clear. Digital records feed VAT returns. Those same records support accounts preparation. Accounts preparation supports filing. It's one connected workflow.

If you're building software confidence, practical guidance on software for business accounts can help you compare the everyday strengths of different systems.

What trainees should learn inside the software

Focus on tasks that mirror real work:

- Bank reconciliation so ledger balances are trustworthy

- VAT coding so transactions feed the right return treatment

- Chart of accounts review so reports are meaningful

- Year-end adjustments so final figures are not distorted

- Export and reporting functions so data can move into filing or analysis tasks

This is also where analytical thinking starts to grow. A future business analyst or data analyst often begins by learning how business systems store information and where errors creep in.

For readers comparing finance software across markets, top software for managing UAE business finances offers a useful cross-market view of how platforms are chosen for compliance, reporting, and daily control. The country context is different, but the logic behind software selection is familiar.

Strong software users don't just enter data. They understand what the system is preparing the business to report later.

Future-Proof Your Skills for Tomorrow's Compliance

A lot of public guidance still treats filing as if the current system will stay the same. It won't. The direction of travel is toward simpler submission for businesses, but that simplicity at the front end increases the need for data quality behind the scenes.

A major 2024-2025 reform proposes allowing companies to file accounts 'once only' with the government. This shift means future professionals, including business and data analysts, will need skills to manage and interpret this unified data, as noted in RossMartin's summary of the Companies House changes.

Why this changes career opportunities

If one filing can feed multiple government uses, then poor data becomes a bigger problem. An error doesn't stay in one place. It travels. That means future employers will need people who can check source data, understand system logic, and question inconsistencies before submission.

Traditional finance training and analytical training converge. A bookkeeper or accounts assistant who understands records and controls already has part of the foundation. Add business analysis skills, and you can map processes and spot failure points. Add data analysis skills, and you can test patterns, clean datasets, and support better decisions.

That's also why behavioural thinking matters in compliance work. People don't always make errors because they lack knowledge. Sometimes they follow habits, assumptions, or shortcuts. Synopsix's analysis of behaviour is a useful read if you want to think more about why people comply, where they merely conform, and how that affects process design.

Build a skill set that lasts

A durable training plan usually combines:

- Bookkeeping and VAT for record accuracy and tax awareness

- Advanced payroll for deadline discipline and regulated processing

- Accounts assistant skills for document handling and practical office workflows

- Final accounts knowledge for year-end preparation and reporting structure

- Business analyst tools for process mapping and requirements thinking

- Data analyst tools for cleaning, checking, and interpreting structured information

There's also a direct earnings reason to take this seriously. Junior bookkeepers in the UK earn an average of £25,000 per year, while senior bookkeepers can earn up to £40,000 annually, according to current bookkeeping salary information. Better skills create better options.

The same principle applies to entry pathways. UK bookkeeping qualifications can take between six weeks and six months to complete, and there are no mandatory entry requirements for candidates pursuing ICB bookkeeping qualifications, as outlined by AAT qualifications and courses. That makes this a realistic route for recent graduates, career changers, and professionals who need practical CPD.

If you want structured, job-ready training in bookkeeping and VAT, advanced payroll, accounts assistant work, final accounts, business analysis, or data analysis, Professional Careers Training offers flexible study with support from qualified trainers, software training in Sage, Xero, and QuickBooks, and career-focused help with CV preparation, job search strategy, LinkedIn optimisation, and employer referrals.