The gap between an average salary and top-end salaries in the UK is wide. The Office for National Statistics reports that full-time weekly earnings remain...

Why the Cash Flow Statement Is So Important

Before we jump into the numbers, it’s crucial to understand what a cash flow statement really does and why mastering it is a core skill for any UK finance professional. Think of it as the story of your company’s cash. Unlike the income statement, which shows profit, this report reveals your actual ability to pay bills, fund operations, and invest in the future.

Here’s a critical distinction that trips up many people: profit isn’t the same as cash. A business can look profitable on paper due to accrual accounting but lack the physical cash to pay suppliers or staff. Understanding this is essential for sound financial analysis and a core concept in our bookkeeping & VAT training.

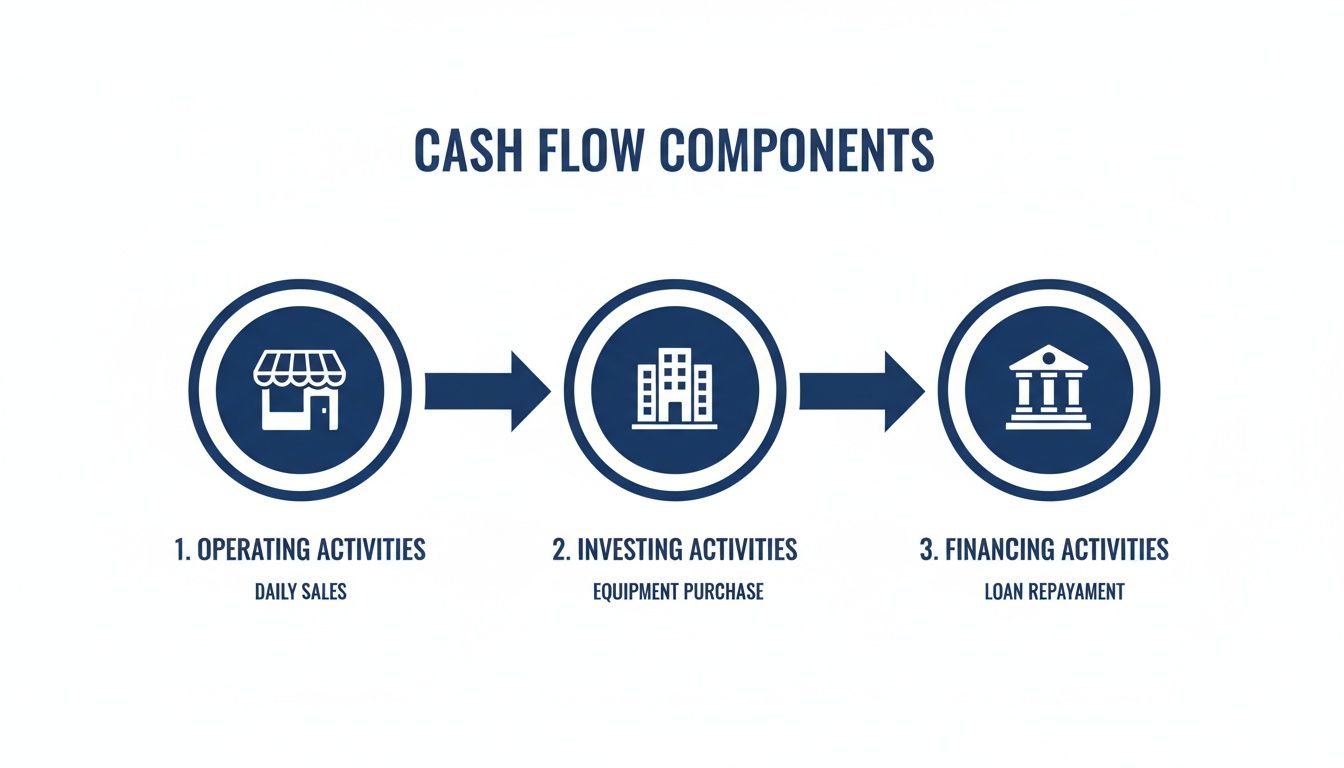

The Three Core Components of Cash Flow

Every cash flow statement is broken down into three main sections. Each one tells a different part of your financial story.

To make this clearer, here’s a quick summary of what each activity section reveals about a business’s financial health.

| Activity Section | What It Shows | Typical UK Examples |

|---|---|---|

| Operating Activities | Cash generated from your primary, day-to-day business operations. | Revenue from sales, payments to suppliers, employee wages, rent payments. |

| Investing Activities | Cash used for or generated from long-term assets and investments. | Buying new machinery, selling an office building, purchasing shares in another company. |

| Financing Activities | Cash movements between a company and its owners or creditors. | Taking out a bank loan, repaying debt, issuing new shares, paying dividends. |

A healthy business will typically generate positive cash flow from its operating activities, which then funds its investing and financing needs.

The diagram below shows how these three components work together to provide a complete picture of a company’s cash movements.

This visual flow really highlights how day-to-day operations, long-term investments, and funding decisions all feed into the overall cash position of the business.

Direct vs Indirect Methods

When it comes to preparing the statement, you have two approaches: the direct and indirect methods.

The direct method lists all cash receipts and payments, giving a very straightforward view of where cash came from and went. It’s clear, but it requires incredibly detailed tracking of every single transaction.

The indirect method, on the other hand, starts with the net income figure from the profit and loss statement and then adjusts for non-cash items (like depreciation) and changes in working capital. This is why most UK businesses prefer it—it’s generally simpler to prepare using existing financial statements.

To see how these concepts play out in a real-world context, it’s worth reviewing a detailed example of a cash flow statement.

Getting to grips with this foundational report is the first step towards creating comprehensive financial reports. It’s a skill you can build on as you learn more about how to prepare financial statements.

Using the Indirect Method to Prepare Your Statement

For most UK companies, the indirect method isn’t just an option—it’s the standard way to prepare a cash flow statement. If you’re aiming for a role as a bookkeeper, payroll specialist, or accounts assistant, getting this right is non-negotiable. It’s the skill that connects a company’s reported profit with its actual cash in the bank. This isn’t just theory; let’s walk through how it works in practice.

Unlike the direct method where you track every single cash transaction, the indirect approach starts with the net profit from the income statement. From that number, we’ll make a series of adjustments to strip out non-cash items and factor in changes in working capital. What you’re left with is the real net cash generated from day-to-day operations.

Starting with Net Profit

Your starting point is always the bottom line of the income statement. This figure is based on accrual accounting, which means it includes revenues you’ve earned and expenses you’ve incurred, whether or not the cash has actually changed hands. Our job is to work backwards from this profit number to find the true cash position.

Let’s use a simple example: a growing UK-based SME called “Crafty Mugs Ltd.” They’ve reported a £50,000 net profit for the year. That looks great on paper, but it doesn’t tell us how much cash they actually have from their core business activities.

To get the full story, we need to adjust for all the items that hit the profit figure but didn’t involve an immediate cash exchange. This reconciliation is a fundamental skill you’ll develop in our final accounts training.

Adjusting for Non-Cash Expenses

First, we need to deal with any expenses that reduced the net profit without actually using up cash. The most common one you’ll come across is depreciation.

When Crafty Mugs Ltd. bought a new kiln, they didn’t expense the full cost on the income statement right away. Instead, they recorded a depreciation expense to spread that cost over the kiln’s useful life.

- Depreciation: Let’s say they recorded £5,000 in depreciation this year. This expense lowered their profit, but no cash actually left the business for it. So, we need to add it back.

- Amortisation: This is the same principle but for intangible assets, like a patent. If they had an amortisation charge, you’d add that back too.

By adding back these non-cash expenses, you begin to reverse the effects of accrual accounting. You are essentially saying, “This expense was recorded for profit calculation, but it didn’t use any of our cash, so let’s add it back to our cash total.”

This isn’t just something for small businesses. Look at the UK Statistics Authority’s Annual Report for 2024/25. It shows a net expenditure of £383,270,000, which was adjusted by £14,017,000 in non-cash items to get closer to the real operational cash flow. It’s a perfect real-world example of how vital these adjustments are. You can explore the full report on the UKSA website for more context.

Accounting for Changes in Working Capital

Next up, we have to look at the changes in current assets and current liabilities from the start of the year to the end. This is where having a solid grasp of the balance sheet is crucial. If you’re feeling a bit rusty, it’s worth taking a moment to review how to read balance sheets.

These adjustments for working capital show us where cash has been either tied up or freed up in the daily running of the business. This is a core competency for any accounts assistant.

Here’s the logic behind each adjustment:

- Increase in a Current Asset (e.g., Accounts Receivable): If Crafty Mugs’ accounts receivable increased by £10,000, it means they sold more on credit than they collected in cash. That revenue is in the net profit figure, but the cash hasn’t landed yet. We have to subtract this increase.

- Decrease in a Current Asset (e.g., Inventory): If their inventory dropped by £3,000, it means they sold more stock than they bought. Selling inventory turns it into cash (or a receivable), so this frees up cash. We add this decrease back.

- Increase in a Current Liability (e.g., Accounts Payable): If their accounts payable went up by £7,000, they’ve bought goods or services but haven’t paid their suppliers yet. This is like a short-term loan that has preserved their cash. We add this increase.

- Decrease in a Current Liability (e.g., Accrued Expenses): If they paid off a liability, causing it to decrease, actual cash has left the business. This decrease must be subtracted.

Bringing It All Together for Crafty Mugs Ltd.

Let’s pull all these numbers together and calculate the net cash from operating activities for our example company.

| Description | Amount (GBP) | Calculation Step |

|---|---|---|

| Net Profit | £50,000 | Starting Point |

| Add: Depreciation | £5,000 | Add back non-cash expense |

| Subtract: Increase in Accounts Receivable | (£10,000) | Cash not yet received from sales |

| Add: Decrease in Inventory | £3,000 | Cash freed up from selling stock |

| Add: Increase in Accounts Payable | £7,000 | Cash saved by delaying payments |

| Net Cash from Operating Activities | £55,000 | Final Figure |

There you have it. Even though Crafty Mugs Ltd. reported a profit of £50,000, the business actually generated £55,000 in cash from its operations. This is precisely why the indirect method is so powerful for analysts and accounts assistants—it reveals the true story behind the numbers. Getting this process down is a huge step toward being fully job-ready.

Exploring the Direct Method and When to Use It

While the indirect method is the favourite for most UK businesses, a complete finance professional understands both approaches. Knowing how to prepare a cash flow statement using the direct method gives you a much more transparent, granular view of a company’s actual cash movements—a skill particularly valued in roles like business analyst and data analyst where forecasting is key.

This approach is, in principle, far more straightforward. Instead of starting with net profit and making adjustments, you simply total up all cash receipts from customers and then subtract all cash paid out for expenses. Think of it as looking directly at the bank statement and categorising every single transaction.

How the Direct Method Works

The goal here is to present the gross cash receipts and payments for the period. It offers a clear breakdown of where money truly came from and where it went, without the cloud of accrual accounting adjustments getting in the way.

Here’s a look at the main categories you would track:

- Cash received from customers: The actual money collected from sales.

- Cash paid to suppliers: Payments made for inventory and other goods.

- Cash paid to employees: Salaries, wages, and other employee-related costs.

- Cash paid for other operating expenses: Rent, utilities, and marketing costs paid in cash.

- Interest paid: The actual cash outflow for interest on debts.

- Income taxes paid: The amount of tax actually paid to HMRC during the period.

This level of detail is incredibly useful for internal management. It can highlight potential issues—like a large gap between sales revenue and actual cash collected from customers—much faster than the indirect method ever could.

A Practical Example of the Direct Method

Let’s go back to our SME, “Crafty Mugs Ltd.” Using the direct method, we would ignore their reported profit and instead dig right into their cash records for the year. The preparation would look something like this.

| Cash Flow Category | Amount (GBP) | Description |

|---|---|---|

| Cash Inflows | ||

| Cash collected from customers | £200,000 | Total payments received from sales. |

| Cash Outflows | ||

| Cash paid to suppliers | (£80,000) | Payments for clay, glazes, and packaging. |

| Cash paid to employees | (£50,000) | Wages for potters and admin staff. |

| Cash paid for operating costs | (£15,000) | Rent for the studio and utility bills. |

| Net Cash from Operating Activities | £55,000 | Total Inflows – Total Outflows |

You’ll notice the final figure, £55,000, is exactly the same as the one we calculated using the indirect method. Both paths lead to the same destination, but they tell the story in a very different way. The direct method provides a clear, itemised report of cash transactions, while the indirect method shows the reconciliation between profit and cash.

When Is the Direct Method the Better Choice?

So if it’s more work, why would anyone use it? The direct method is often preferred by organisations that need a very clear picture of their short-term liquidity and for cash flow forecasting.

The transparency of the direct method is its greatest strength. It shows the actual sources and uses of cash without any accounting adjustments, which can make it easier for non-accountants to understand and for data analysts to build more accurate future cash flow models.

It’s particularly useful for:

- Internal management reporting: To monitor cash collections and payments closely.

- Non-profit organisations: Where tracking cash from donations and grants is critical.

- Businesses with tight cash flow: Who need to manage their daily liquidity with precision.

The main challenge, and the reason it’s less common, is the data collection. It requires meticulous tracking of every cash transaction. However, this is where practical training in accounting software becomes invaluable. Properly configuring software like Sage 50, a key skill taught in our advanced payroll courses, can automate much of this categorisation, making the direct method far more achievable for businesses that need its clarity.

Analysing Investing and Financing Cash Flows

While operating activities tell you about a company’s day-to-day financial health, its long-term vision is written in its investing and financing activities. Moving beyond daily operations, this is where you’ll learn to classify and report the strategic cash movements that shape a company’s future—a vital skill for preparing any UK business’s cash flow statement.

This kind of analytical mindset is exactly what employers look for in business analyst and data analyst roles, where understanding how capital is raised and deployed is key to providing strategic insight. It’s where you see the big-picture decisions being made.

Decoding Investing Activities

The investing activities section is all about a company’s long-term assets. Think of it as a record of the major strategic purchases and sales a business makes to grow or streamline its operations.

Now, a negative cash flow here isn’t necessarily a bad sign. In fact, for a growing company, it’s often a positive indicator. It shows the business is reinvesting its cash into assets that will generate future income.

Common cash flows from investing activities include:

- Purchase of Property, Plant, and Equipment (PP&E): When a company buys a new office, machinery, or delivery vans, this is a cash outflow. It represents a significant capital expenditure aimed at expansion.

- Sale of Assets: Conversely, if a business sells an old building or surplus equipment, the cash received is recorded as an inflow.

- Purchase or Sale of Investments: This includes buying shares in another company or selling off existing securities.

For example, a UK manufacturing firm might show a large cash outflow from investing activities after purchasing a new automated assembly line. While this drains cash in the short term, it’s an investment intended to boost productivity and profitability for years to come.

Unpacking Financing Activities

The financing activities section tells the story of how a company raises capital and pays back its investors and creditors. It shows the flow of cash between the business and its owners and lenders, directly reflecting decisions about its capital structure.

Analysing this section helps you understand a company’s financial leverage and its policies on returning value to shareholders. It provides clear insights into how the business is funding its operations and growth.

Key transactions you will report here are:

- Issuing Shares: When a company sells new shares to investors, the cash received is a significant inflow.

- Repaying Debt: Making payments on a bank loan is a cash outflow.

- Taking on New Loans: The proceeds from a new business loan are recorded as a cash inflow.

- Paying Dividends: Distributing profits to shareholders is a common cash outflow that shows a return to investors.

Understanding these flows is critical. For instance, a tech start-up might show a large cash inflow from issuing shares to fund R&D, while a mature, stable company might show consistent outflows from paying dividends and repaying long-term debt.

When you prepare a cash flow statement, the investing and financing sections provide a narrative. Investing activities show where the company is placing its bets for future growth, while financing activities reveal how those bets are being funded.

The timing and scale of these activities can get pretty complex. Just look at HMRC’s 2024-25 Annual Report, which details payables and accrued revenue of £8.2 billion, with huge portions tied to long-term liabilities like legal claims. The report also shows specific financing outflows, such as a £333 million net payment to the Isle of Man. These figures show just how crucial accurate cash flow analysis is at every level. You can discover more about these public sector financial details.

Practical Scenarios for Classification

Let’s ground these principles with a real-world example. Imagine a UK-based logistics company making some big moves.

- The company sells one of its older warehouses for £500,000. This is the sale of a long-term asset, so the £500,000 is recorded as a cash inflow from investing activities.

- It then uses that money to help purchase a new, larger distribution centre for £1.2 million. The £1.2 million is a cash outflow under investing activities.

- To fund the remainder of the purchase, the company takes out a £700,000 business loan. This is a cash inflow from financing activities.

- At the end of the year, the company pays £25,000 in dividends to its shareholders. This is a cash outflow from financing activities.

By correctly classifying these transactions, the cash flow statement tells a clear story of the company’s strategy. It sold an underperforming asset, invested in a better one for future growth, and used debt to finance it, all while returning value to its shareholders. This level of analysis is exactly what employers look for in candidates with training for accounts assistant and advanced payroll roles.

How to Finalise and Review Your Statement for Accuracy

Getting the individual sections of your cash flow statement prepared is a huge step, but the job isn’t quite finished. For any professional handling final accounts, the review and reconciliation phase is where your work really proves its value.

A skilled accounts assistant or bookkeeper knows that an unchecked statement is a potential liability. Meticulous accuracy is what separates a draft from a reliable financial report, and this final step is where you tie everything together.

Performing the Final Reconciliation

The ultimate test of your cash flow statement’s accuracy comes down to a simple but powerful calculation. You need to sum the net cash flows from all three activities—operating, investing, and financing—to get the total net change in cash for the period.

This final figure shows you the total increase or decrease in cash the business has experienced. But how do you confirm it’s correct? You cross-reference it with your balance sheets.

The process is straightforward:

- Take the opening cash balance from the balance sheet at the start of the period.

- Add the net change in cash you just calculated from your cash flow statement.

- The result should precisely match the closing cash balance on the balance sheet at the end of the period.

If these figures align perfectly, you can be confident your statement is mathematically sound. This reconciliation proves that every cash movement has been accounted for, connecting the income statement and balance sheet into one cohesive story. It’s a fundamental skill we emphasise in our hands-on, CPD-approved training. If you want to explore this further, you can learn more about reconciliation in accounting in our detailed guide.

Cross-Referencing with Company Financials

This final check is standard practice for businesses of all sizes. Take PwC UK’s 2025 financial statements, for example. They report that their cash equivalents and deposits stood at £862 million, up from £773 million the previous year.

When finalising their statement of cash flows, their finance team would have performed this exact reconciliation. They would ensure the net change in cash calculated for the year perfectly explains the movement from £773m to £862m. It’s the final seal of approval, confirming your work is consistent with the other core financial reports.

Common Mistakes to Watch Out For

Even with the best intentions, errors can creep in. A thorough review means actively looking for the common pitfalls. Catching these mistakes before the report is finalised is the hallmark of a competent finance professional.

The review stage is not just about finding errors; it’s about validating the story the numbers are telling. Does the statement make sense in the context of the business’s activities for the period?

Here is a practical checklist to guide your final review:

- Misclassifying Transactions: Double-check that you haven’t put an investing activity in the financing section or vice versa. For instance, interest paid is typically an operating activity, while dividends paid are a financing activity.

- Mishandling Non-Cash Items: When using the indirect method, have you correctly added back all non-cash expenses like depreciation and amortisation to net profit? Forgetting these is one of the most frequent errors.

- Forgetting Changes in Working Capital: It’s easy to overlook movements in accounts receivable, accounts payable, and inventory. An increase in receivables, for example, must be subtracted from net profit.

- Inconsistent Data: Confirm that the figures you’ve used from the income statement and balance sheets are consistent and from the correct reporting periods. A simple typo can throw the entire reconciliation off.

- Ignoring Supplemental Disclosures: Some significant non-cash activities, like converting debt to equity, don’t appear in the main body of the statement. They must be disclosed in the notes to the financial statements, so make sure they haven’t been missed.

By methodically working through this checklist, you transform your cash flow statement from a draft into a reliable and accurate financial document, ready for stakeholders.

Still Have Questions About Cash Flow Statements?

Even after you get the hang of preparing a cash flow statement, a few questions always seem to pop up for aspiring accountants and bookkeepers. Honestly, understanding the nuances behind these reports is what separates a good analyst from a great one. Let’s tackle some of the most common queries I hear.

What Is the Main Difference Between a Cash Flow Statement and an Income Statement?

The biggest difference comes down to one thing: accrual vs. cash accounting.

Your income statement is built on accrual accounting. It records revenue the moment it’s earned and expenses as soon as they’re incurred—regardless of when money actually changes hands. This is why a company can look incredibly profitable on paper but have absolutely no cash in the bank.

A cash flow statement, on the other hand, sticks strictly to the cash basis. It tracks only the actual movement of cash in and out of the business. This gives you a true picture of a company’s liquidity and its real-world ability to pay its bills right now.

Why Is the Indirect Method More Common in the UK?

In the UK, the indirect method is king, and it really comes down to two things: it’s efficient, and it tells a better story. Firstly, it’s just simpler and cheaper to prepare. You’re using figures that are already sitting there on the income statement and balance sheet, so you don’t need a separate, detailed system to track every single cash transaction.

But more importantly, the indirect method provides a brilliant reconciliation between net profit and actual cash flow. This bridge helps analysts and managers see exactly why the profit figure doesn’t match the cash generated, shining a light on how non-cash expenses and changes in working capital have impacted things.

This reconciliation is a powerful analytical tool. It tells a story that the direct method can’t—the story of how a company’s day-to-day operational decisions and accounting policies affect its cash position.

How Does Software Training Help with Preparing These Statements?

Getting hands-on training with accounting software like Xero, Sage, or QuickBooks is essential because these platforms do the heavy lifting. Our certified courses in bookkeeping, final accounts, and for aspiring accounts assistants teach you how to set up your chart of accounts and classify transactions correctly from day one, which is the foundation of any accurate report.

While the software can generate a cash flow statement with a few clicks, its output is only as reliable as the data you put in. That’s where a trained professional comes in. You need someone who can:

- Ensure the underlying data is clean and correctly categorised.

- Interpret the final report in the context of what’s really happening in the business.

- Make any necessary adjustments for non-standard or unusual transactions.

Proper training transforms a complex manual chore into a streamlined, analytical process. It empowers you to provide valuable insights and strategic advice instead of just plugging in numbers, making you a far more valuable asset to any business.

At Professional Careers Training, we provide the practical skills you need to excel. Our 1-2-1 training with ACCA-qualified accountants on software like Xero and Sage will give you the confidence to prepare, analyse, and interpret financial statements like a seasoned professional. Explore our courses today to get started.