You're in Sage or Xero, posting routine entries, and one payment makes you pause. The supplier name doesn't match any regular trade creditor. You ask...

You're in Sage or Xero, posting routine entries, and one payment makes you pause. The supplier name doesn't match any regular trade creditor. You ask a colleague, and they say it's a business owned by the managing director's spouse. At that point, this stops being a simple purchase ledger task. It becomes a disclosure issue.

That's where International Accounting Standards 24, usually called IAS 24, matters. For many trainees, it first appears as an exam topic. In real work, it's much more practical than that. It helps you spot where business relationships could affect how accounts look, and it tells the finance team what must be disclosed so users of the financial statements can understand that risk properly.

If you're training in bookkeeping and VAT, advanced payroll, final accounts, accounts assistant work, or even business analysis and data analysis, IAS 24 teaches a habit that employers value. Don't just ask, “Has this been posted?” Ask, “Who is this with, and does that relationship matter?”

Why IAS 24 Matters for Your First Accounting Job

It is 4:45 pm on a month-end close day. You are in Sage or Xero, clearing the last few supplier invoices before the ledger is locked. One invoice looks normal on the face of it. Correct VAT code, approval in place, amount agrees to the paperwork. Then you notice the supplier is owned by a director's relative.

At that point, your job changes. You are no longer only posting an invoice correctly. You are helping the business decide whether the relationship behind that invoice needs to be disclosed in the financial statements.

That is why IAS 24 matters early in your career. It deals with related party disclosures, which means the accounts must show users where transactions and balances involve people or entities connected to the business. The bookkeeping entry may be routine. The relationship may not be. During final accounts preparation, that difference matters because readers need to understand where influence, control, or close connections could affect how transactions were agreed.

A good way to view IAS 24 is this. Double-entry records what happened. IAS 24 helps explain who it happened with, and why that could matter to someone reading the accounts. For a trainee, that is a big shift in thinking. You stop treating every invoice, journal, and balance as if it sits in isolation.

In day-to-day work, that shows up in practical tasks:

- While posting invoices in Sage or Xero: check whether the customer or supplier is linked to a director, shareholder, parent company, subsidiary, or senior manager.

- While reviewing ledgers: pay attention to loans, unusual journals, rent charges, consultancy fees, and balances that do not look like normal trading items.

- While helping with year-end files: collect evidence for disclosure notes, such as who the counterparty is, what the transaction was for, and whether anything remains unpaid at year end.

A simple test helps. If you would mention the relationship when explaining the transaction to your manager, it probably deserves a related party check.

This matters for your first role because junior staff often see the transaction before anyone else does. The financial controller or external accountant may only review totals later. You are the person who can flag, “This supplier is connected to management,” before the year-end note becomes a last-minute scramble. In practice, that means cleaner audit files, fewer follow-up questions, and better judgement during close.

The skill also carries into other reporting areas. If you want to improve reporting with revenue recognition, the same habit applies. Look past the entry itself and understand the commercial story behind it.

For trainees building career-ready habits, this is the difference between processing and accounting. Employers notice people who can post accurately and spot issues that affect disclosure, governance, and final accounts quality. If you want a clearer picture of what employers expect from junior finance staff, this guide to starting a UK accounting career is a useful next step.

Decoding IAS 24 Core Concepts and Definitions

Most confusion around International Accounting Standards 24 comes from the words, not the debits and credits. Once the language is clear, the standard becomes far less intimidating.

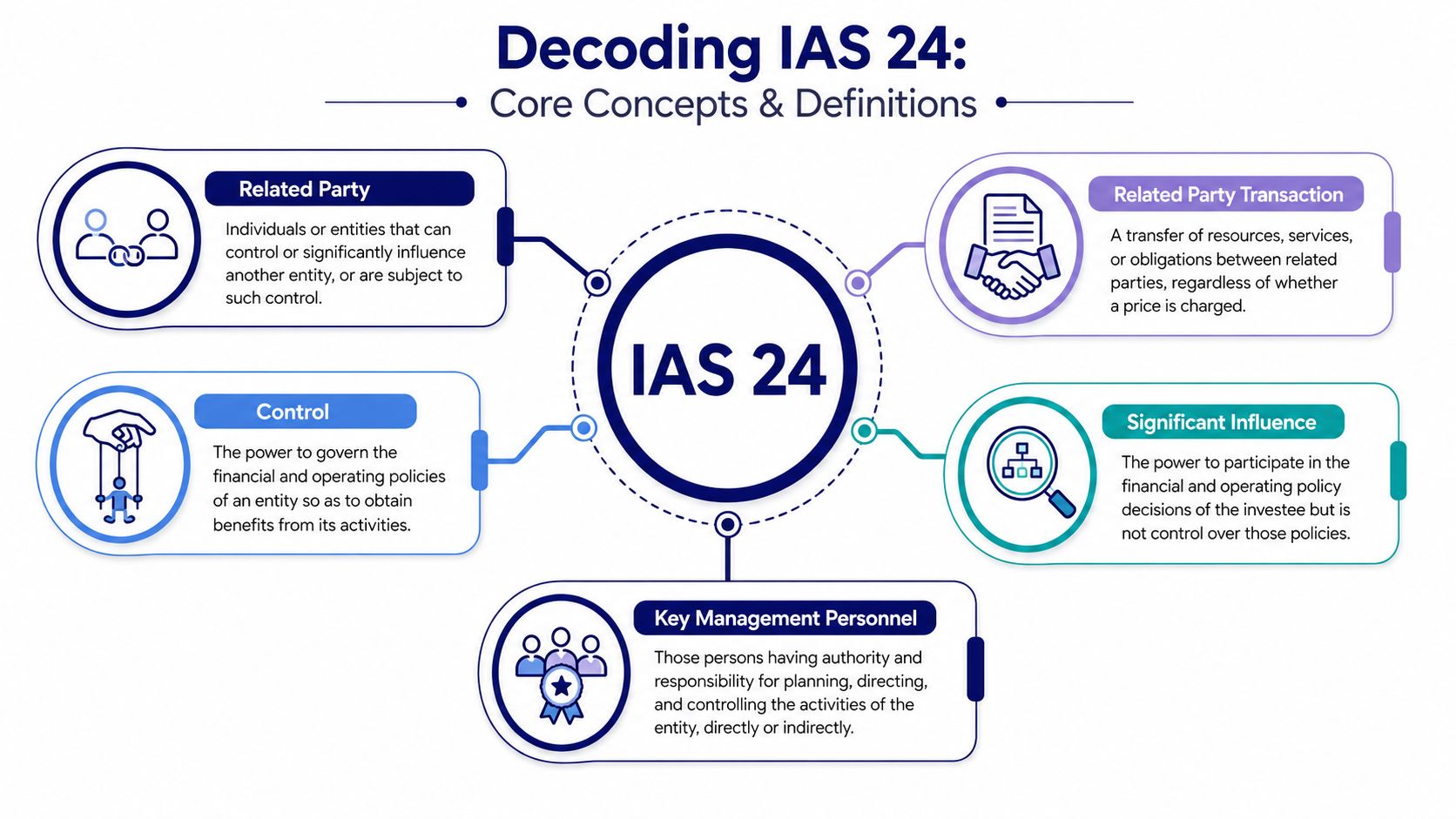

Related party

A related party is a person or entity connected closely enough to influence, or be influenced by, the reporting entity. In plain English, it means the relationship is close enough that transactions may not happen on the same basis as they would between independent strangers.

Consider a football match scenario. If two teams share the same owner, you wouldn't ignore that relationship when judging a player transfer between them. The transfer may still be valid, but users want transparency.

Under IAS 24, that can include group companies, controlling investors, key management personnel, and close family members where relevant. The important point for a trainee is simple. Don't only think about companies inside the group chart. Think about people and influence too.

Related party transaction

A related party transaction is wider than many new assistants expect. It isn't limited to a sale or purchase at market price. It can be a transfer of resources, services, or obligations between related parties, whether or not a price is charged.

That catches people out.

If a director lets the company use office space without charging rent, or a family-owned company provides services free of charge, there may still be disclosure implications even though the invoice value is nil. In the ledger, you may see very little. In the notes to the accounts, it may still matter.

Control and significant influence

These two ideas are often mixed up. A simple analogy helps.

- Control: You're the driver of the car. You decide where it goes.

- Significant influence: You're not driving, but you're the passenger whose views shape the route.

Control means having the power to govern financial and operating policies so benefits can be obtained from the entity's activities. Significant influence is weaker than control, but still meaningful. Someone may not command the whole business, yet still shape key decisions enough to create a related party relationship.

When a relationship can affect terms, timing, or decision-making, treat it as something to review rather than something to assume away.

Key management personnel

Key management personnel, often shortened to KMP, are the people with authority and responsibility for planning, directing, and controlling the entity's activities, directly or indirectly. In practice, that usually means directors and senior decision-makers.

IAS 24 requires disclosure of key management personnel compensation in total and by category, which gives the standard a strong governance angle in UK IFRS accounts.

Why these definitions matter in software and analysis

In Sage, Xero, or QuickBooks, the chart of accounts won't tell you whether a supplier is controlled by a director's family. The software records transactions. It doesn't automatically understand relationships unless your team builds that process.

That's why accounts assistants and analysts need to read beyond account codes. A “consultancy expense” line may be ordinary, or it may involve a related party. The code is the same. The context is different.

Identifying Related Parties in Practice

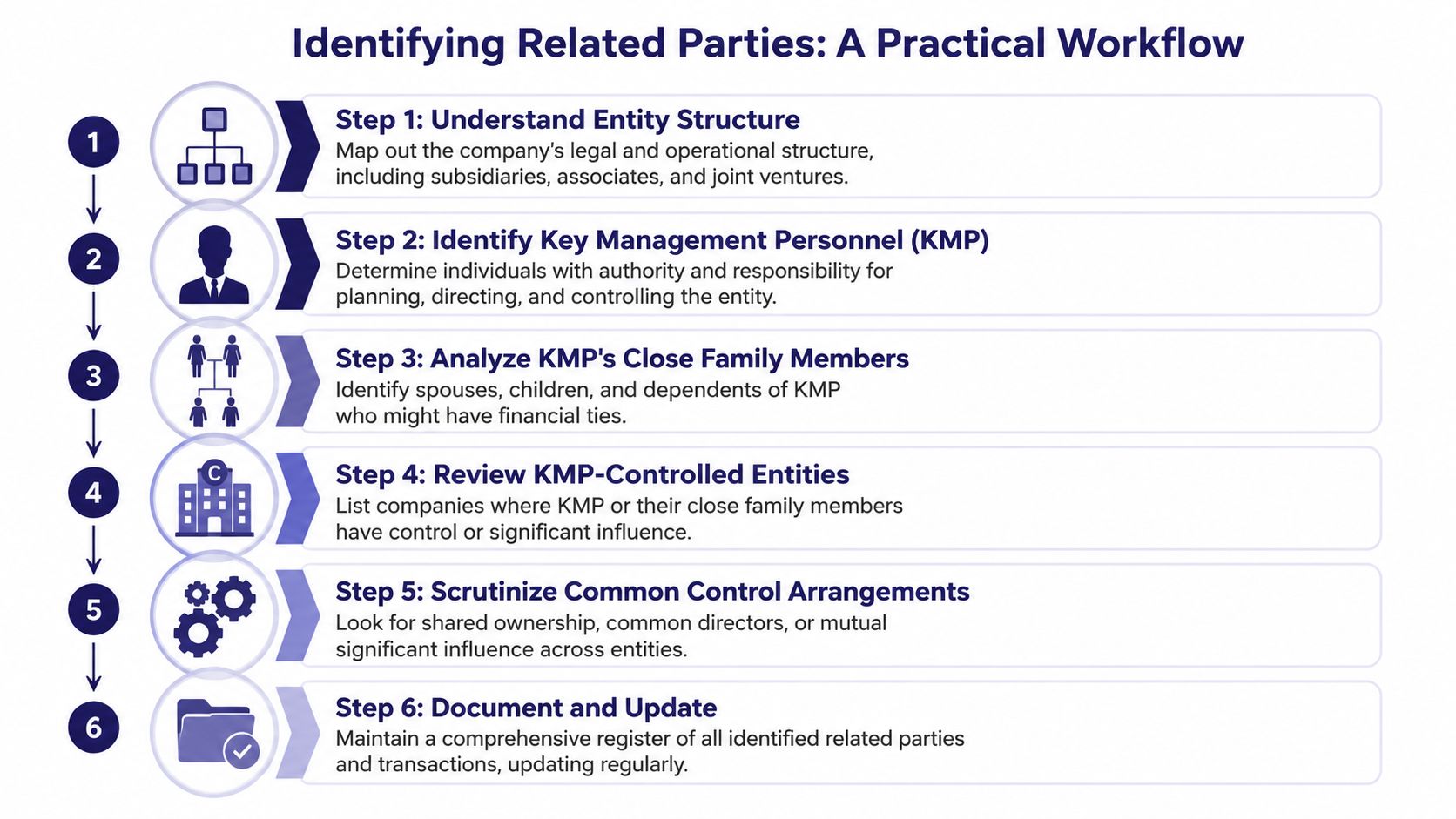

Knowing the definitions is one thing. Building a clean, auditable related party list is the primary task. Many trainees often get stuck in this process.

A useful starting point is this: related parties rarely reveal themselves neatly in the nominal ledger. You have to map them.

Start with people, then move to entities

Begin with a list of directors and senior decision-makers. Then ask practical questions.

- Who owns the company?

- Who controls major decisions?

- Which family relationships could be relevant?

- Which other businesses do those people control or influence?

- Are there trusts, holding companies, or sister entities outside the immediate group chart?

Determining related parties often requires significant judgement. KPMG notes that control can be direct or indirect, including common control, joint control, or significant influence, and that the practical challenge is building an auditable identification process rather than just reciting the rule in theory, as explained in its related party disclosures guidance.

Build a related party register

In a small business, this might start as a controlled spreadsheet. In a larger finance team, it may sit in a month-end checklist, governance file, or financial reporting workbook.

Include fields such as:

- Name of party: Individual or entity name.

- Relationship type: Director, shareholder, close family member, controlled entity, common control, or other.

- How identified: Board records, declarations of interest, ownership records, prior-year accounts, or management confirmation.

- Transactions noted: Sales, purchases, loans, balances, guarantees, or services.

- Review status: Confirmed, queried, or awaiting support.

Here's a useful explainer before the next step:

What to check in Sage, Xero, and year-end files

The software won't solve the judgement issue, but it can help you trace evidence.

- Supplier and customer lists: Scan for surnames, trading names, or entities you recognise from board discussions.

- Director's loan accounts: Review postings carefully. These often point to related party balances.

- Journals near period end: Look for recharges, write-offs, or manual entries involving unusual counterparties.

- Payroll and benefits records: Senior management data may help identify KMP-related items.

- Working papers: Prior-year disclosure notes often reveal names and relationships that still need tracking.

Working habit: Don't wait until the final accounts stage. Tag possible related parties during the year, while the detail is still easy to verify.

A good accounts assistant doesn't just process. They build a trail another person can follow. Auditors love that. Managers rely on it.

The Required Disclosures A Practical Checklist

IAS 24 matters because it focuses on disclosure, not recognition or measurement. The numbers may already be posted correctly, yet the accounts can still be incomplete if the note disclosure is weak. The IFRS overview explains that entities must disclose the nature of the relationship, transaction amounts, year-end balances, commitments, and terms, which helps users assess transfer-pricing risk and earnings quality because transactions may not be on market terms. It also means preparers need controls that capture both figures and narrative context in the IFRS IAS 24 standard summary.

What an accounts assistant should gather

When you support final accounts preparation, think in two layers. First, collect the numbers. Second, collect the explanation.

If you only hand over a ledger total, the financial reporting manager still won't know enough to draft the note properly. They need the relationship, the terms, whether a guarantee exists, and whether there are collectability concerns.

| Disclosure Item | What to Disclose | Practical Tip for Trainees |

|---|---|---|

| Nature of the relationship | Who the related party is and why they are related | Write this in plain English, such as “entity controlled by a director's close family member” |

| Transaction amounts | The value of transactions during the period | Pull totals from the ledger, then agree them to invoices, journals, or loan movements |

| Year-end balances | Amounts owed to or by the related party at period end | Reconcile to aged receivables, aged payables, or loan schedules |

| Commitments | Any obligations or arrangements that continue beyond year end | Check contracts, board minutes, and management emails |

| Terms and conditions | Whether balances are secured, unsecured, interest-free, repayable on demand, or otherwise unusual | Keep copies of agreements and note verbal terms confirmed by management |

| Guarantees | Any guarantee connected to the balance or transaction | Ask directly if a director or group entity has provided support |

| Doubtful debts and related expense | Any provision or expense recognised for balances with related parties | Cross-check impairment reviews and credit control notes |

| KMP compensation | Total compensation and the categories required for disclosure | Coordinate with payroll, HR, and year-end journals |

Why this often goes wrong

The hard part isn't always arithmetic. It's messy information. Terms may sit in emails. A family link may be known by management but not recorded in the purchase ledger. A director loan may have no formal agreement at all.

That's why data handling matters. If you're moving between finance support and analyst-style work, it helps to understand how unstructured and semi-structured information affects reporting quality. A practical read on that wider skill is this guide to semi-structured data for operations, because related party evidence often lives outside tidy accounting tables.

For extra context on the year-end note itself, many trainees also benefit from a focused explanation of related party transactions in financial reporting.

A simple year-end routine

Use this at month end or pre-audit stage:

- Run ledger extracts: Search supplier, customer, and journal activity for known related names.

- Review balance sheet accounts: Pay close attention to loans, accruals, and intercompany-style balances.

- Ask management specific questions: General questions get vague answers. Ask for names and relationships.

- Tie evidence together: Keep invoice copies, agreements, emails, and reconciliations in one folder.

- Draft a disclosure summary: Even a rough summary saves time for the final accounts reviewer.

Worked Example and Model Disclosure Text

A straightforward example makes IAS 24 much easier to apply.

A director pays business expenses personally when the company has a short cash flow squeeze. Later, instead of claiming each item separately, the amount is left in the director's loan account. There's no interest charged, and the balance remains unpaid at year end.

How to capture it in the bookkeeping records

In Sage or Xero, the postings might look routine. The original costs go to the correct expense codes. The credit goes to the director's loan account or another liability code used for amounts due to directors.

What matters is the extra tagging around the entry.

- Note that the counterparty is a director

- Keep support showing what was paid on behalf of the company

- Record whether the balance is interest-free

- Record whether it is repayable on demand or under another arrangement

- Flag the account for year-end related party review

If you only post the journal and move on, the disclosure trail weakens.

What the final accounts team needs from you

The reporting drafter usually needs four things:

- Who the related party is

- What happened during the period

- What balance remained at year end

- What terms applied

A short internal handover note might say:

Director-funded business expenses were recorded through the director's loan account. The balance was unsecured and interest-free. Management confirmed no formal repayment schedule.

That note gives the reviewer enough context to draft the financial statements.

Model disclosure text

You can adapt wording like this for a training exercise or working paper draft:

During the period, the company received funding support from a director through the director's loan account in respect of business expenditure paid personally on behalf of the company. The transactions were related party transactions by virtue of the director's role as key management personnel. At the reporting date, an outstanding balance was due to the director. The balance was unsecured and interest-free.

Notice what this wording does well. It states the relationship, explains the nature of the transaction, and describes the terms. It doesn't make unsupported claims such as “arm's length” unless the business can prove that statement properly.

What trainees often miss

The common mistake is to think, “It's already in the director's loan account, so that's enough.” It isn't. The ledger captures the accounting entry. IAS 24 asks for the story around the entry.

That's the difference between bookkeeping and financial reporting. One records the movement. The other explains its meaning.

Common Pitfalls and Advanced Scenarios

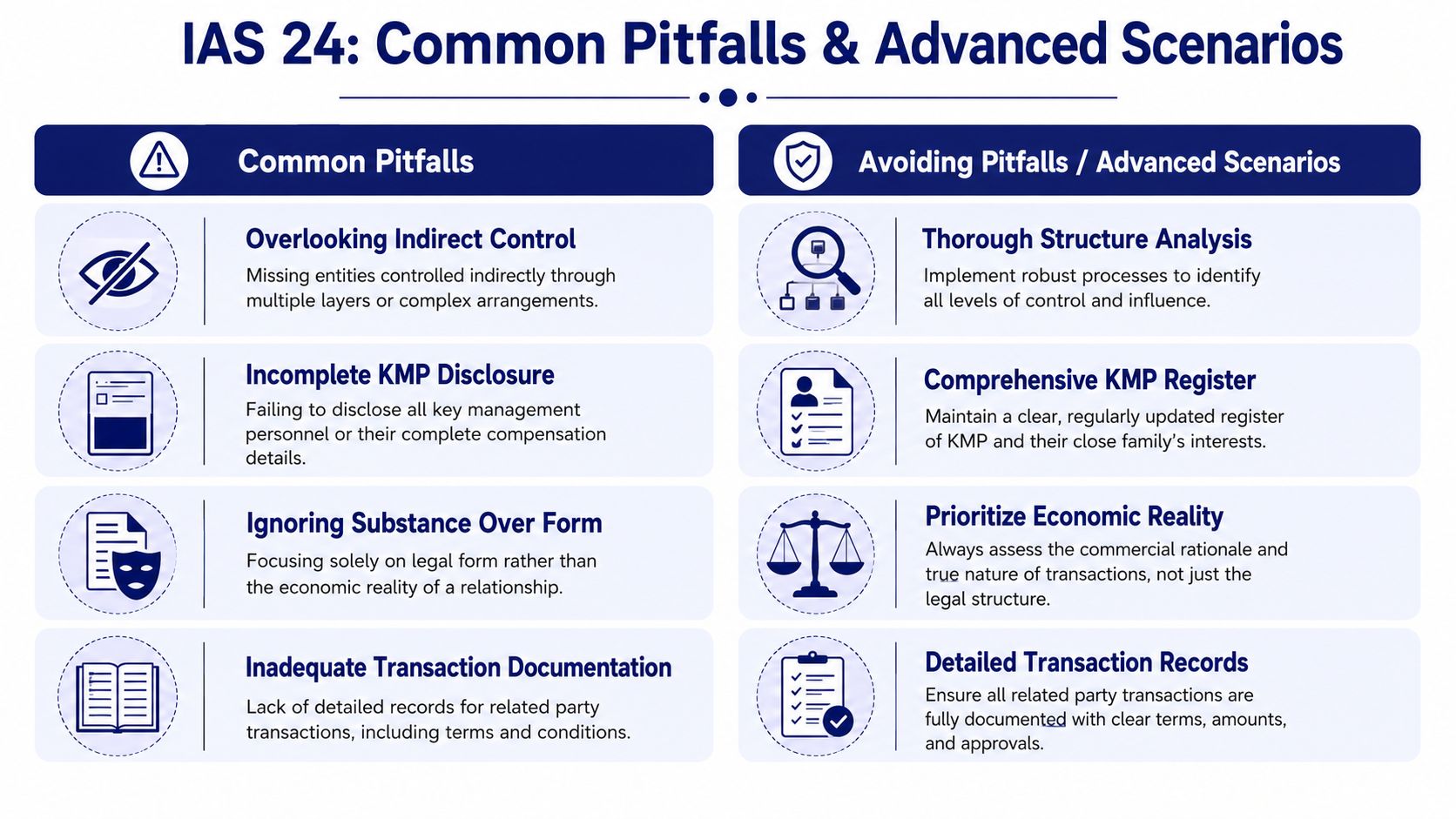

IAS 24 usually goes wrong in quiet ways. The company doesn't forget to prepare accounts. It forgets to ask the right questions.

Pitfalls that catch trainees early

One frequent error is missing transactions with no charge. If no invoice exists, trainees sometimes assume there's nothing to disclose. IAS 24 is wider than that.

Another problem is relying too heavily on legal names. A supplier may look unrelated on the system, but a quick enquiry reveals it is controlled indirectly by someone close to management.

Then there's the phrase “arm's length”. Some teams use it too casually. If the accounts say that, it should be supportable. Assumptions aren't evidence.

The safest habit is to test the relationship first, then draft the disclosure. Don't draft the narrative and hope the facts fit.

Government-related entities

There is also a targeted exemption for government-related entities. If the exemption is used, the entity must still disclose the government name, the nature of the relationship, and enough detail for users to understand the effect of the transactions, including individually significant items and a qualitative or quantitative indication of other material transactions, as set out in the IAS 24 guidance text.

For UK trainees in public-sector-adjacent organisations, housing, regulated environments, or government-linked structures, this is important. The exemption doesn't mean “say nothing”. It changes the reporting approach to one based on materiality and context.

IFRS and UK GAAP judgement

Many UK businesses don't use full IFRS, so trainees also need to recognise which framework applies before lifting wording from prior accounts. If the reporting framework differs, the disclosure route may differ too.

That wider point matters beyond IAS 24. If you're learning how accounting policy changes, estimates, and disclosures interact across standards, a useful follow-on topic is International Accounting Standard 8 and its role in reporting judgement.

A short avoidance checklist

- Question indirect links: Don't stop at the first company layer.

- Check family connections: Especially where small private companies are involved.

- Review unusual terms: Interest-free, unsecured, or undocumented balances need attention.

- Keep written evidence: Auditors can't inspect what nobody saved.

- Match framework to entity: IFRS wording doesn't belong everywhere automatically.

Turning IAS 24 Knowledge into Career Skills

You are helping close a year-end file in Xero. The ledger balances, the bank agrees, and the draft accounts look tidy. Then a manager asks one extra question: “Was that director loan repaid before year end, and do we need to disclose the rent paid to the director's property company?” That is the moment IAS 24 stops being theory and becomes job skill.

IAS 24 teaches you to read the story behind the entries, not just the entries themselves. For a UK trainee, that matters in day-to-day bookkeeping, year-end support, audit preparation, and analyst work. A payment can be coded correctly and still need disclosure because of who it was with. That is the practical habit employers want.

In real office work, the standard shows up as a process. You identify the related party. You trace the transaction in Sage or Xero. You check the paperwork, such as loan agreements, payroll records, board minutes, or invoices from connected businesses. Then you help turn that evidence into a disclosure note that is clear enough for a reviewer, auditor, or finance manager to follow.

That skill set reaches beyond compliance. It shows judgement.

It also makes software work more meaningful. In Sage or Xero, anyone can post a journal once they know which buttons to press. A stronger trainee asks better questions: Is this supplier connected to a director? Is this balance really a trade creditor, or is it a loan from a shareholder? Does payroll include key management pay that needs grouping for disclosure? Those questions reduce clean-up work at final accounts stage.

For UK companies applying IFRS, IAS 24 includes disclosure of related party relationships, transactions, outstanding balances, and key management personnel compensation by category, as noted earlier in the article. In practice, that means you are helping convert raw ledger data into information that explains the business relationships behind it.

If you can do that, you are already more useful to an employer than someone who only enters invoices and waits for instructions. You are helping the finance team spot risk, prepare cleaner working papers, and draft accounts with fewer last-minute surprises.

That is a strong career signal, and it is why practical training matters. If you want to turn IAS 24 knowledge into job-ready ability, Professional Careers Training offers practical accountancy training with ACCA-qualified support, flexible study options, software training in Sage, Xero and QuickBooks, and career support that helps trainees move from theory into real UK accounting and analyst roles.