You're in the middle of a live deadline stack, one client is asking for a VAT update, another wants year-end numbers, and your inbox keeps...

Why IAS 7 Matters for Your Accounting Career

A trainee often learns profit first and cash later. In the workplace, that order can cause trouble. You might post sales correctly, reconcile ledgers neatly, and still miss the fact that the business is short of usable cash.

IAS 7 gives structure to that problem. The modern version of the standard dates from December 1992, when the International Accounting Standards Committee issued the revised IAS 7, Cash Flow Statements, replacing the earlier standard. It took effect on 1 January 1994, and under current IFRS guidance it still requires IFRS reporters to present a statement of cash flows split into operating, investing, and financing activities, plus a reconciliation of cash and cash equivalents to the statement of financial position, as explained in this IAS 7 background paper.

For UK learners, that isn’t just history. UK-listed groups using IFRS follow this framework in their published accounts, so IAS 7 sits at the centre of how many UK businesses present liquidity.

Why employers care

If you want an Accounts Assistant role, your manager needs you to code transactions carefully enough that the finance team can prepare reliable cash flow information later.

If you want to work in bookkeeping and VAT, your day-to-day entries affect the quality of the underlying cash data. If the postings are messy, the cash flow statement becomes a repair job.

If you’re heading towards business analyst or data analyst work, cash flow helps you test whether reported performance looks sustainable. A company may show growth in revenue while cash from normal trading tells a more cautious story.

Practical rule: Profit shows performance under accounting rules. Cash flow shows movement of money. Good finance staff understand both.

Why this helps in training and interviews

IAS 7 knowledge makes you sound commercially aware. In interviews, you can explain why a lender, investor, or finance manager would look beyond profit. In exams, you can classify transactions more accurately. In software-based work, you can spot when poor chart design will create reporting problems later.

That’s also why systems matter. If you’re comparing tools for a growing business, this guide to choosing scalable software is useful because cash reporting quality often depends on how well the system captures transactions from the start.

When you’re building your wider accounting skills, it also helps to see IAS 7 as part of the final accounts process rather than a standalone topic. This guide to preparing financial statements puts the cash flow statement into that bigger reporting picture.

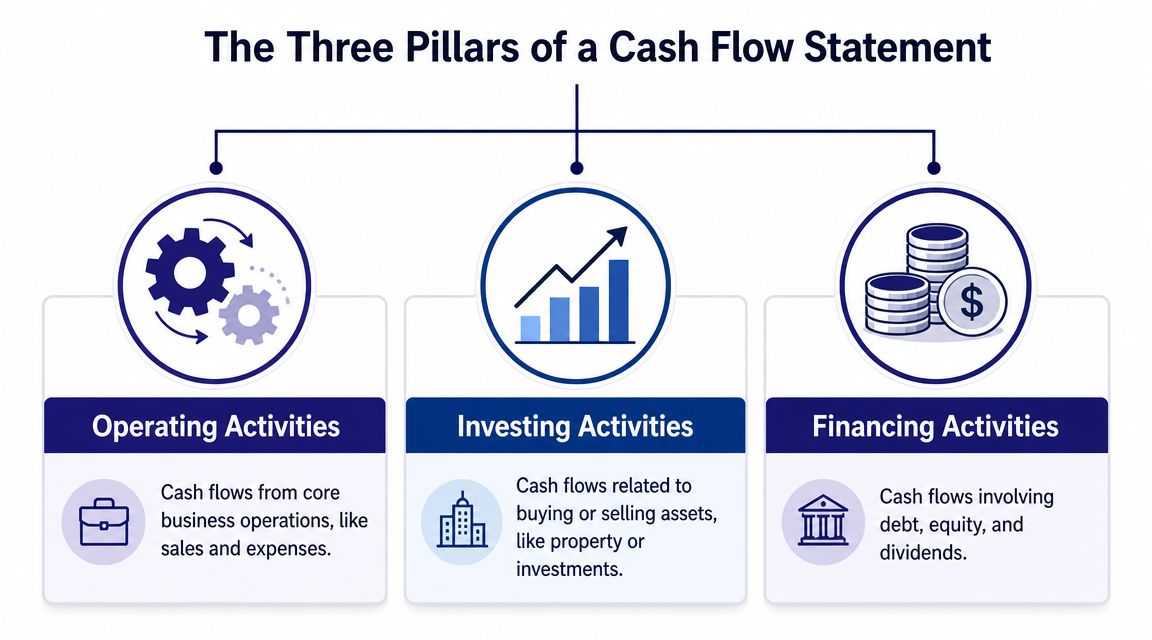

The Three Pillars of a Cash Flow Statement

Think about your own money for a moment. One part comes from your normal income. Another part relates to buying or selling things that last for years. A third part comes from borrowing, repaying debt, or putting money in from savings. IAS 7 uses a very similar idea for companies.

Operating activities

Operating activities are the cash flows linked to the main trading activity of the business.

For a shop, that usually means cash received from customers and cash paid to suppliers, staff, and other routine costs. For a service business, it may centre on fees collected and running expenses paid.

This category matters because people often treat it as the clearest sign of whether the core business is generating cash through normal work.

A simple trainee example helps:

- Cafe example: Cash from food sales is operating.

- Payroll example: Wages paid to staff are operating.

- Bookkeeping example: Payments to regular suppliers are operating.

Investing activities

Investing activities usually deal with longer-term assets and investments.

If a business buys equipment, sells a vehicle, or pays for software that will support the business over time, that normally points you towards the investing section. These aren’t day-to-day trading flows. They relate to building or changing the asset base.

Examples you might see in a UK accounts office include:

| Activity | Likely classification | Why |

|---|---|---|

| Buying machinery | Investing | It supports the business over time |

| Selling old equipment | Investing | It relates to a non-current asset |

| Paying for a long-term asset | Investing | It isn’t part of routine trading receipts and payments |

Financing activities

Financing activities show how the business funds itself and returns funds to providers of finance.

This includes items such as raising a loan, repaying borrowings, or issuing shares. If operating tells you how the business trades, financing tells you how it stays funded.

That distinction is useful in interviews. If a business has weak operating cash but keeps receiving loan cash, you can see that the company is being supported by finance rather than by normal trading.

A strong answer in an interview isn’t just naming the category. It’s explaining what the category says about the business model.

Where learners get confused

The hard part isn’t the three labels. The hard part is that some items don’t fit neatly when you first see them.

IAS 7 requires UK IFRS reporters to classify cash flows into operating, investing, and financing activities, but it also allows interest and dividends received or paid to be classified across those categories if the policy is applied consistently and disclosed. In practice, accountants have to map each cash movement to its underlying economic nature, not just the account name in the ledger. A supplier-finance or lease-linked payment, for example, can include both financing and operating elements and cannot be classified solely by its predominant characteristic, as explained in BDO’s IAS 7 in practice guide.

That point matters more than many trainees realise. If you classify something badly, you can make operating cash flow look better or worse than it really is. Employers notice when you understand that risk.

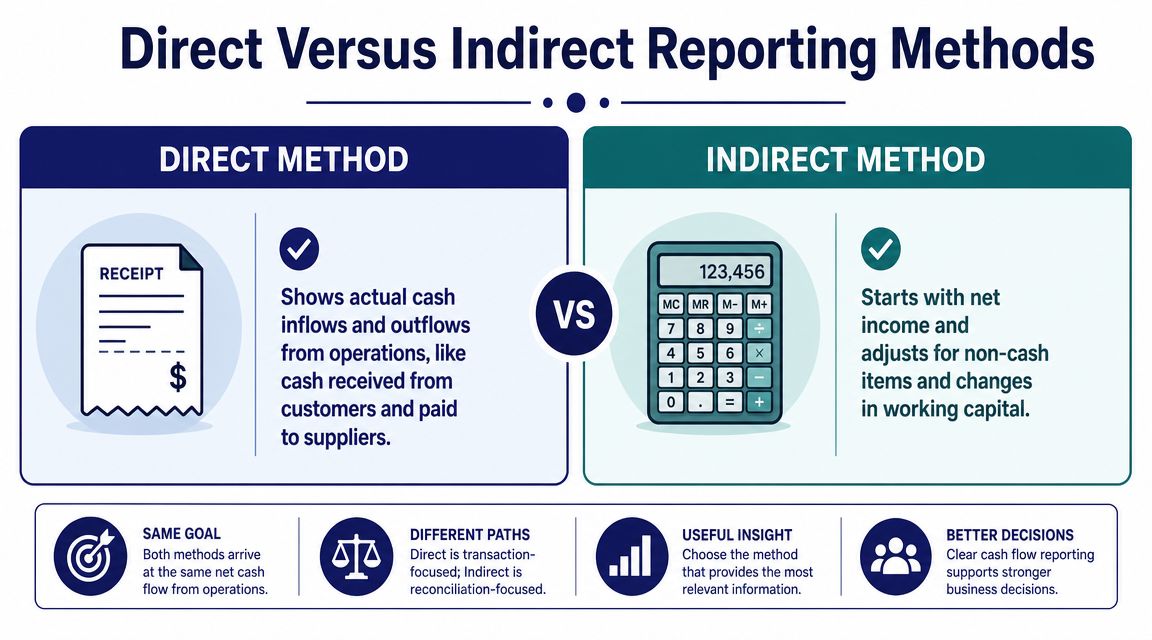

Direct Versus Indirect Reporting Methods

Many learners are fine with the three categories, then get stuck on direct and indirect reporting. The confusion usually starts because both methods deal with operating cash flows, but they tell the story in different ways.

The direct method

The direct method lists major classes of cash receipts and cash payments from operations.

It reads in a straightforward way. Cash received from customers. Cash paid to suppliers. Cash paid to employees. Cash paid for other operating costs.

That’s why many learners find it easier to understand at first glance. It looks like a real cash summary rather than an accounting bridge.

The indirect method

The indirect method starts with profit and adjusts it to arrive at operating cash flow.

You take profit, then remove non-cash items and reflect working capital movements. Trainees encounter adjustments for depreciation, receivables, payables, and inventory.

For an analyst, this method is useful because it reveals the gap between reported profit and cash generated from operations. It shows whether earnings are being tied up in stock or unpaid customer balances.

Side-by-side comparison

| Feature | Direct method | Indirect method |

|---|---|---|

| Starting point | Actual cash receipts and payments | Profit figure |

| Main strength | Clear picture of cash movement | Clear link between profit and cash |

| Typical trainee challenge | Gathering detailed cash data | Understanding adjustments |

| Best for | Seeing operational cash movement plainly | Analysing earnings quality |

What IAS 7 allows

Under the UK’s IFRS-aligned framework, IAS 7 includes detailed disclosure rules and allows separate disclosure of interest and dividends cash flows, with classification choices applied consistently. The IFRS Foundation states that cash equivalents are short-term, highly liquid investments convertible to known amounts of cash with an insignificant risk of value change, and ICAEW confirms that operating cash flows may be shown using either the direct or indirect method, as noted on the IFRS Foundation IAS 7 page.

That gives companies a choice. In practice, many trainees meet the indirect method more often in study materials and workplace reports because it connects directly back to profit.

If you’re aiming for business analyst or data analyst work, don’t just memorise the indirect method. Learn what each adjustment is telling you about stock, debtors, creditors, and non-cash charges.

Why this matters for job roles

For accounts assistants, the indirect method teaches you why clean ledger postings matter. If depreciation is mixed up, if working capital accounts aren’t reconciled, the cash flow statement becomes unreliable.

For final accounts work, the indirect method is often where the draft report is tested for logic. If profit rose but receivables and stock also rose sharply, cash may not have kept pace.

For data-focused roles, this method helps you ask sharper questions. Is growth being funded by customer cash, or by delayed supplier payments? Are profits supported by real collections, or trapped in balances?

Classifying Tricky Items Like Interest and Tax

At this point, many trainees stop feeling comfortable. The obvious transactions are easy. The awkward ones are the ones that turn up in real jobs, real software, and real interviews.

Interest and dividends

Interest paid can look like an operating item because it is paid in the course of running the business. It can also look like a financing item because it relates to borrowings.

Interest received and dividends received can create the same kind of debate. The key with IAS 7 is not choosing at random. The entity needs a consistent policy and must disclose it properly.

For a trainee, the practical lesson is simple. Don’t classify these items just because the nominal code says “finance cost” or “investment income”. Think about the policy being followed and whether it is being used consistently.

Tax cash flows

Tax often causes confusion because learners want a shortcut. They want a rule that says all tax goes in one bucket without question.

Real life is messier. You need to look at the nature of the cash flow and the reporting approach used. The difficulty is one reason this area keeps appearing in technical discussions and classroom examples.

Hybrid transactions and split elements

A lease-linked payment is a good example of where trainees can get caught out. One payment may include an element that feels operational and another that reflects financing. A single label in the ledger doesn’t solve that problem.

The same issue appears in supplier-finance arrangements and one-off deals with several moving parts. If you classify the whole amount by instinct, you may misstate operating cash flow.

When a transaction has mixed features, slow down. Ask what each cash component actually represents.

A few mini-scenarios

- Manufacturing company interest paid: You should check the policy. Don’t assume.

- Dividend received by an investment-focused entity: The economic nature may point you one way, but the reporting policy still matters.

- Corporation tax paid after a profitable year: Don’t rely on habit alone. Consider the nature of the payment and any related transaction context.

- Lease payment: You may need to split the cash flow rather than dump it all into one category.

Why this remains a live issue

A frequently underexplained UK issue is how IAS 7 classification works for hybrid or one-off transactions such as taxes, lease payments, and multi-element deals. IAS 7 requires cash flows to be classified by the nature of the activity, not by a transaction’s predominant characteristic, and EFRAG’s work has highlighted ongoing preparation problems around taxes, investing, and financing cash flows. In the UK context, this is especially relevant because IFRS 18 will amend IAS 7 and is effective for periods beginning on or after 1 January 2027, as discussed in KPMG’s overview of IFRS developments.

That’s useful in an interview because it shows you know two things. First, IAS 7 still involves judgement. Second, those judgements need to be documented well because reporting rules continue to evolve.

A Worked Example of a Cash Flow Statement

Let’s use a simple fictional example for Fictional UK SME Ltd. using the indirect method. The numbers below are only a training illustration to show structure and logic.

Sample statement

| Description | £’000 (Year 2026) |

|---|---|

| Profit before tax | |

| Adjust for depreciation | |

| Adjust for changes in receivables | |

| Adjust for changes in inventory | |

| Adjust for changes in payables | |

| Cash generated from operations | |

| Tax paid | |

| Net cash from operating activities | |

| Purchase of equipment | |

| Net cash used in investing activities | |

| Loan received | |

| Loan repayment | |

| Dividends paid | |

| Net cash from financing activities | |

| Net increase or decrease in cash and cash equivalents |

How to read it

Start with profit before tax. This is an accounting figure, not a cash figure.

You then adjust for non-cash items such as depreciation. Depreciation reduces profit, but it doesn’t mean cash left the bank during the period. So you add it back when reconciling profit to operating cash flow.

Then come the working capital movements. These are often the most important lines for trainees.

- Receivables increase: Sales may have been recorded, but customers haven’t paid yet. That usually reduces operating cash.

- Inventory increase: The business has tied cash up in stock. That also tends to reduce operating cash.

- Payables increase: The business has delayed payment to suppliers. That can increase operating cash in the short term.

A common interview question is, “Why can profit rise while operating cash falls?” Working capital movements are often the answer.

What each section tells you

Operating activities show whether the core business is generating cash after adjusting profit for non-cash items and working capital changes.

Investing activities show whether the business is spending cash on assets or receiving cash from disposals.

Financing activities show whether the business is relying on loans, owner funding, or distributions.

That mix matters. A business can survive weak operating cash for a while if financing inflows are strong, but that isn’t the same as healthy day-to-day trading.

Trainee takeaway

If you’re preparing for software-led accounting tasks in Xero, Sage, or QuickBooks, this structure helps you understand what sits behind the report you print. If you’re preparing for final accounts work, it helps you explain why changes in the balance sheet affect cash.

For extra practice with layout and method, this guide to preparing a cash flow statement is a useful reference point when you want to turn ledger data into a finished statement.

Essential Disclosures and Foreign Currency Flows

A cash flow statement doesn’t stand on its own. The notes around it matter because they explain what sits inside the figures and what readers should be careful about.

What users need to understand

A good set of disclosures helps readers answer practical questions:

- What counts as cash equivalents

- Whether any major investing or financing activity happened without cash

- Whether the business has restrictions on using some cash balances

- Whether financing structures are affecting the picture shown by operating cash flow

Foreign currency adds another layer. If a business receives or pays cash in another currency, the accounting team has to translate that cash flow properly. Exchange differences can also affect the movement between opening and closing cash balances.

If you’re new to this area, it helps to pair IAS 7 with exchange-rate rules. This IAS 21 training resource on foreign currency matters gives useful context for understanding how foreign currency cash movements feed into financial reporting.

Supplier finance disclosures

A technically important recent change is the IAS 7 supplier finance amendment issued by the IASB in May 2023, effective for annual periods beginning on or after 1 January 2024, with early application permitted. The amendment requires entities to disclose the effect of supplier finance arrangements on liabilities, cash flows, and liquidity risk. It also means finance and treasury teams need to track opening and closing carrying amounts of supplier-finance liabilities and explain non-cash changes, as outlined in EY’s summary of the supplier finance amendments.

A key implication is that supplier finance can make operating cash flow look stronger than the underlying working-capital pressure really is.

Why this helps your employability

Employers value trainees who read beyond the face of the statement. If you can say, “I’d also want to inspect the note on supplier finance and the makeup of cash equivalents,” you sound like someone who understands reporting quality, not just report formatting.

For business analysts, those disclosures help you judge liquidity risk. For accounts assistants, they show why detailed schedules and reconciliations matter. For bookkeepers, they reinforce the need for accurate coding and document retention from the start.

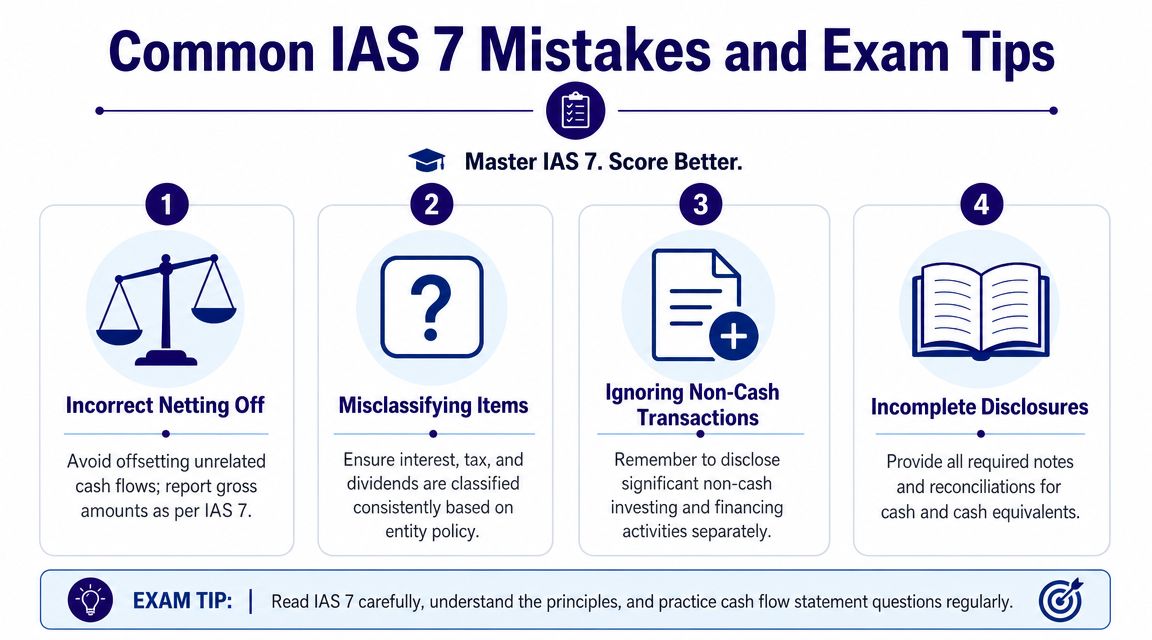

Common IAS 7 Mistakes and Exam Tips

The most common IAS 7 errors usually come from rushing. A trainee sees a familiar label, picks a category quickly, and moves on. That works for easy questions, but it breaks down in exams and in real accounts work.

Mistakes that keep appearing

- Incorrect netting off: Don’t offset unrelated inflows and outflows when gross presentation is needed.

- Misclassifying awkward items: Interest, dividends, tax, lease-related cash flows, and supplier-finance items need careful judgement.

- Ignoring non-cash transactions: If a major investing or financing event happens without cash, it still matters for disclosure.

- Forgetting consistency: A policy choice is only useful if the business applies it consistently and explains it clearly.

Exam and interview tips

- Start with the business story: Ask what the company does. Classification gets easier when you understand the business model.

- Trace the movement: Don’t just look at the income statement. Use balance sheet changes to explain cash effects.

- Watch operating cash closely: Interviewers often care most about whether the core business is producing cash.

- Explain judgement out loud: If an item is tricky, say why it is tricky and what policy issue you would check.

- Use software logic: In workplace tests, think about how Sage, Xero, or QuickBooks codes feed through to reporting.

- Link cash to employability: An accounts assistant who understands cash conversion is more useful than one who only memorises ledger names.

A short video can also help reinforce the mechanics visually.

Learn IAS 7 as a decision process, not a memorised list. That’s what helps you in exams, month-end work, and interviews.

If you want structured support with cash flow statements, bookkeeping, final accounts, payroll systems, accounting software, or job-focused finance training, Professional Careers Training offers accountancy and employability courses with practical delivery, software exposure, and recruitment support designed for trainees entering UK finance roles.