You might be doing everything “right” and still feel stuck. You've taken on more at work, helped with month-end, learned bits of Excel or Xero...

An invoice lands in your inbox for “consultancy services”. The supplier name is unfamiliar, but the director's surname appears in the company title. The payment terms are odd. Nobody seems surprised except you.

That moment matters more than most trainees realise.

If you're working in bookkeeping, payroll, accounts prep, final accounts, or even moving into business analysis and data analysis, the work evolves from routine processing into real financial judgement. You're no longer just posting invoices. You're spotting relationships, asking whether a transaction is ordinary, and deciding what needs extra care before the accounts go out.

Related party transactions sound technical, but the daily work is practical. Who is connected to the business? What changed hands? Was it recorded properly? Does it need to be disclosed? Those are the questions that sharpen your skills and make you more useful to any finance team.

Your Guide to Navigating Related Party Transactions

A junior accounts assistant often sees the first signs of a related party transaction long before a manager does. It might be a rent invoice from a landlord who turns out to be the director. It might be wages paid to a relative with no clear contract on file. It might be a balance on the ledger that sits there month after month because nobody wants to chase it.

None of those things automatically means something is wrong. Many related party transactions are perfectly normal. Groups trade with subsidiaries. Directors lend money to support cash flow. Companies pay key managers for genuine work. The issue is not that a relationship exists. The issue is that the relationship can influence the deal.

Why trainees get stuck

Most confusion starts with one wrong assumption. People think a transaction only matters if cash changed hands at a strange price.

That's too narrow.

A relationship can affect timing, credit terms, guarantees, write-offs, or whether the transaction happened at all. Once you start thinking that way, you stop looking only at invoices and start looking at the full story around the entry.

Practical rule: If a connection could affect the terms, treat it as something to review, not something to ignore.

This is why the topic matters across several career paths:

- Bookkeeping and VAT staff: You're often posting supplier invoices, director expenses, and intercompany entries first.

- Accounts assistants: You're likely to reconcile loan accounts, review aged balances, and support the year-end file.

- Final accounts trainees: You need to help draft notes that explain what happened and who was involved.

- Advanced payroll learners: You may see payments to directors or key management that need separate consideration.

- Business analysts and data analysts: You may be asked to spot unusual patterns, connected entities, or repeated payments with weak commercial logic.

The skill behind the rule

Good finance staff don't panic when they see something connected to a director or senior manager. They slow down, gather facts, and document clearly.

That mindset is what moves you forward in your career. A trainee who can say, “This supplier may be connected to the director, I've checked Companies House, matched the invoices, and flagged the year-end balance for disclosure review,” is already thinking beyond data entry.

Related party transactions are one of those subjects that reveal how accounting really works. The ledger entry is only part of the job. The rest is judgement, evidence, and clear reporting.

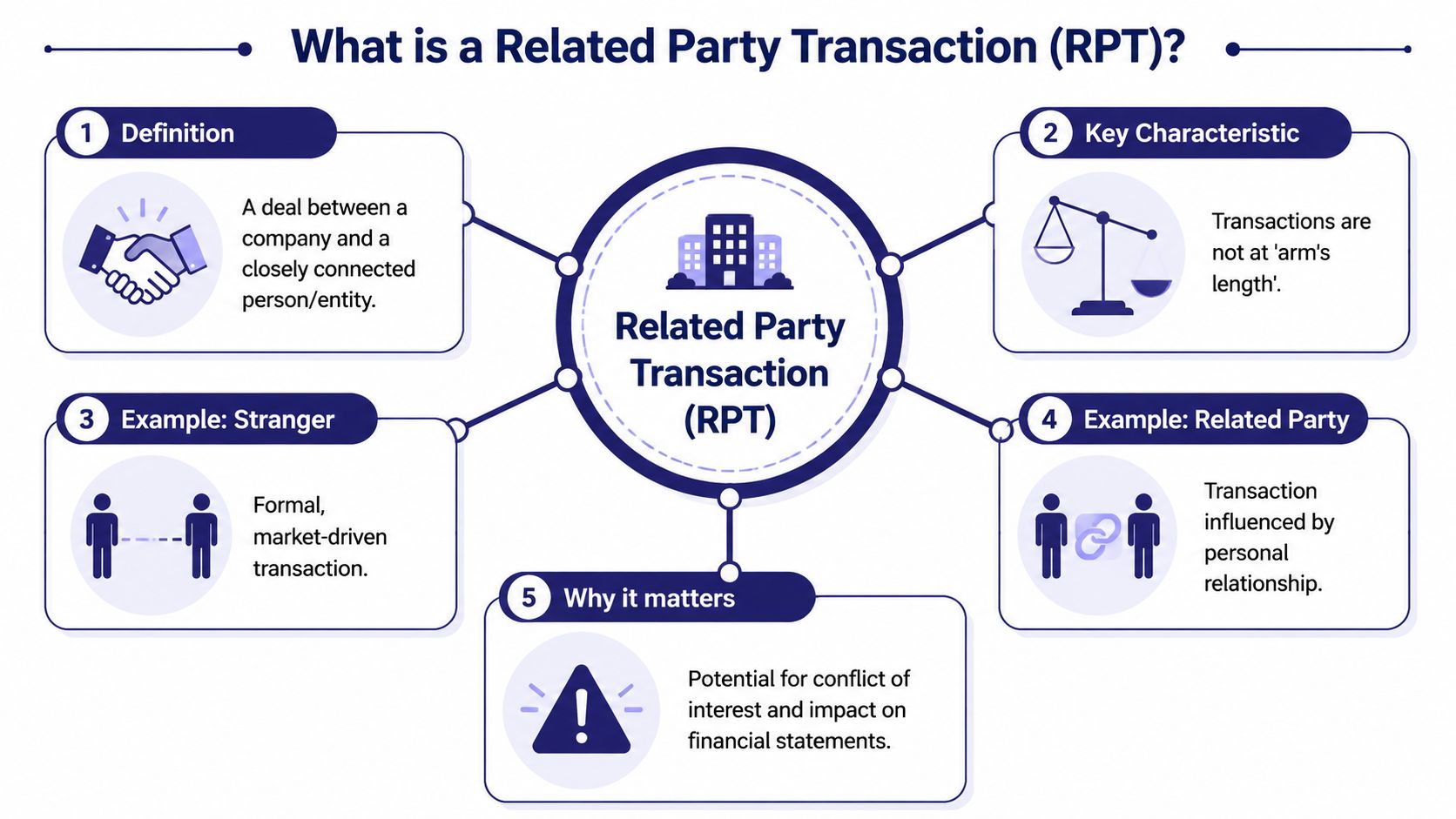

What Exactly Is a Related Party Transaction

At heart, a related party transaction is a deal between a business and someone closely connected to it. The easiest way to understand it is to compare two loans.

A bank lends money to a company after credit checks, legal documents, and commercial pricing. A director lends money to the same company because the business needs support and the director wants to help keep it trading. Same broad category, very different relationship.

That relationship is the reason the accounting rules care.

The simple idea behind it

Business deals with strangers are usually described as arm's length. Each side looks after its own interest. Each side negotiates.

Deals with related parties may still be genuine and fair, but the relationship can influence the outcome. A company may accept delayed payment. A director may waive interest. A parent company may guarantee a loan. A family member may provide services without charging immediately.

Under IAS 24, which governs this area in practice for most UK reporting entities, a related party transaction is defined broadly as any transfer of resources, services, or obligations between a reporting entity and a related party, regardless of whether a price is charged. The standard also requires disclosure of the nature of the relationship and details about transactions, outstanding balances, and commitments, and it requires separate disclosure of key management personnel compensation by category, as explained in the IAS 24 related party disclosures standard.

That last point catches many trainees out. No invoice is needed for something to matter.

Common examples in plain English

A related party transaction could include:

- A director's loan: The director pays company bills personally, then the company records the balance owed back.

- Use of property: The company trades from a building owned by a shareholder or director.

- Management charges: One group company charges another for support staff or admin time.

- Loan guarantees: A connected person supports company borrowing without charging a fee.

- Unpaid balances: Money remains outstanding between the company and a connected party at year end.

If you handle director current accounts, it also helps to understand the wider practical issues around UK director loan regulations, because those balances often overlap with related party questions in real bookkeeping work.

A useful test is this. Would the terms probably look the same if the business were dealing with a complete stranger?

If the answer is no, or even “not sure”, you've likely found something worth checking.

The UK Rules You Need to Know

The rules can look scattered because they sit in accounting standards, company law, and audit practice. But the reason behind them is simple. Users of accounts need to see where personal connections may have influenced the numbers.

For UK trainees, the three names you'll hear most often are IAS 24, FRS 102 Section 33, and the Companies Act 2006. They don't all do exactly the same job, but they all push in the same direction. They aim for transparency.

Why the framework exists

The modern disclosure approach used by UK companies is rooted in IAS 24. It was designed to address a long-standing reporting risk. Related parties can influence reported results even when transactions look formal and may appear to be at arm's length. Audit practice reinforces this by requiring auditors to evaluate whether related party transactions were properly identified, accounted for, and disclosed, and to watch for transactions that may lack a business purpose, as discussed in Deloitte's guide to related party transactions and disclosure frameworks.

That's the key point. The rules aren't there because every connected transaction is suspicious. They're there because readers of the accounts need enough information to judge the effect of those relationships.

How a trainee should think about the rulebook

A simple working view helps:

| Framework | What it means in practice |

|---|---|

| IAS 24 | Tells you what related party information needs to be disclosed in the accounts. |

| FRS 102 Section 33 | Serves a similar purpose for many UK GAAP preparers. |

| Companies Act 2006 | Adds legal duties in areas such as directors, approvals, and reporting obligations. |

You don't need to memorise every paragraph to work well in practice. You do need to understand what each framework is trying to prevent.

- Hidden influence: A business can look more profitable or more stable if connected deals aren't visible.

- Weak comparability: If one company uses connected-party support and another doesn't, users need to know.

- Poor governance: Directors and boards must show that connected dealings were handled properly.

What this means at desk level

For an accounts assistant, the practical effect is straightforward. You need to keep records that help someone else follow the trail.

That means names, relationships, approval evidence, balances outstanding, and supporting documents. If you leave those details vague in Xero, Sage, or QuickBooks, the year-end team has to rebuild the story from scratch. That wastes time and increases risk.

How to Spot Related Party Transactions in Your Work

Most related party transactions don't announce themselves clearly. They show up as ordinary entries with slightly odd features. A different surname on the bank statement. A supplier set up in a rush. A journal that moves a balance without much explanation.

That's why good trainees build a habit of looking for patterns.

Mini-scenarios you'll recognise

A purchase invoice arrives from a company that shares an address with one of your directors. The service description is broad. Nobody can point you to a contract.

A rent payment goes out monthly, but the property isn't owned by the company. It belongs to a shareholder.

A sales invoice is raised to another company in the group, but the amount remains unpaid far longer than ordinary trade debt.

A director's current account moves up and down all year with expenses, personal payments, and occasional business costs all mixed together.

None of those entries proves misconduct. But each one deserves follow-up.

What to check first

When something feels unusual, start with plain questions:

- Who is the counterparty: Is this person or business connected to a director, shareholder, senior manager, or group company?

- What is the business reason: Can someone explain why the company entered into the transaction?

- What are the terms: Are payment timing, credit, guarantees, or pricing different from normal trading terms?

- What evidence exists: Is there an invoice, agreement, email approval, board minute, or payroll support?

- What is still outstanding: Does a balance remain unpaid or unresolved at the reporting date?

If the paperwork is thin and the relationship is close, raise the question early. Don't wait for the audit file.

Academic evidence discussed in a UK-relevant fraud context shows that related party transactions are not automatically fraudulent, but when fraud exists they are more likely than non-related-party frauds to involve the CEO or CFO and misappropriation of assets. That's why they are better treated as a higher-risk signal than a standalone red flag, as outlined in the analysis of fraud and related party transactions.

Red flags in bookkeeping systems

In Xero, Sage, and QuickBooks, warning signs often appear as coding or master-data issues rather than dramatic events:

- Supplier records with personal names hidden inside business names

- Nominal postings to suspense or generic admin codes

- Repeated journals into director loan or intercompany accounts

- Round-sum invoices with weak descriptions

- Aged balances that nobody clears

- Payments made before approval paperwork appears

If you're also moving toward data analysis, then your skills become valuable. Filtering transactions by shared addresses, repeated bank references, or connected contacts can reveal patterns that manual reviews miss.

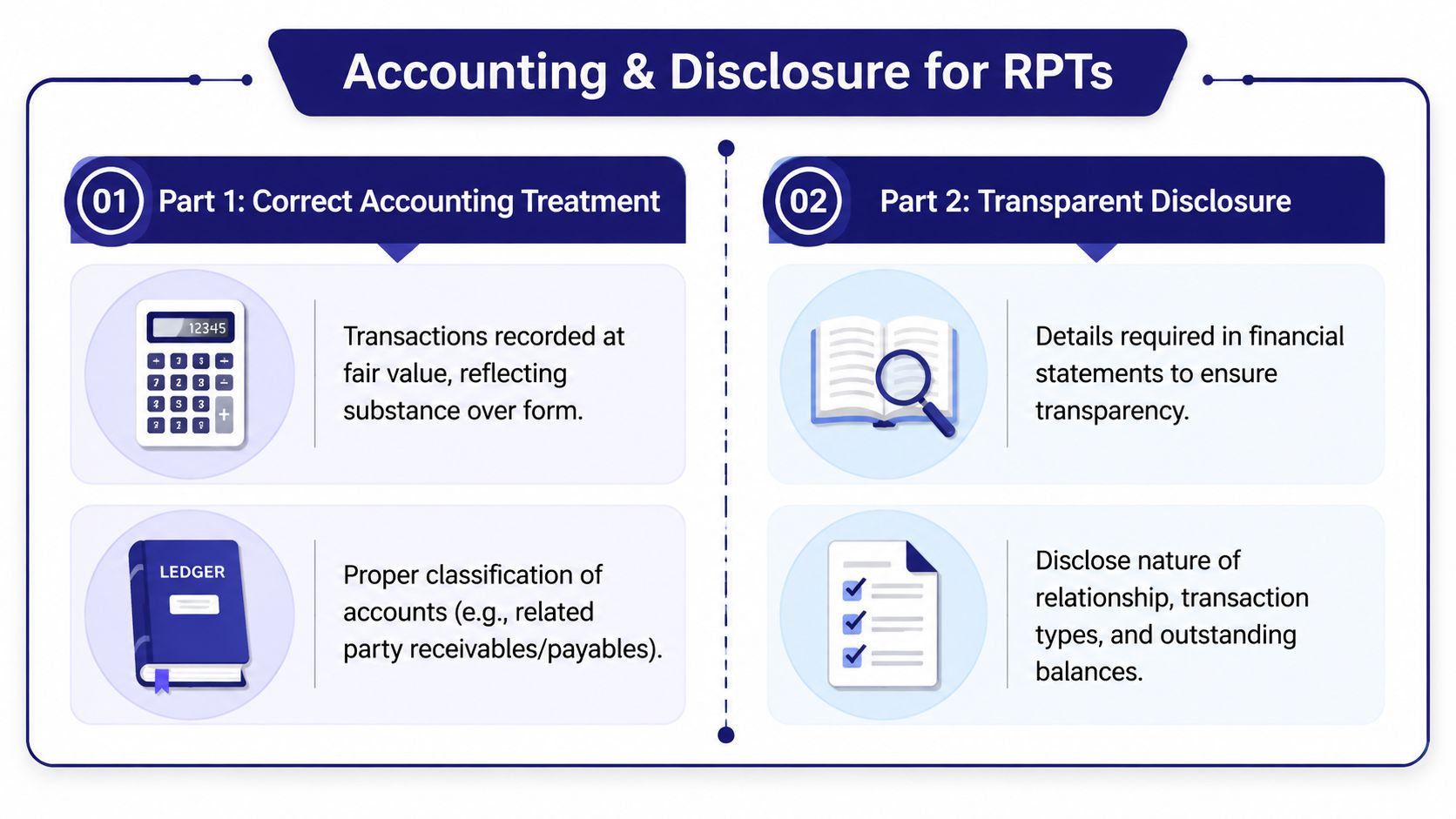

Correct Accounting and Disclosure for RPTs

Once you've identified a related party transaction, your job has two parts. First, record it correctly in the ledger. Second, make sure the year-end disclosure tells the truth clearly enough for someone outside the business to understand what happened.

That split matters. A transaction can be posted accurately in the bookkeeping and still be badly disclosed in the final accounts.

A simple accounting example

Take a common case. A director pays a company supplier personally because cash is tight, and the company now owes the director.

A basic bookkeeping entry might look like this:

| Entry | Debit | Credit |

|---|---|---|

| Supplier expense or creditor cleared | Relevant expense or creditor account | |

| Amount owed to director | Director's loan account |

If the company later repays the director:

| Entry | Debit | Credit |

|---|---|---|

| Reduce liability to director | Director's loan account | |

| Cash paid from bank | Bank |

That's simple bookkeeping, but the detail around it matters. Keep the invoice, note why the director paid it, and make sure the posting goes to a clearly labelled account rather than disappearing into a miscoded liability.

This is also why final accounts work needs strong support files. If you want a broader refresher on year-end preparation, this guide to how to prepare financial statements is useful background.

What the disclosure needs to say

In the UK, IAS 24 requires disclosure of the nature of the related-party relationship, the transaction amount, outstanding balances, commitments, and terms and conditions because related parties may influence pricing, timing, and settlement in ways that are not visible in arm's-length trading. Those disclosure points are also central to audit work under auditor procedures for related party transactions.

A plain-language disclosure note might say that during the year the company received administrative support from an entity controlled by a director, describe the amount charged in the year, state what balance remained outstanding at year end, and explain the main terms such as repayment or settlement arrangements.

Keep the wording factual. Don't dress it up. Don't leave out the uncomfortable parts.

Here's a short explainer that can help fix the idea in your mind:

One practical mistake to avoid

Trainees sometimes think that if the balance is small or the transaction was genuine, disclosure is optional. That's the wrong mindset.

Audit view: The question isn't only whether the posting is correct. It's whether the accounts give a clear picture of the relationship and its effect.

That's why you should document the relationship while processing the entry, not months later during year-end panic.

Auditing RPTs and Setting Up Internal Controls

Auditors pay close attention to related party transactions because they carry built-in risk. A connected transaction may be valid, but it can also be used to shift profits, hide liabilities, move assets, or bypass normal approval routes.

From an auditor's perspective, the danger is not just a wrong number. It's an incomplete story.

What auditors want to know

An auditor usually asks questions such as:

- Was the related party identified properly

- Who approved the transaction

- Does it have a clear business purpose

- Do the records support management's explanation

- Has the company disclosed it fully

That's why businesses need more than a year-end disclosure note. They need internal controls that make related party transactions visible when they happen.

Controls that actually help

A sensible control environment often includes the following:

- A related party register: Keep an up-to-date list of directors, key managers, close connections, and relevant entities.

- Approval rules: Require board or senior review before significant connected-party deals are entered into.

- Separate ledger treatment: Use dedicated nominal codes or tracking categories for director loans and intercompany balances.

- Evidence retention: Store contracts, invoices, emails, and approvals in one place.

- Year-end confirmation: Ask directors and senior staff to confirm related party relationships and transactions before the accounts are finalised.

The issue of materiality is also important. In some US disclosure settings, SEC Item 404 uses a threshold above $120,000, but UK practice focuses on both quantitative and qualitative factors. The bigger lesson for UK teams is that board oversight and approval processes matter, not just the final disclosure note, as discussed in this piece on materiality and governance in related party transactions.

That's a useful reminder for trainees. A transaction can be important because of who is involved, even if the amount alone doesn't look dramatic.

Why this matters for your career

If you want to move toward audit, financial control, or business analysis, learning to think in controls gives you an edge. It shows you understand process, risk, and governance, not just posting.

A practical next step is to build your understanding of audit thinking through structured learning such as courses in auditing.

For readers who also deal with cross-border or specialist connected-party lending issues, this article on navigating related party loans for your SMSF gives a useful example of how relationship-based lending can create extra compliance risk in another setting.

Good controls don't slow a finance team down. They stop the team from having to explain weak records later.

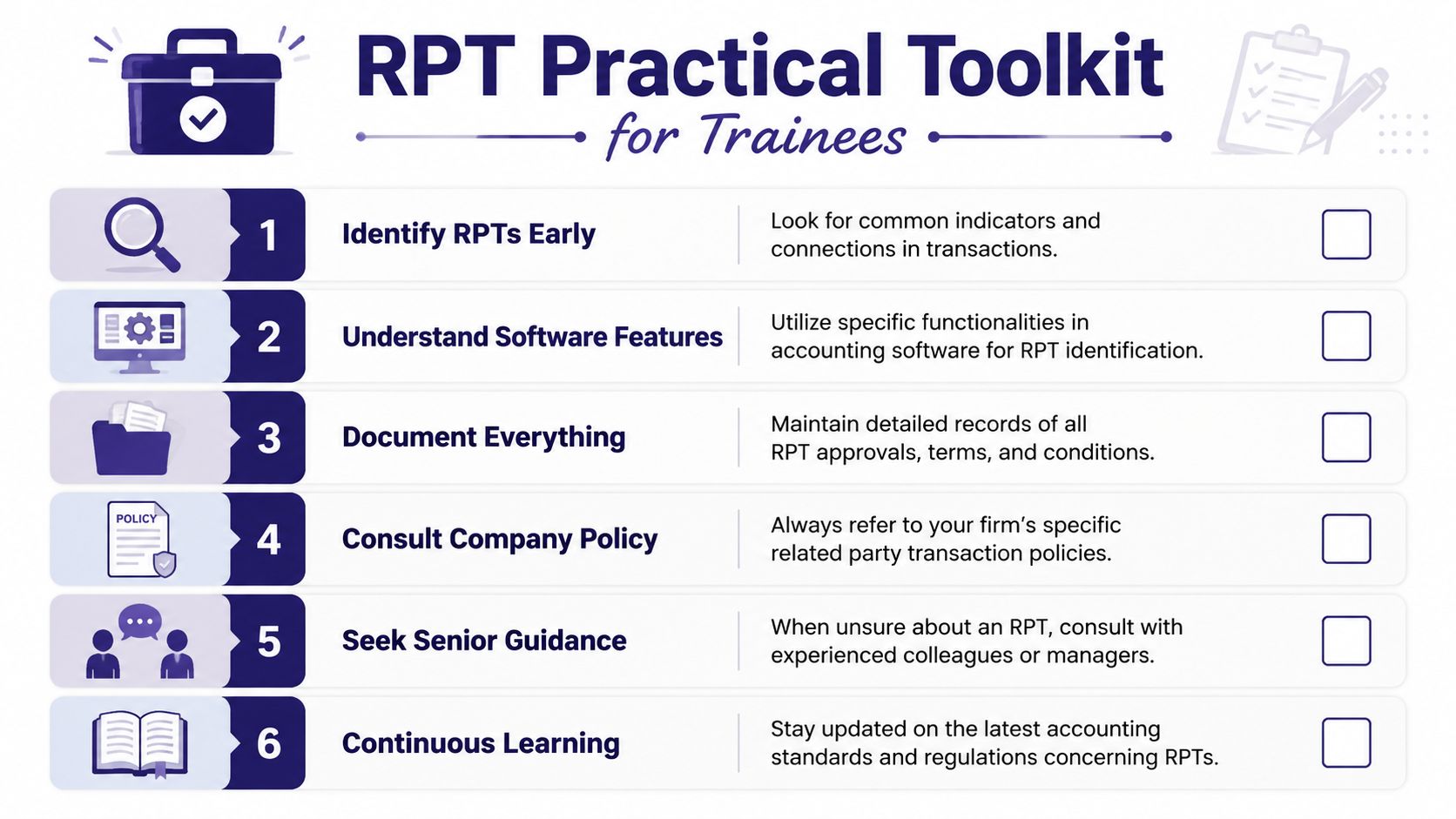

A Practical Toolkit for Trainees

The best way to handle related party transactions is to build them into your normal routine. Don't treat them as rare technical issues saved for the year-end accountant. If you do that, important details get lost.

Software habits that make life easier

In Xero, create a contact group or tracking label for related parties. That makes it easier to filter transactions and review balances before month end or year end.

In Sage, use clear nominal codes for director's loan accounts, intercompany balances, and key related liabilities. Avoid mixing these with ordinary trade creditors or general journals.

In QuickBooks, use well-named suppliers and customers, and add notes in the contact record when a counterparty is connected to a director, shareholder, or group company. Clean naming matters more than many trainees expect.

If you're studying standards alongside practical software work, this resource on International Accounting Standard 8 is also a helpful reminder that consistent accounting policies and careful judgement matter when transactions don't fit neatly into routine processing.

A job-ready checklist

Keep this checklist beside your month-end or year-end work:

- Identify the connection: Check whether the person or entity is linked to a director, shareholder, key manager, or group company.

- Code it clearly: Use the right ledger account from day one. Don't bury it in general overheads.

- Keep the evidence: Save contracts, invoices, emails, and approval notes together.

- Review balances: Look closely at anything outstanding at the period end.

- Ask about terms: Were payment timing, interest, security, or settlement unusual?

- Flag disclosure early: Let the year-end preparer know before the final accounts note is drafted.

- Escalate when unsure: A quick question today is better than an audit issue later.

For bookkeeping trainees, this improves coding and reconciliations. For payroll learners, it sharpens your awareness of director and key management payments. For accounts assistants, it supports stronger year-end files. For business analysts and data analysts, it builds the habit of looking for relationships behind the numbers, not just movements within them.

That's what employers notice. Not just whether you can process transactions, but whether you can understand them.

If you want practical, job-focused training in bookkeeping, VAT, payroll, accounts assistant work, final accounts, and accounting software, Professional Careers Training offers flexible support built around real UK finance roles. Their training includes 1-to-1 guidance from ACCA-qualified Chartered Accountants and CPD-approved trainers, plus hands-on help with Sage, Xero, QuickBooks, financial statements, and career support for trainees who want to become more confident and employable.