Your first bank reconciliation often feels harder than it should. The bank statement says one thing, the cash book says another, and every unmatched line...

Your first bank reconciliation often feels harder than it should. The bank statement says one thing, the cash book says another, and every unmatched line seems to raise a new question. If you're a new Accounts Assistant, a trainee bookkeeper, or a business owner doing your own records, that moment can feel like a test of whether you're really cut out for finance work.

It is a test, but not in the way generally understood.

Bank reconciliation isn't just about finding errors. It's about proving that the cash figure in the accounts can be trusted. That makes it one of the most practical skills you can learn early in a UK finance career, because employers need people who can work carefully, think logically, and turn messy transaction data into reliable records.

Why Mastering Bank Reconciliation Launches Your Accounting Career

A strong bank reconciliation process sits at the centre of day-to-day finance work. When a business knows its cash position is correct, it can pay staff, settle suppliers, prepare VAT returns, and produce management accounts with confidence. When that cash position is wrong, every report built on it becomes weaker.

That's why this task appears so often in job descriptions for Bookkeepers, Accounts Assistants, and junior finance staff. Employers aren't only asking whether you can tick matching lines in Xero, Sage, or QuickBooks. They want to know whether you can spot the difference between a simple timing issue and a real problem.

Why employers care about this skill

Bank reconciliation shows several employable strengths at once:

- Attention to detail. You need to compare dates, amounts, references, and posting logic.

- Commercial awareness. You learn how cash movement affects payroll, VAT, supplier payments, and final accounts.

- Problem-solving. Not every difference is an error. Some are normal timing items. Others need investigation.

- Software confidence. Modern roles often involve bank feeds, rules, and exception handling in systems such as Xero, Sage, and QuickBooks.

- Control mindset. Finance teams rely on reconciliation to support accurate reporting and reduce the chance of error or misuse.

Why it matters beyond bookkeeping

A candidate who understands reconciliation often progresses faster because the skill connects with other training areas.

In Bookkeeping & VAT, it supports accurate cash records and cleaner VAT return preparation.

In Accounts Assistant work, it supports purchase ledger, sales ledger, and month-end close.

In Advanced Payroll, it helps you check that payroll payments cleared as expected and that deductions were posted correctly.

In Final Accounts, it gives confidence that the cash figure on the balance sheet is not guesswork.

In Business Analyst and Data Analyst pathways, it builds a habit that matters everywhere in finance data work. Compare two datasets, isolate exceptions, explain variance, document the result.

Practical rule: If you can explain why two cash balances differ, you already think more like a finance professional than someone who only enters transactions.

Many learners first see bank reconciliation as a routine admin task. In practice, it teaches judgement. You learn what belongs in the books, what belongs on the bank side, what needs a journal, and what needs escalation. Those habits make you useful very quickly in a real finance team.

Laying the Groundwork Before You Begin

Students often want to jump straight into matching transactions. That's usually where frustration starts. A clean reconciliation begins before you compare a single line, because poor preparation creates confusion later.

What you need on your desk or screen

At minimum, gather the records for the same period:

- The latest bank statement for the account you're reconciling

- The cash book or general ledger report from the accounting system

- The previous reconciliation, so you can see whether old outstanding items were cleared

- Supporting records such as deposit records, payment listings, remittance advice, or notes about unusual items

This preparation matters because a reconciliation isn't performed in isolation. It carries forward from the prior period. If an old outstanding cheque still hasn't cleared, or a prior correction wasn't posted properly, this month's reconciliation will inherit that issue.

The terms that confuse beginners

Two items cause the most uncertainty.

Deposits in transit are amounts recorded in the books but not yet shown by the bank. This often happens when money is paid in near the end of the period.

Outstanding cheques are payments already entered in the books but not yet cleared by the bank.

Both are normal timing differences. They don't always mean anyone has made a mistake.

A useful way to think about them is simple. The books may know about a transaction before the bank does, or the bank may know about an item before the books do. Reconciliation is the method for bringing both views into agreement.

Why record quality matters in the UK

In the UK, reconciliation isn't just tidy housekeeping. HM Revenue & Customs requires VAT-registered businesses to keep business records that support VAT returns for at least 6 years, which means reconciliation evidence becomes part of a long-term control trail, not a short-lived monthly exercise, as noted in this explanation of bank reconciliation record-keeping and control evidence.

That point changes how you should treat your working papers. A reconciliation should be clear enough that someone else can follow it later. That includes a manager, an auditor, or a tax reviewer.

Keep every unmatched item traceable to source records. If you can't explain where it came from, you don't yet have a finished reconciliation.

Preparation skills that transfer into training

Learners in bookkeeping courses are often taught to connect reconciliation work with double entry, because every unexplained difference eventually leads back to posting logic. If you need a refresher, this guide to double entry bookkeeping fundamentals is a useful background read before you tackle more complex reconciliations.

Good preparation also builds habits that employers notice:

| Preparation task | Why it matters in practice |

|---|---|

| Check the statement period | Prevents matching the wrong month |

| Use the latest ledger report | Avoids investigating already-corrected items |

| Review prior outstanding items | Stops old problems being ignored |

| Gather supporting documents | Speeds up investigation of exceptions |

Professionals don't start with guesswork. They start with complete records.

The Core Reconciliation Procedure A Step-by-Step Walkthrough

The heart of the bank reconciliation process is a controlled flow. Compare what matches, isolate what doesn't, then adjust the books where needed until both adjusted balances agree.

A clear visual can help fix that flow in your mind.

Start with the easy matches

Begin by placing the bank statement beside the cash book or ledger report for the same period. Then work through line by line, matching identical items.

Look first for the straightforward entries:

- Regular supplier payments

- Customer receipts

- Standing orders and direct debits

- Payroll payments

- Card receipts that appear clearly and in full

As you match each line, mark it in a consistent way. Some teams use ticks on printed reports. Others use software status markers. The method matters less than the discipline. You need a visible record of what has been checked.

This early stage gives you a cleaner list of exceptions. It also stops you wasting time investigating items that already agree.

Separate timing differences from real errors

Once the obvious matches are cleared, focus only on the unmatched items. At this stage, beginners often get stuck, because every difference can look equally serious at first.

It helps to divide them into two broad groups.

Timing differences are expected gaps. A deposit may be in the ledger but not yet on the statement. A cheque may have been issued but not yet presented.

Errors or omissions need action. A bank charge may appear on the statement but not in the books. A payment may have been entered with the wrong amount. A receipt may have been posted to the wrong account or wrong date.

A practical control sequence is to compare the ending bank balance and the cash book, identify timing differences such as deposits in transit and outstanding cheques, adjust for bank-side items like fees and interest, then post journal entries so the adjusted bank balance equals the adjusted ledger balance, as set out in this bank reconciliation workflow guidance.

Post the adjustments in the right place

One of the most common misunderstandings is this. You do not change the bank statement. You only post entries in your own accounting records.

If the bank has charged a fee and you haven't recorded it yet, the journal goes into the books.

If the bank has added interest and it isn't in the ledger, the journal goes into the books.

If a cheque is still outstanding, that isn't a new journal entry. It is a reconciling item on the bank side.

That distinction is basic, but it matters a lot.

The reconciliation isn't finished when you find the difference. It's finished when you know whether that difference needs a journal, a carry-forward item, or an investigation.

To see the process demonstrated in another format, this short video is a helpful companion while you work through your own practice example.

Keep the workflow practical

A tidy working approach might look like this:

- Match obvious items first so only real exceptions remain

- List unmatched items clearly rather than holding them in your head

- Check dates and references before assuming an amount is wrong

- Post book adjustments promptly for fees, interest, and other bank-notified items

- Confirm the final equality between adjusted bank and adjusted book balances

If you want another plain-language example of the broader reconciliation task, a guide framed as a financial health check-up for Florida companies is useful because the core matching logic is the same even though the business context differs.

This is also why software training matters. Xero, Sage, and QuickBooks can speed up matching, but the accountant still has to recognise what the software is showing. A good trainee doesn't just click “OK”. They understand why the item belongs there.

Creating Your Bank Reconciliation Statement

A completed reconciliation must end in a document that proves what you did. That document is the bank reconciliation statement.

Managers don't want a verbal summary. Auditors don't want guesswork. They want a clear record showing how the opening differences were analysed and how the final adjusted balances were brought into agreement.

What the statement is trying to show

The statement tells a simple story.

The bank statement balance and the book balance are different for identifiable reasons. Those reasons are listed, classified, and applied to the correct side. After those items are considered, both sides arrive at the same adjusted figure.

That final agreement is the control point.

A simple worksheet structure

Below is a basic format you can use in training or in early practice work.

Sample Bank Reconciliation Worksheet

| Description | Book Balance Side (£) | Bank Balance Side (£) |

|---|---|---|

| Ending balance before reconciliation | ||

| Add deposits in transit | ||

| Less outstanding cheques | ||

| Less bank charges | ||

| Add interest received | ||

| Add or less correction entries | ||

| Adjusted balance |

You wouldn't fill every line on every reconciliation. The structure gives you a place for common reconciling items.

How to read each part

The ending balance before reconciliation is the starting point from each source. One comes from the bank statement. The other comes from the cash book or ledger.

The timing items usually sit on the bank side. Deposits in transit increase the bank-side adjusted view because the books already know about the money. Outstanding cheques reduce it because the books already show payments that the bank hasn't yet processed.

The book adjustments usually include items first seen on the statement, such as charges or interest. These belong in the company's own records.

A correction entry may be needed where the business posted something incorrectly, such as a duplicated transaction or a wrong amount.

Why classification matters

A strong reconciliation doesn't just list differences. It explains them in a disciplined way. If your statement has a vague line such as “miscellaneous difference”, that usually means the work isn't finished.

Good documentation should answer these questions:

- What is the item

- Why is it causing a difference

- Which side does it affect

- Does it need a journal

- Will it clear next period or does it need follow-up

A reconciliation statement should let another person retrace your logic without asking you to sit beside them.

What a reviewer expects to see

A reviewer usually looks for five things:

| Review point | What it tells them |

|---|---|

| Clear period date | You reconciled the correct month |

| Named reconciling items | Differences were understood, not hidden |

| Correct side treatment | You know what belongs to bank side and book side |

| Adjusted balances agree | The control worked |

| Supporting evidence retained | The work can be checked later |

This is one reason reconciliation is valuable in training for final accounts and accounts assistant roles. The finished statement is not just paperwork. It is evidence of competence. It shows that you can take raw financial data, analyse variances, and present a defendable result.

That same discipline also helps in business analyst and data analyst work. You are comparing two data sources, classifying outliers, and documenting the logic behind your result. The software and subject may change. The thinking process doesn't.

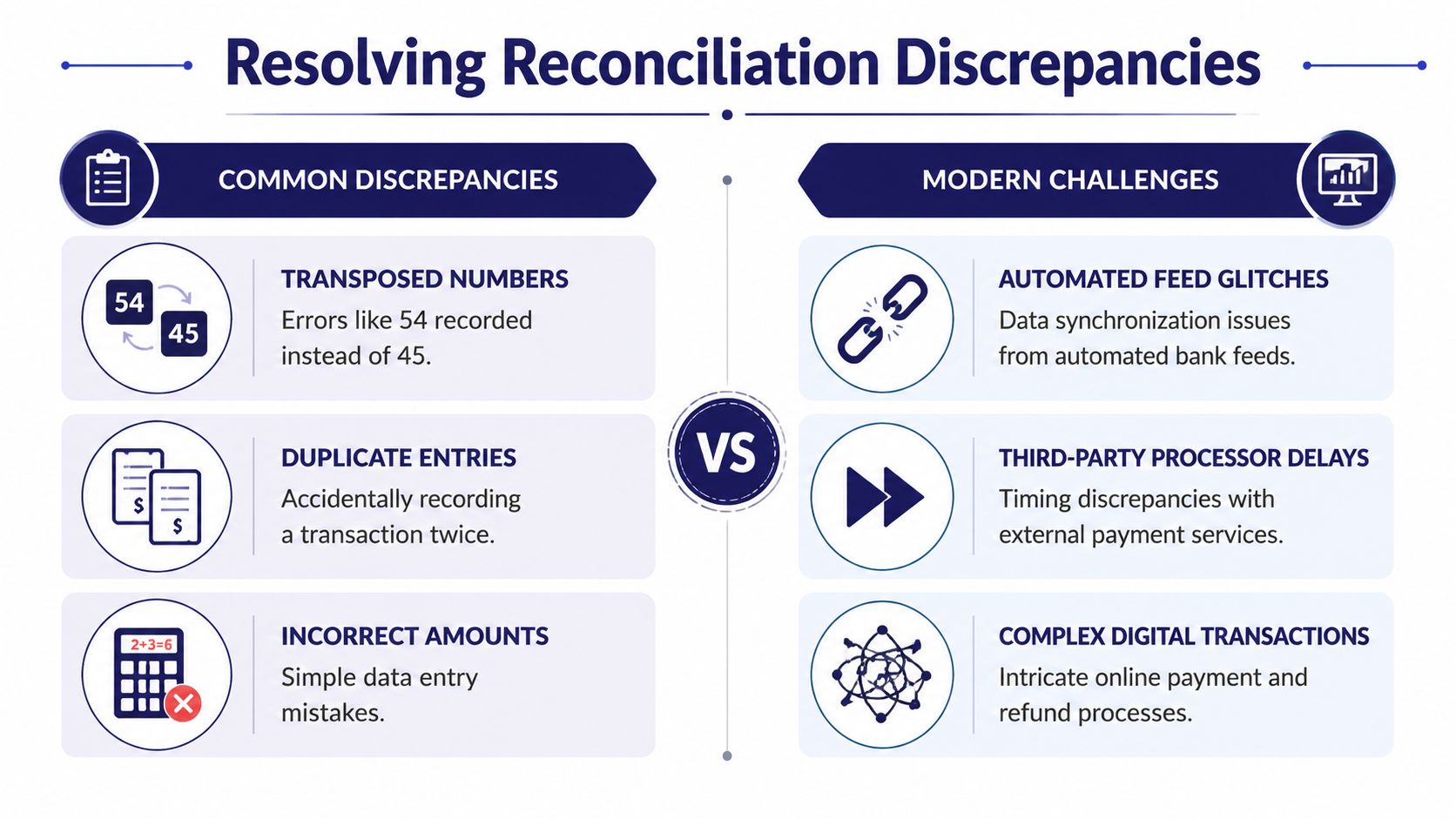

Troubleshooting Common Discrepancies and Modern Challenges

You finish the month-end reconciliation, but the bank still does not agree. The difference is small enough to tempt a quick adjustment and large enough to worry a reviewer. That moment tests more than accuracy. It tests judgement, documentation, and the habit of asking what the difference is really telling you.

This part of the bank reconciliation process often separates a trainee who can post entries from one who can support a finance team with confidence. Employers value that difference. It is the same mindset developed in Bookkeeping & VAT and Accounts Assistant training, then applied in Xero, Sage, and QuickBooks environments where bank feeds move fast but errors still need a human explanation.

The discrepancies trainees usually meet first

Start with the simplest explanation and work outward. Bank reconciliation works like checking two versions of the same story. If one version says £54 and the other says £45, the issue may be a typing error rather than a missing transaction.

Common examples include:

- Transposed numbers, such as entering 54 instead of 45

- Duplicate entries, where the same receipt or payment is posted twice

- Incorrect amounts, where the transaction is real but the value is wrong

- Missing book entries, such as bank charges, interest, or direct debits not yet recorded

- Timing differences, where the item exists but falls into a different accounting period

These are not just exam-style problems. They are everyday finance issues, and solving them shows the kind of care employers expect from junior accounting staff.

Classify the difference before you correct it

A useful habit is to sort each unmatched item by type before posting anything. That slows you down in a good way.

A practical structure is to group items into deposits in transit, outstanding cheques, bank charges, interest, debit or credit memoranda, and correction entries, as explained in this guidance on exception types in bank reconciliation. Once the item has a category, the next question becomes easier. Is it a timing item, a posting error, or something that needs investigation?

That approach also mirrors good software practice. If you want to build confidence with cloud systems, this overview of accounting software used in business accounts helps show why employers look for candidates who understand both bookkeeping logic and the systems that process it.

Modern payment flows create harder matching problems

Older training examples often assume one bank line matches one ledger entry. Real businesses are rarely that tidy.

A card processor may deduct fees before payout. An online platform may bundle dozens of customer receipts into one settlement. A refund may appear on a different day from the original sale. By period end, the bank may show one net amount while the ledger shows sales, fees, refunds, and clearing balances across several dates.

You might see:

- Net settlements where fees are taken before cash reaches the bank

- Batched payouts covering many transactions in one deposit

- Refund timing gaps between the sale date and the refund date

- Delayed settlements arriving after the month-end cut-off

- Split-source evidence where one bank line must be traced to the ledger, processor report, and fee breakdown

Software certification demonstrates its career relevance. A candidate who can explain one-to-many matching in Xero, trace settlement reports in QuickBooks, or review imported transactions in Sage is far more useful to an employer than someone who only knows the paper version of reconciliation.

If a bank line does not match one ledger line, check whether it represents a batch payout, a net settlement, or a timing delay before assuming it is wrong.

Repeated differences often point to process weakness

Some items are innocent timing differences. Some are warning signs.

If the same old reconciling item appears month after month, the problem may be poor posting discipline, weak review, or an unresolved control failure. If supplier bank details change without clear approval, or payments appear without supporting documents, the issue may go beyond bookkeeping accuracy into risk management.

That is why regular reconciliation supports preventing internal fraud. It helps finance staff spot duplicate payments, unusual withdrawals, unexplained journals, and transactions that do not fit the normal pattern of the business. UK fraud guidance from the National Crime Agency also shows why firms need routine checks that identify suspicious activity early rather than after the loss is discovered.

Signs that need escalation, not a quick fix

A good accounts assistant knows when to stop forcing a match and raise a question.

| Warning sign | Why it matters |

|---|---|

| The same outstanding item appears repeatedly | It may no longer be a genuine timing difference |

| A supplier payment goes to unfamiliar bank details | The change may need approval and verification |

| A transaction has no invoice, remittance, or clear source record | The audit trail is incomplete |

| Corrections are posted each month for the same issue | The root cause has not been fixed |

| A settlement amount cannot be traced to fees, receipts, and refunds | The payment flow may not be understood properly |

That judgement makes reconciliation a career-building skill. It shows you can do more than clear transactions. You can examine evidence, question anomalies, document risk, and protect the reliability of the accounts.

Optimising Your Process with Software and Controls

Manual reconciliation still teaches the principles well, but most UK finance teams now work with digital bank feeds and cloud accounting systems. That shift changed the rhythm of the bank reconciliation process. What used to be a paper-based month-end task can now happen far more frequently inside the software.

Guidance from accounting software providers says firms should reconcile at least monthly, while high-transaction businesses may do so weekly or daily, and the wider move to digital bank feeds has made that possible, as explained in this overview of bank reconciliation and digital accounting workflows.

What software does well

Xero, Sage, and QuickBooks can handle a large share of the routine work:

- Importing bank transactions automatically

- Suggesting likely matches

- Applying bank rules to recurring items

- Flagging exceptions for review

- Keeping an audit trail of postings and changes

For a trainee, these systems can feel almost magical at first. A feed arrives, suggested matches appear, and the account starts to clear quickly.

That speed is useful, but it creates a risk. Some users accept software matches without understanding them.

Why understanding still matters more than clicking

Software can suggest. It cannot take professional responsibility.

A strong finance candidate knows when to accept a match, when to split an entry, when to create a correction, and when to stop and investigate. Employers value that skill more than basic button-pressing because software only works well when the setup and review are sound.

This is especially relevant when connected tools are involved. If the bank feed misreads a reference, if a payment app batches transactions, or if a rule posts to the wrong nominal code, someone has to diagnose the issue.

That's also why broader software literacy helps. A learner who understands accounting software settings, ledger behaviour, and reporting logic is better prepared to manage real finance workflows. This guide to software used for business accounts gives a useful overview of the systems often seen in training and practice.

Controls make the process trustworthy

The best reconciliation process is not just fast. It is defensible.

A few controls matter more than most:

- Separate preparation from review. One person prepares the reconciliation, another checks it.

- Review old outstanding items. Don't let stale differences drift forever.

- Keep supporting documents together. A finished reconciliation should be easy to review later.

- Restrict changes to master data. Supplier bank details and posting rules need careful control.

If you're thinking about the fraud angle, practical reading on preventing internal fraud gives useful context for why review procedures and separation of duties matter so much around cash.

The employability angle

It is at this stage that bank reconciliation becomes bigger than bookkeeping.

In Advanced Payroll, controls help confirm payroll cash movements and spot unusual withdrawals.

In Final Accounts, a strong reconciliation supports reliable year-end balances.

In Business Analyst and Data Analyst work, system logic, exception handling, and audit trails translate directly into better data governance habits.

A candidate who can use Xero, Sage, or QuickBooks and explain the accounting behind each matched and unmatched line stands out. That's the difference between software familiarity and job-ready capability.

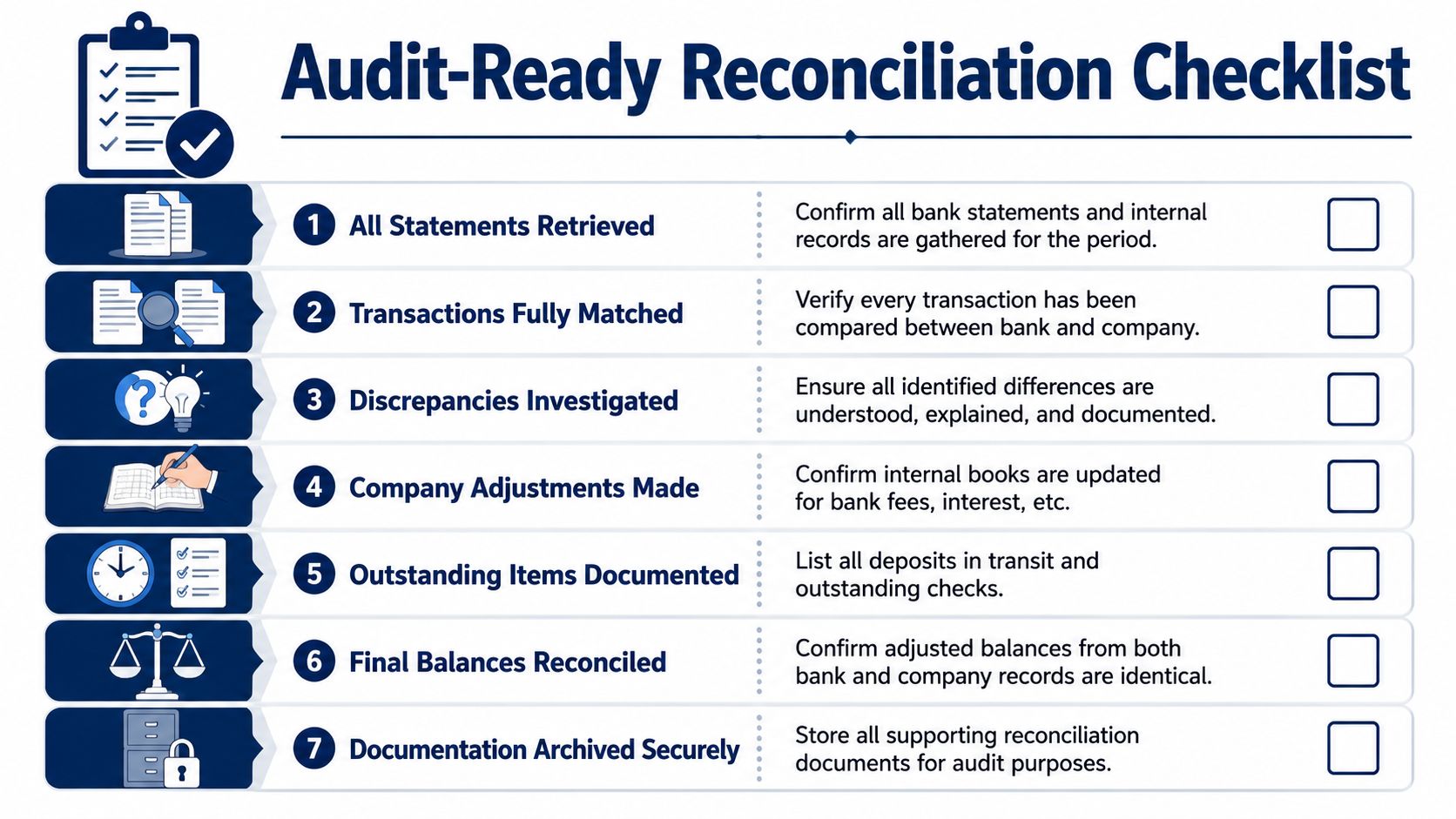

Your Audit-Ready Bank Reconciliation Checklist

It is 4:45 on a Friday. A manager asks for proof that the cash figure in the accounts can be trusted before reports go out. If your reconciliation is clear, supported, and easy to follow, that request is routine. If it is patchy, the same request turns into a scramble through emails, statements, and old notes.

That is why this final check matters so much. In real finance roles, bank reconciliation is not judged only by whether the numbers agree. It is judged by whether another person can review your work, follow your reasoning, and see exactly how you dealt with every difference. That standard is taught early in Bookkeeping & VAT and Accounts Assistant training because employers want people who can produce work that stands up to review in Xero, Sage, and QuickBooks, not just click "match" and hope for the best.

Use this final check before sign-off

- All records gathered. You have the bank statement, cash book or ledger, prior reconciliation, and the backup for unusual items. Missing paperwork is like trying to mark an exam with half the pages gone.

- Matched items cleared. Routine receipts and payments have been compared and marked off properly in the ledger or software.

- Exceptions classified. Each difference is labelled for what it is, such as timing, bank charge, interest, error, or duplicate entry. "Unexplained difference" is not a useful category.

- Book-side journals posted. Charges, interest, bounced payments, and corrections have been entered in the books where needed.

- Outstanding items listed clearly. Unpresented cheques and outstanding lodgements are dated and described so they can be checked in the next period.

- Adjusted balances agree. After all valid adjustments, the bank figure and book figure match.

- Evidence filed securely. A reviewer should be able to pick up the file later and understand the whole story without asking you to rebuild it.

The standard employers recognise

A good reconciliation answers three practical questions.

| Question | What the work should prove |

|---|---|

| Can I trust the cash figure | Yes, because every difference is identified and supported |

| Can I retrace the logic | Yes, because the matching, adjustments, and outstanding items are clearly shown |

| Can this be reviewed later | Yes, because the documents and explanations are complete |

This is one reason reconciliation links so closely to employability. A trainee who can prepare a tidy reconciliation is showing more than bookkeeping accuracy. They are showing judgement, organisation, software discipline, and an understanding of audit trail. Those are the habits employers look for in junior finance staff and the same habits assessed in practical training and software certification work.

If you want to strengthen the reporting side as well, this guide on how to prepare financial statements helps connect reconciled cash to reliable year-end accounts.

There is a wider professional lesson too. The careful review used in reconciliation, checking inputs, tracing exceptions, and documenting decisions, is the same mindset teams use when they compare enterprise AI systems for finance operations. Good finance staff do not accept outputs at face value. They test how those outputs were produced.

Clean reconciliation work shows that the person who prepared it can be trusted with financial responsibility.

If you want to build that level of job-ready confidence, Professional Careers Training offers practical accountancy training designed for real UK roles. Learners can develop hands-on skills across Bookkeeping & VAT, Accounts Assistant, Advanced Payroll, Final Accounts, and software certifications in Sage, Xero, and QuickBooks, with flexible study options, tutor support, and career-focused guidance that helps turn technical knowledge into employable capability.