You're probably in one of two places right now. You're either studying bookkeeping or accounting and keep seeing the term trial balance accounting in class...

You're probably in one of two places right now. You're either studying bookkeeping or accounting and keep seeing the term trial balance accounting in class notes, or you've started using Xero, Sage, or QuickBooks and noticed a report called Trial Balance without feeling fully sure what it proves.

That's normal. Many trainees can post invoices, record payments, and enter journals, but they get stuck when someone asks, “Can you check the trial balance before month-end?” That question matters because it sits right at the point where bookkeeping turns into dependable financial reporting.

If you want to work in bookkeeping & VAT, advanced payroll support, an accounts assistant role, final accounts preparation, or even move into business analyst or data analyst work where finance data needs to be trusted, this is one of the core skills to grasp. A trial balance helps you test whether the ledger stands on solid ground before anyone builds reports on top of it.

Why Every Trainee Accountant Must Master the Trial Balance

At the end of a reporting period, the pressure changes. During the month, a trainee might post supplier invoices, raise sales invoices, record receipts, enter payroll journals, and code bank payments. Then month-end arrives, and someone needs to check whether the books make sense.

That's where many beginners realise accounting isn't just data entry. It's judgement.

Take a common trainee task. You've been helping a small business record transactions throughout the month. The purchase ledger looks fine. The sales ledger looks active. Bank entries are in. But before anyone can rely on the figures, someone has to pull the ledger balances together and confirm the debits and credits line up. That checkpoint is the trial balance.

Why employers care about it

A hiring manager for an Accounts Assistant role doesn't just want someone who can click buttons in software. They want someone who understands what sits underneath the reports. The same is true for Bookkeeper roles. If you can explain how a trial balance is prepared, how you'd spot an issue, and what you'd do next, you sound job-ready.

That matters in several training pathways:

- Bookkeeping & VAT: You need clean ledgers before VAT work can be trusted.

- Advanced payroll: Payroll journals affect wages, tax, pension, and control accounts. If postings are wrong, the trial balance often shows the strain.

- Accounts assistant work: Month-end routines often include checking ledger balances and reviewing unusual postings.

- Final accounts: You can't prepare reliable accounts if the underlying balances are questionable.

- Business analyst and data analyst roles: Finance data only helps decision-making when the underlying records are consistent.

Practical rule: If you can read a trial balance confidently, you're no longer just entering figures. You're checking the quality of the accounting system.

It's an employability skill, not just an exam topic

This is why colleges and training providers keep returning to trial balances. It's one of the first places where theory, software, and real work meet. In interviews, candidates who understand trial balance accounting usually come across as more grounded because they can connect transactions, ledgers, and reports in a single line of thought.

That's exactly what employers want from junior finance staff.

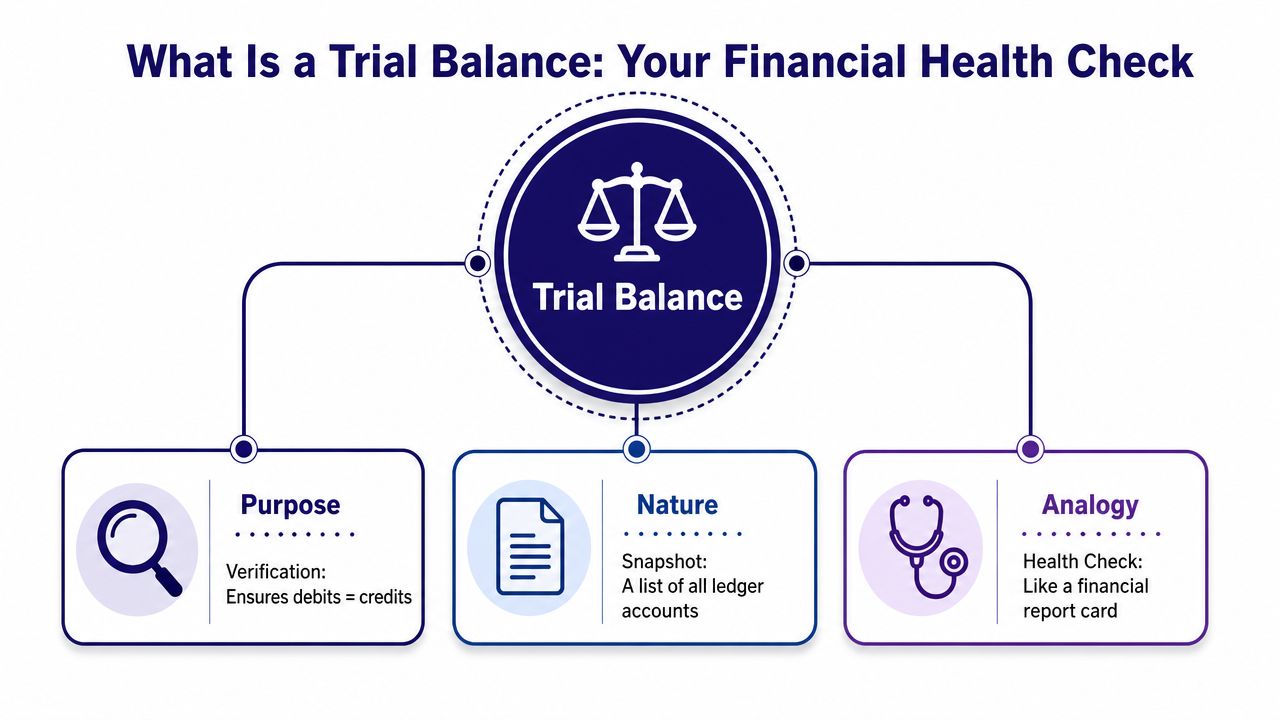

What Is a Trial Balance in Accounting

You are in your first week as an Accounts Assistant. The finance manager asks you to check the trial balance before month-end. If you know what you are looking at, you can spot whether the bookkeeping records are ready for the next stage. If you do not, the report looks like a long list of account names and figures.

A trial balance is a list of ledger balances shown in two columns, debit and credit, to check whether the books are arithmetically balanced. It sits partway through the accounting process, after transactions have been posted to the ledgers and before the final accounts are prepared.

The simple idea behind it

A trial balance works like a checkout total after you have scanned every item. You are not reviewing whether each purchase was wise. You are checking whether the system has captured everything in balance.

That balance comes from double-entry bookkeeping. Each transaction affects at least two accounts, with debits matching credits. A trial balance pulls those closing balances together so you can test whether that rule still holds across the full ledger. If you want to strengthen that foundation, this guide to double-entry bookkeeping basics explains the logic clearly.

Here is the idea in a simple sequence:

| Stage | What it shows |

|---|---|

| Transactions recorded | Business activity has been entered |

| Ledger balances extracted | Each account has a closing balance |

| Trial balance totalled | Total debits and total credits can be checked |

What a trial balance actually does

Its first job is to check arithmetic agreement in the books. If total debits do not equal total credits, something needs attention. That could be a posting error, a casting mistake, or a missing entry.

Its second job is practical. It gives the bookkeeper or accounts assistant a working list of balances to review before preparing reports such as the profit and loss account and balance sheet. In real workplaces, especially in Xero, Sage, and QuickBooks, this is one of the reports junior finance staff are often asked to export, scan, and question.

That is why employers ask about it in interviews. If you can explain what a trial balance is, what it checks, and what it does not check, you sound like someone who can support month-end work rather than someone who has only memorised definitions.

What it does not tell you

A balanced trial balance does not prove every entry is correct. It only shows that the debit total equals the credit total.

Students often miss this point. If rent has been posted to the wrong expense account, the trial balance can still balance. If a transaction has been omitted completely, the trial balance can still balance. The report is a control tool, not a guarantee that every accounting decision was right.

Trial balance vs balance sheet

This is a common point of confusion.

A trial balance is an internal list of all ledger balances, including income, expenses, assets, liabilities, and capital. A balance sheet is a formal financial statement showing financial position at a given date. One helps you check the bookkeeping records. The other presents part of the final result.

If you are aiming for a Bookkeeper or Accounts Assistant role, being able to explain that difference clearly is useful on your CV and in interviews. It shows you understand both the bookkeeping process and the reports produced from it.

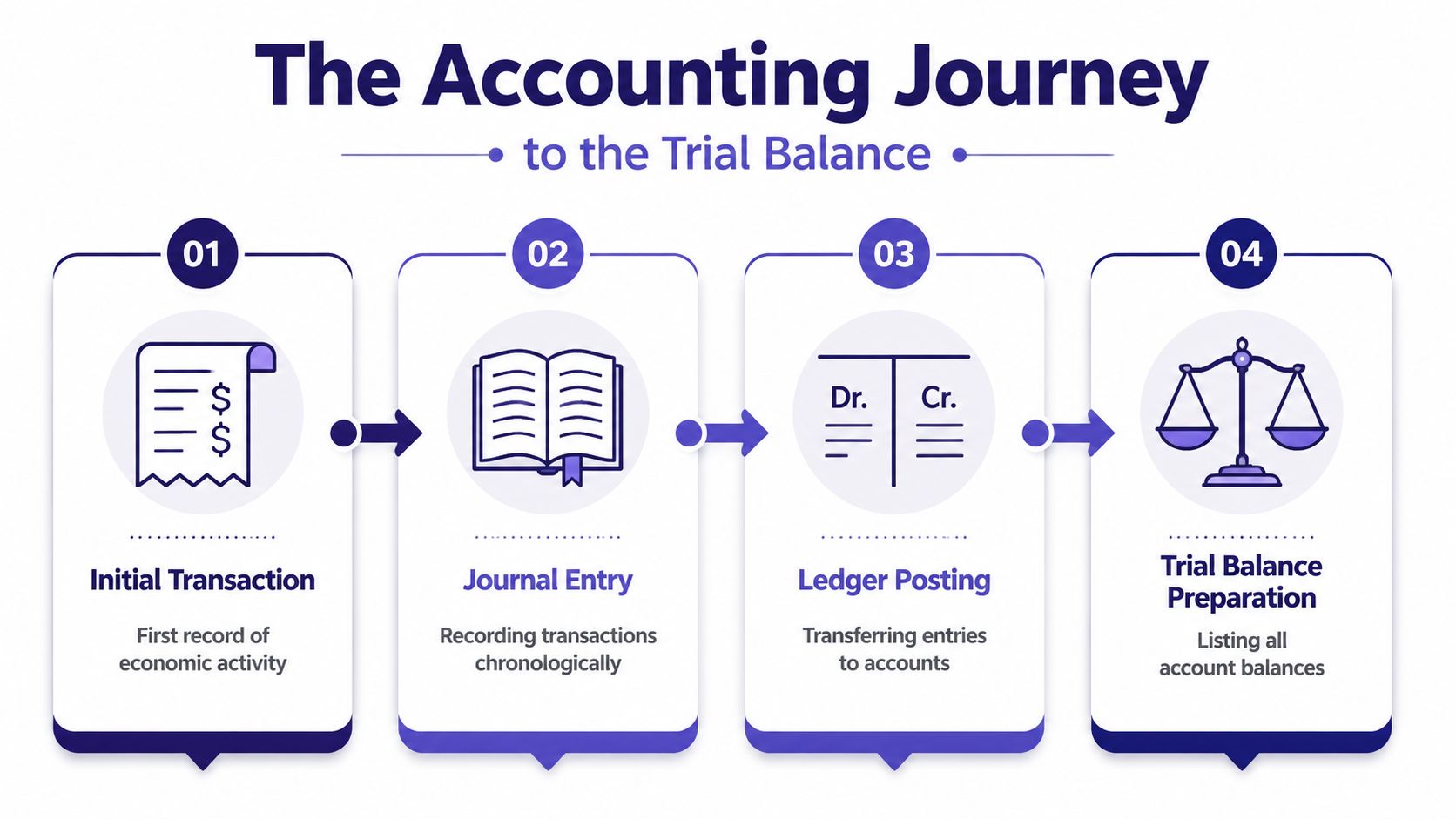

The Accounting Journey to the Trial Balance

A trial balance makes much more sense when you stop seeing it as a standalone report. It's the result of a chain of accounting steps. Each step feeds the next.

A business transaction begins with evidence. That might be a sales invoice, a supplier bill, a till receipt, a bank statement line, or a payroll report. Someone then records that event in the accounting records. After that, the figures are posted into the relevant ledger accounts. Only then can the business pull those balances into a trial balance.

From transaction to journal

Suppose a business buys office supplies and pays by bank transfer. The source document might be the supplier invoice and the payment confirmation. The accountant or bookkeeper records the transaction by recognising both sides of the entry.

At this stage, trainees often focus on the wording of the transaction. What matters more is the logic. Which account receives the debit, and which account receives the credit?

From journal to ledger

Once transactions are recorded, they sit in individual ledger accounts. Cash has its own ledger. Sales has its own ledger. Rent, wages, VAT, trade receivables, and trade payables all sit in their own places.

By the end of the reporting period, each ledger has a closing balance. That closing balance is what gets lifted into the trial balance.

Here's the flow in plain terms:

A transaction happens

A sale, purchase, payment, receipt, payroll run, or adjustment takes place.It gets recorded

The transaction is entered with debit and credit logic.It lands in the ledger

Each account builds up activity during the period.Balances are extracted

The closing figure from each account is transferred to the trial balance.

If you can explain this journey in an interview, you sound like someone who understands accounting systems rather than someone who has only memorised definitions.

Why this flow matters in real jobs

In bookkeeping and accounts assistant work, you often won't prepare everything from scratch by hand. Software does much of the posting. But employers still expect you to understand the path from source document to ledger to report.

That's also useful outside pure accounting roles. A business analyst may need to understand where finance data comes from before using it in reporting. A data analyst working with finance extracts needs to know that bad inputs in the ledger will flow into every downstream report.

The trial balance is where that full journey becomes visible.

How to Prepare a Trial Balance Step by Step

Preparing a trial balance is methodical. It isn't glamorous, but it's one of the cleanest ways to show that you understand bookkeeping properly.

The process is supported by a standard UK memory aid. As explained by First Intuition on the trial balance and DEAD CLIC, the DEAD CLIC mnemonic helps you decide where balances belong. DEAD means Debits = Expenses, Assets, Drawings. CLIC means Credits = Liabilities, Income, Capital. The same source also outlines the four-step process: list all ledger account balances, record debit and credit balances in their respective columns, sum each column, and investigate if they don't match.

Use DEAD CLIC first

This mnemonic saves trainees a lot of hesitation.

DEAD

Expenses, Assets, Drawings normally appear on the debit side.CLIC

Liabilities, Income, Capital normally appear on the credit side.

If you're unsure where a ledger balance should sit, start there.

The four practical steps

1. List every closing ledger balance

Take the balances from the general ledger at the reporting date. Don't guess and don't skip accounts. Include cash, bank, receivables, payables, capital, sales, expenses, and any other live account.

2. Place each balance in the correct column

Assets and expenses usually go into the debit column. Liabilities, income, and capital usually go into the credit column. Drawings also sit with debits.

3. Add both columns

Total the debit column. Then total the credit column.

4. Investigate any mismatch

If the totals differ, stop there. Don't push ahead into final accounts or reporting. Check the ledger balances, account classifications, and postings.

Worked example for ABC Services

Below is a simple teaching example. It's designed to show the layout and the logic, not to imitate every account a real business might hold.

Sample Trial Balance for "ABC Services" as at 31 December 2026

| Account Name | Account Type (DEAD/CLIC) | Debit (£) | Credit (£) |

|---|---|---|---|

| Cash | DEAD | 8,000 | |

| Trade Receivables | DEAD | 2,500 | |

| Equipment | DEAD | 6,000 | |

| Drawings | DEAD | 1,000 | |

| Rent Expense | DEAD | 1,200 | |

| Salaries Expense | DEAD | 2,300 | |

| Trade Payables | CLIC | 2,000 | |

| Bank Loan | CLIC | 4,000 | |

| Capital | CLIC | 10,000 | |

| Sales | CLIC | 5,000 | |

| Interest Received | CLIC | 2,000 | |

| Totals | 21,000 | 21,000 |

How to read the example

Notice what's happening here.

Cash, trade receivables, and equipment are assets, so they sit under DEAD in the debit column. Rent expense and salaries expense are expenses, so they also go in debit. Drawings is part of DEAD too.

On the credit side, trade payables and bank loan are liabilities. Capital is capital. Sales and interest received are income. They all sit under CLIC.

Memory trick: Don't try to memorise dozens of account rules one by one. Learn DEAD CLIC properly and classify each account from there.

What this teaches you for work

When you can prepare a trial balance manually, software reports become easier to interpret. If Sage shows an unexpected debit balance on a liability account, or Xero produces a figure that looks odd in an income code, you'll understand why that matters.

That's why trial balance accounting matters in practical training for bookkeeping & VAT, accounts assistant work, and final accounts. It also sharpens your confidence with payroll journals, control accounts, and software-based reporting.

Common Trial Balance Errors and How to Fix Them

You are at month-end in an Accounts Assistant role. Xero says the trial balance is out by £90, your supervisor wants the draft figures before lunch, and you need to work out whether the problem is a simple input mistake or something deeper in the ledger.

That is why this topic matters in real work.

A trial balance helps you spot arithmetic problems quickly, but it does not confirm that every posting is correct. Trainees often assume, “if it balances, it must be right.” In practice, that is one of the easiest ways to miss errors that later create trouble in bank reconciliations, VAT checks, or management accounts.

Errors that often make the trial balance disagree

Start with the errors that break the arithmetic. These are usually easier to find because the debit and credit totals no longer match.

| Error type | What it looks like | What to check |

|---|---|---|

| Transposition error | Numbers are reversed, such as £54 instead of £45 | Compare the entry to the invoice, receipt, or journal |

| One-sided entry | Only the debit or only the credit is posted | Review the full double entry for the transaction |

| Incorrect ledger total | The account balance has been added up wrongly | Recalculate the ledger account line by line |

| Balance in the wrong column | A debit balance is shown as credit, or the reverse | Check the account type and normal balance |

A good way to picture this is a set of weighing scales. If one side is heavier, you know something has gone wrong with the totals or the placement of an amount. In bookkeeping jobs, these are often the first checks you make before asking whether the issue sits in the original invoice posting, a journal, or an imported bank transaction.

Errors that a balanced trial balance can still hide

This is the part that catches many trainees.

A trial balance can agree perfectly and still contain wrong accounting. The maths works, but the logic does not.

Here are the main hidden errors:

| Error type | What happens | Why the trial balance still balances | How to fix it |

|---|---|---|---|

| Omission | A transaction is missed completely | Neither side is entered | Match source documents to the ledger |

| Commission | The amount goes to the wrong account of the same type | Debit and credit entries still exist | Check account names, codes, and descriptions |

| Principle | The posting goes to the wrong class of account | Both sides are posted, but one is classified wrongly | Review whether the item belongs in asset, expense, liability, capital, or income |

For example, if you post equipment as repairs expense, the trial balance may still balance. The debit and credit are both there. The problem is classification. That matters in job roles such as Bookkeeper and Accounts Assistant because your manager may rely on those figures to review profit, costs, and asset values.

This is also why trial balance checking and reconciliation are taught together in good training. A trial balance checks ledger agreement. Reconciliation checks whether the ledger agrees with outside evidence, such as bank statements, supplier statements, or control accounts. If that distinction still feels unclear, this guide to reconciliation in accounting will help.

If your team wants to streamline closing cycles with reconciliation, that process often reveals the errors a balanced trial balance cannot show.

A practical routine for finding the problem

Use a clear order. It saves time.

Confirm the difference

Check whether the mismatch comes from the trial balance totals or from an earlier ledger calculation.Look at recent postings first

Fresh entries are common error points, especially after busy invoice runs, payroll journals, or manual adjustments.Scan for unusual balances

An expense account with a credit balance or a liability with a debit balance deserves attention.Trace back to the source document

Review invoices, bank entries, supplier statements, payroll reports, and journals.Check account classification

If the trial balance agrees but the figures still look odd, ask whether the transaction was posted to the right type of account.

This routine is useful in software as well as manual work. In Sage or Xero, you may not be adding columns by hand, but you still need to recognise when a balance looks wrong and know how to investigate it. That is exactly the sort of judgment employers ask about in interviews for trainee finance roles.

A strong CV does not need to claim years of experience. It helps to say you can prepare and review a trial balance, identify common error types, and trace discrepancies back to ledger entries or supporting documents. In an interview, be ready to explain one example clearly: “I would first check whether the trial balance is out because of a one-sided entry, a transposition error, or a ledger total mistake. If it balances, I would then test for omission, commission, or principle errors.”

For a visual walk-through of error spotting and correction, this short video is helpful:

A balanced trial balance shows arithmetic agreement. It does not prove that every posting is sensible.

Trainees who understand that difference are easier to trust with month-end work.

Trial Balances in Xero Sage and QuickBooks

Manual preparation teaches the logic. Software handles much of the processing.

In Xero, Sage, and QuickBooks, the trial balance is usually generated directly from the ledger. Once transactions have been posted, the software can produce the report quickly. That's useful in real jobs because month-end work often depends on speed as well as accuracy.

But automation doesn't remove the need for understanding. It changes your role.

What software does and what you still do

| Software task | Your task |

|---|---|

| Pulls balances into a report | Check whether the balances make sense |

| Totals debit and credit columns | Investigate unusual or unexpected figures |

| Filters by date or period | Confirm the right period has been selected |

| Exports data for reporting | Explain the numbers clearly to others |

If you're comparing the main platforms, this guide on QuickBooks vs Xero vs Sage is a useful place to start.

This matters in bookkeeping & VAT and accounts assistant roles because employers often ask for software familiarity. It also matters for business analyst and data analyst pathways. Finance software can generate reports, but someone still needs to understand whether the report is trustworthy.

Using Trial Balance Skills to Boost Your Accounting Career

Trial balance knowledge turns into career value surprisingly fast. In junior finance roles, it shows you can do more than process transactions. It shows you can check them.

As noted by Xero's guide to trial balances, the trial balance serves as the basis for preparing the main financial statements, the balance sheet and the profit and loss account, making it the foundational link between ledger data and final accounts for UK accountants and trainees entering professional careers in accountancy. Auditors often rely on it to decide which accounts to review during annual audits.

How to present this skill on your CV

Use direct wording. For example:

- Prepared and reviewed trial balances to verify ledger accuracy before month-end reporting

- Investigated ledger discrepancies and corrected posting errors

- Worked with Xero, Sage, or QuickBooks to produce trial balance reports

- Supported final accounts preparation using trial balance data

- Reviewed payroll and expense postings to maintain balanced ledgers

How to answer interview questions well

If an interviewer asks, “What is a trial balance?” don't stop at a textbook definition. Explain what it helps you do in practice.

A strong answer sounds like this in plain English: it's an internal report that lists ledger balances, checks that debits and credits agree, and gives you a reliable base for later reporting. Then add how you'd investigate if something didn't match, or how you'd review unusual balances even when the report balanced.

Interview advice: Employers remember candidates who connect the trial balance to month-end work, software use, and error checking.

This skill supports several job routes. It's core for Bookkeeper, Accounts Assistant, and Final Accounts work. It also strengthens your profile in roles where finance data feeds analysis, including business analyst and data analyst positions.

If you want to build real confidence in trial balance accounting, bookkeeping & VAT, advanced payroll, accounts assistant duties, final accounts, and finance software such as Xero, Sage, and QuickBooks, Professional Careers Training offers practical training designed around job-ready skills. Their support includes 1-to-1 training with ACCA qualified Chartered Accountants and CPD approved trainers, flexible weekday, evening, and weekend study options, official certification in Sage, Xero, and QuickBooks, plus CV preparation, career coaching, job hunting strategy, LinkedIn optimisation, and employer referrals.