You're probably in one of these situations right now. You've prepared a draft profit figure in Sage, Xero, or an Excel working paper, then someone...

You're probably in one of these situations right now. You've prepared a draft profit figure in Sage, Xero, or an Excel working paper, then someone more senior changes the tax line and your neat numbers no longer tie. Or you're studying bookkeeping and VAT, advanced payroll, final accounts, or an accounts assistant course and wondering why tax in financial statements feels so different from the tax rules you've seen elsewhere.

That gap is where IAS 12 starts to matter.

For UK trainees, International Accounting Standards 12 can feel technical at first, but it solves a very practical problem. It explains why the tax shown in the accounts often differs from what a company will pay to HMRC right now, and how to record that difference properly. Once you understand that, you stop treating tax as a mysterious adjustment and start reading accounts with more confidence.

Why IAS 12 Matters for Your UK Accounting Career

A common trainee moment goes like this. You take profit before tax, multiply it by the corporation tax rate, and expect that to be the tax charge. Then the final accounts show something else. At first, that looks like an error. Usually, it isn't.

The reason is simple. Accounting profit and taxable profit are not the same thing. Financial statements follow accounting standards. Tax returns follow tax law. IAS 12 sits between those two worlds and helps you report the tax effects properly.

Where trainees meet IAS 12 in real work

If you're training for roles in accounts assistant, final accounts, or even business analyst and data analyst positions in finance teams, IAS 12 turns up more often than you might expect.

- Accounts assistants see it when fixed asset schedules and tax workings don't match.

- Bookkeeping and VAT trainees meet it when postings are correct commercially but need different tax treatment later.

- Advanced payroll learners benefit because payroll journals often feed the wider year-end tax picture, especially where accruals and provisions affect reporting.

- Final accounts students need it because deferred tax often appears in year-end journals and note disclosures.

- Business analysts and data analysts use the logic behind IAS 12 when reconciling finance data, building reporting packs, or checking why the effective tax rate differs from the headline rate.

Why employers value this skill

Knowing IAS 12 tells an employer you can do more than process entries. It shows you can explain why a number appears in the accounts, challenge a mismatch, and support year-end reporting.

Practical rule: If you can bridge the gap between accounting records and tax impact, you become more useful during month-end, year-end, and audit season.

That matters in UK finance teams where staff often move between bookkeeping, management accounts, final accounts preparation, and systems-based reporting. Teams also rely more on automation and structured workflows, which is why some trainees find it useful to understand how Matil's financial services solutions fit into document-heavy finance processes such as extracting data from tax papers, reconciliations, and supporting schedules.

The career benefit

IAS 12 gives you a sharper answer when someone asks, “Why doesn't the tax charge equal profit times the tax rate?” If you can answer that clearly, you sound job-ready.

That's valuable whether you want to become a stronger accounts assistant, move into final accounts, or support finance teams as a business or data analyst. In UK practice and industry, people notice the trainee who can explain the logic behind the tax line instead of just copying it forward.

What Is IAS 12 Income Taxes

IAS 12 is the accounting standard that tells companies how to deal with the tax consequences of transactions in their financial statements. The key idea is that tax should be reflected in the same broad reporting picture as the transaction that created it, not only when cash is finally paid.

That's why IAS 12 isn't just about the corporation tax bill. It's also about future tax effects that already exist because of events recorded in the accounts.

The two terms you must know

To understand IAS 12, you need to get comfortable with two phrases.

Carrying amount means the value of an asset or liability in the financial statements.

Tax base means the value of that same asset or liability for tax purposes.

If those two figures differ, that difference often creates deferred tax.

A simple analogy

Think about a company car or a machine used in the business. In the accounts, the asset is reduced over time through depreciation. For tax, HMRC may allow relief under capital allowances on a different pattern. So the asset has one value in the accounts and another value for tax.

That gap is what IAS 12 cares about.

A useful way to think about it is this. IAS 12 is a timing map. It tracks when accounting recognises something and when tax recognises it. If the timing differs, the standard asks whether there's a future tax consequence that needs to be shown now.

The core rule behind the standard

The central principle is set out clearly in the IFRS summary of IAS 12 Income Taxes. IAS 12 mandates that entities recognise a deferred tax liability (or asset, subject to specified conditions) for all temporary differences arising between the carrying amount of assets or liabilities in financial statements and their respective tax bases, excluding temporary differences on initial recognition where there is no impact on taxable profit at that time.

That sentence is dense, so break it down like this:

- Compare the accounting value with the tax value.

- Identify the temporary difference.

- Decide whether that difference means more tax later or less tax later.

- Record the deferred tax effect if the standard requires it.

IAS 12 isn't asking, “What tax did we pay?” It's asking, “What tax consequences already exist because of what we've recorded?”

Why this matters beyond pure accounting

If you're studying business analysis or data analysis, this logic is useful because it teaches you to reconcile two valid datasets that follow different rules. One dataset is prepared for financial reporting. The other reflects tax treatment. Your job is often to explain the variance, not just spot it.

That's why International Accounting Standards 12 is a strong training topic for UK learners who want practical finance credibility.

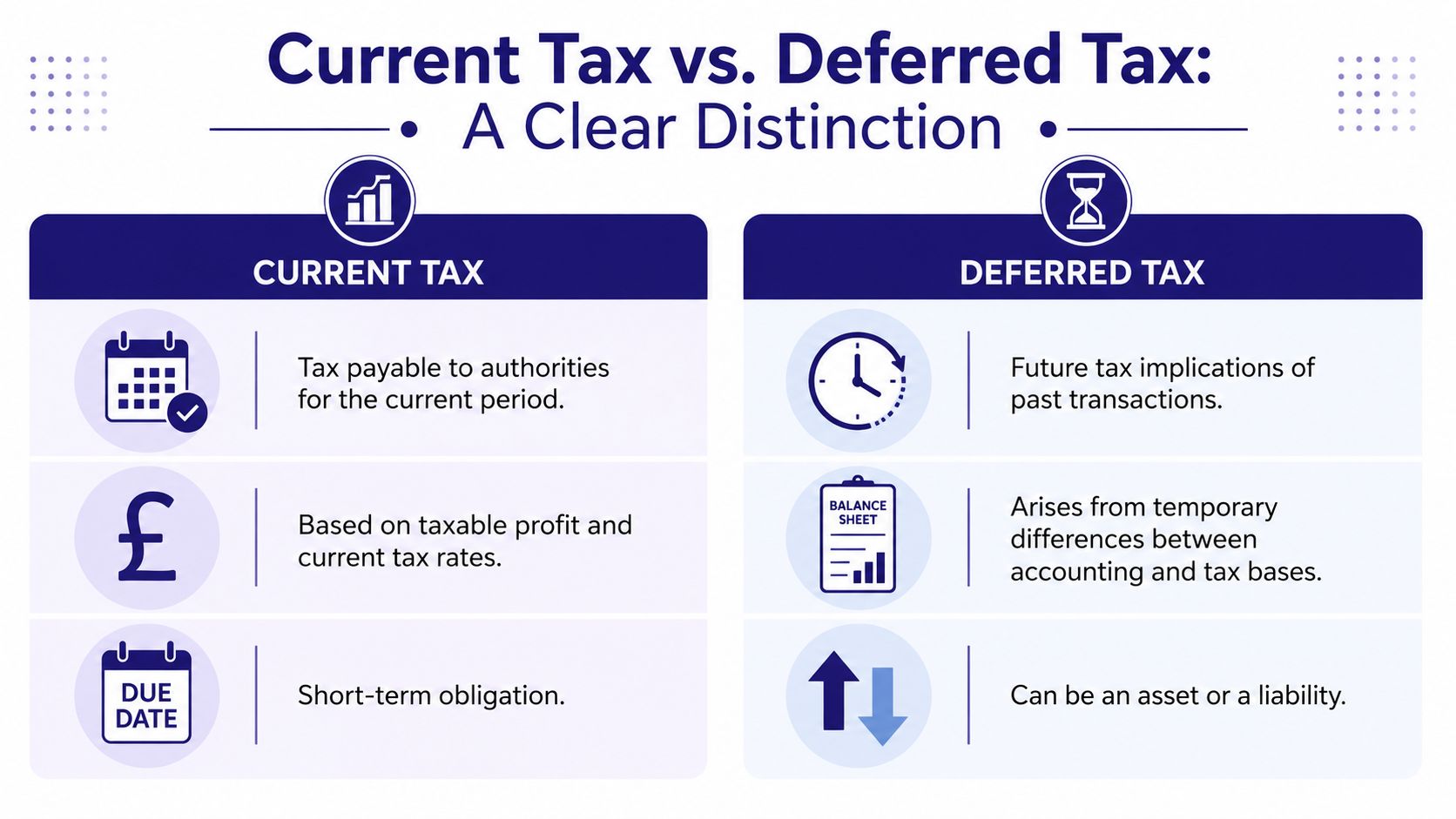

The Core Distinction Current Tax vs Deferred Tax

Most trainees find IAS 12 much easier once they separate current tax from deferred tax. They are linked, but they are not the same thing.

Current tax

Current tax is the amount payable in respect of the current period's taxable profit. This is the nearer-term tax bill. It's based on tax rules, tax adjustments, and the period's taxable result.

If you work in an accounts team, current tax is the part that feels closest to the corporation tax return. It connects to what the business owes HMRC for the period.

Deferred tax

Deferred tax is different. It deals with the future tax effects of transactions that have already happened.

That future effect usually comes from timing differences between accounting treatment and tax treatment. The transaction is already in the books. The tax effect hasn't fully run through yet.

A side-by-side view

| Feature | Current tax | Deferred tax |

|---|---|---|

| Main focus | Tax payable for the current period | Future tax effect of existing differences |

| Based on | Taxable profit | Temporary differences |

| Where trainees see it | Tax computation, provision for corporation tax | Fixed assets, provisions, losses, year-end adjustments |

| Time horizon | Near term | Future periods |

How to picture the difference

Use this mental shortcut.

- Current tax is the bill for this year.

- Deferred tax liability is like an IOU for tax likely to be paid in a later period because of a current difference.

- Deferred tax asset is like tax relief that may reduce a later bill, provided the recognition conditions are met.

That distinction helps when reviewing final accounts. A business might have a modest current tax charge but still show a deferred tax movement because asset values, provisions, or losses have changed.

Why trainees get confused

The confusion usually comes from expecting one tax number to do everything. In published accounts, the tax line often includes both current tax and deferred tax. So the total tax expense in profit or loss may not match the corporation tax payment pattern.

That's normal.

Career tip: When reviewing a tax note, ask two separate questions. What is payable for the period? What future tax effect has been recognised because of timing differences?

Practical relevance in UK job roles

In a bookkeeping role, you might not calculate deferred tax every week, but you still need to recognise the entries that create it. In an accounts assistant role, you may help prepare fixed asset schedules, accruals, or provisions that feed directly into deferred tax calculations. In a final accounts role, you'll often need to post the year-end deferred tax journal and understand its effect on both profit and the statement of financial position.

For business analysts and data analysts in finance teams, this split matters because tax reporting packs often separate current and deferred movements. If your dashboard only shows one combined line, the explanation can become misleading.

Recognising and Measuring Deferred Tax

Once you know what deferred tax is, the next step is calculation. The workflow is more manageable than many trainees expect. Start with the balance sheet item, compare its accounting value with its tax value, then ask what that difference means for future tax.

Taxable and deductible temporary differences

A taxable temporary difference usually creates a deferred tax liability. That means the company is likely to pay more tax later when the difference reverses.

A deductible temporary difference usually creates a deferred tax asset. That means the company may get tax relief later when the difference reverses.

A common UK example of a taxable temporary difference is when capital allowances have reduced the tax base of an asset faster than depreciation has reduced the carrying amount. A common deductible temporary difference is a provision recognised in the accounts before it becomes tax-deductible.

The prudence point for deferred tax assets

Trainees often think every deductible difference automatically becomes an asset. It doesn't. You still need enough confidence that future taxable profits will be available to use that benefit.

So the question isn't only, “Is there a deductible temporary difference?” It's also, “Is it appropriate to recognise the related deferred tax asset?”

That judgement matters in real jobs. If you work on final accounts or support an audit file, you'll often need evidence for why management believes the asset should be recognised.

Measuring deferred tax in the UK

Measurement is where UK-specific knowledge becomes important. According to the ICAEW IAS 12 tracker, under UK-adopted IAS 12, deferred tax assets and liabilities are measured using the tax rates expected to apply when the liability is settled or the asset is realised, based on tax laws enacted or substantively enacted at the reporting date. For the UK's 2024 fiscal year, the standard corporation tax rate of 25% for profits over £250,000 is the benchmark rate used in UK financial statements for deferred tax calculations.

That rule matters because deferred tax is not measured using a random estimate or the cash tax paid this year. It is measured using the rate expected to apply when the timing difference reverses, based on enacted or substantively enacted law at the reporting date.

A useful check when you're learning

Ask these questions in order:

- What is the carrying amount?

- What is the tax base?

- What is the temporary difference?

- Is it taxable or deductible?

- What tax rate should apply when it reverses?

- If it's an asset, is recognition supportable?

If you want to build stronger confidence with year-end judgement areas, it also helps to understand where IAS 12 sits alongside other standards on changes in estimates and accounting treatment, such as IAS 8 training guidance.

A short visual explainer can also help fix the logic before you try the journal entries:

IAS 12 in Action Practical Examples and Journal Entries

Theory only sticks when you can post the entries. These examples use simple numbers to show the mechanics. The figures are illustrations for training, not cited market data.

Example one fixed asset and capital allowances

A company buys a machine for £100,000. In the accounts, it depreciates the machine on a straight-line basis over five years, so the annual depreciation charge is £20,000. For tax, suppose capital allowances are claimed faster than depreciation in the early years.

If, at the year end, the machine's carrying amount is higher than its tax base, there is a taxable temporary difference. That usually creates a deferred tax liability because the business has already had more tax relief than accounting depreciation would suggest, and that timing benefit will unwind later.

Example deferred tax on fixed asset

| Year | Carrying Amount | Tax Base | Temporary Difference | Deferred Tax Liability @ 25% |

|---|---|---|---|---|

| 1 | £80,000 | £60,000 | £20,000 | £5,000 |

| 2 | £60,000 | £35,000 | £25,000 | £6,250 |

| 3 | £40,000 | £20,000 | £20,000 | £5,000 |

| 4 | £20,000 | £10,000 | £10,000 | £2,500 |

| 5 | £0 | £0 | £0 | £0 |

The pattern shows what trainees need to notice. Deferred tax is not static. It moves as the timing difference changes.

If the liability at the end of Year 1 is £5,000, the basic journal is:

- Debit Tax expense

- Credit Deferred tax liability

If the liability increases by Year 2 to £6,250, you post the movement of £1,250, not the whole balance again:

- Debit Tax expense £1,250

- Credit Deferred tax liability £1,250

Why this matters in final accounts

This is exactly the kind of adjustment that appears at year end. The fixed asset note may look fine. The depreciation charge may look fine. The corporation tax computation may also look fine. But if you miss deferred tax, the statement of financial position and tax note won't be complete.

Check the fixed asset register, depreciation schedule, and tax written down value working together. If those three don't tell the same timing story, deferred tax is often sitting in the gap.

Example two warranty provision

Now take a different item. A business recognises a warranty provision of £12,000 in the accounts because it expects future claims. For tax, suppose the cost is only deductible when the company pays the claims.

Here, the liability appears in the accounts before tax relief is available. That creates a deductible temporary difference, which may lead to a deferred tax asset if recognition is appropriate.

At 25%, the potential deferred tax asset is £3,000.

The journal would be:

- Debit Deferred tax asset £3,000

- Credit Tax expense £3,000

This credit to tax expense reduces the overall tax charge in profit or loss because it reflects tax relief expected in a future period.

What an accounts assistant should take from this

Don't memorise only the journal. Understand the direction.

- If the company is likely to pay more tax later because of a temporary difference, think deferred tax liability.

- If the company is likely to get relief later, think deferred tax asset, subject to recognition conditions.

- Always compare the closing deferred tax balance with the opening balance, then post the movement.

That approach works whether you're using Excel, Sage, Xero, or a year-end accounts pack prepared for review.

UK Disclosures and Common Pitfalls for Trainees

Getting the number right is only half the job. You also need to present it clearly.

One of the most useful IAS 12 disclosures in UK accounts is the tax reconciliation. This note explains why the total tax expense differs from a simple profit multiplied by the standard rate. It turns a confusing tax line into a story.

The tax reconciliation note

Under UK-adopted IAS 12, entities must disclose a reconciliation of total income tax expense to the product of accounting profit multiplied by the applicable UK tax rate. The FCT Training overview of IAS 12 notes that this disclosure reveals the effect of items such as non-taxable profits and non-deductible expenses, and it also states that many FTSE 100 firms averaged an effective tax rate of 18.7% in 2024 because of factors such as offshore tax credits and loss utilisations.

For a trainee, the lesson is practical. The tax note isn't boilerplate. It explains why the tax charge moved away from the headline rate.

Common mistakes trainees make

- Mixing up current and deferred tax: One is the present-period tax bill. The other reflects future tax effects.

- Forgetting the recognition test for deferred tax assets: A deductible difference doesn't automatically mean recognition.

- Posting the closing balance twice: You book the movement in deferred tax, not the full closing figure each year.

- Ignoring note disclosures: Strong workings can still lead to weak accounts if the reconciliation note is incomplete.

- Treating all tax differences as permanent: Some never reverse. Others do. IAS 12 focuses heavily on temporary differences.

A UK point that often catches people out

Trainees also get stuck on when to use a tax rate if legislation is not fully enacted. The issue matters because UK reporting relies on enacted or substantively enacted law at the reporting date, and practice can become inconsistent where transactions sit outside clearly enacted law.

The IAS Plus summary on IAS 12 highlights this implementation challenge and refers to late 2025 UK Corporate Reporting Lab data showing 45% of UK-based companies reported diversity in accounting for deferred tax on transactions outside the scope of enacted law. That's a reminder to trainees to check the legal status of tax changes before assuming a rate.

Pillar Two and the temporary exception

A newer area of confusion involves the OECD Pillar Two rules. The IAS Plus update on the IASB amendments states that the IASB issued amendments to IAS 12 on 27 May 2023, introducing a temporary exception that prevents entities from recognising or disclosing deferred tax assets and liabilities related to OECD Pillar Two income taxes. The same update says the rules implement a global minimum corporate tax rate of 15% for large multinational companies, the exception applies immediately and retrospectively, disclosure requirements are mandatory for annual reporting periods beginning on or after 1 January 2023, and UK entities are not required to disclose Pillar Two exposure for interim periods ending on or before 31 December 2023.

That matters if you work with large groups or multinational reporting packs. If you don't know this exception exists, you can easily apply the normal deferred tax logic where the amendment says not to.

Large-group tax reporting now needs two habits at once. Strong knowledge of the usual IAS 12 rules, and enough awareness to spot when the Pillar Two exception changes the answer.

If you're studying corporation tax alongside financial reporting, a practical companion is this CT600 guide for UK trainees, because it helps connect the reporting side of tax with the tax return side.

Your Next Steps in Mastering Accountancy

IAS 12 is one of those topics that marks a real step up in your development. Once you understand it, you read financial statements differently. You stop seeing tax as a single plug figure and start seeing the underlying logic behind fixed assets, provisions, reconciliations, and year-end adjustments.

That helps across several UK pathways. It strengthens your work in bookkeeping and VAT, supports advanced payroll learners who want broader finance knowledge, sharpens accounts assistant skills, and gives final accounts students a more complete grasp of year-end reporting. It also helps business analysts and data analysts who need to explain finance variances with confidence.

A good next move is deliberate practice. Build a tax reconciliation. Rework a fixed asset deferred tax example. Review a provision and decide whether it creates a deferred tax asset. If you enjoy structured exam-style learning, you might also like Cramberry's guide to CPA exam success, because its study discipline ideas translate well to technical accounting topics.

For a broader grounding in UK taxation topics that support IAS 12, use these courses on taxation as a starting point.

If you want hands-on support with final accounts, accounts assistant skills, bookkeeping software, taxation, or job-focused finance training, Professional Careers Training offers flexible learning with practical mentoring designed for UK career starters and career changers.