You've got the degree. You've done the exams. You know what accruals, control accounts, variance analysis, and ratio interpretation mean. Then you open job boards...

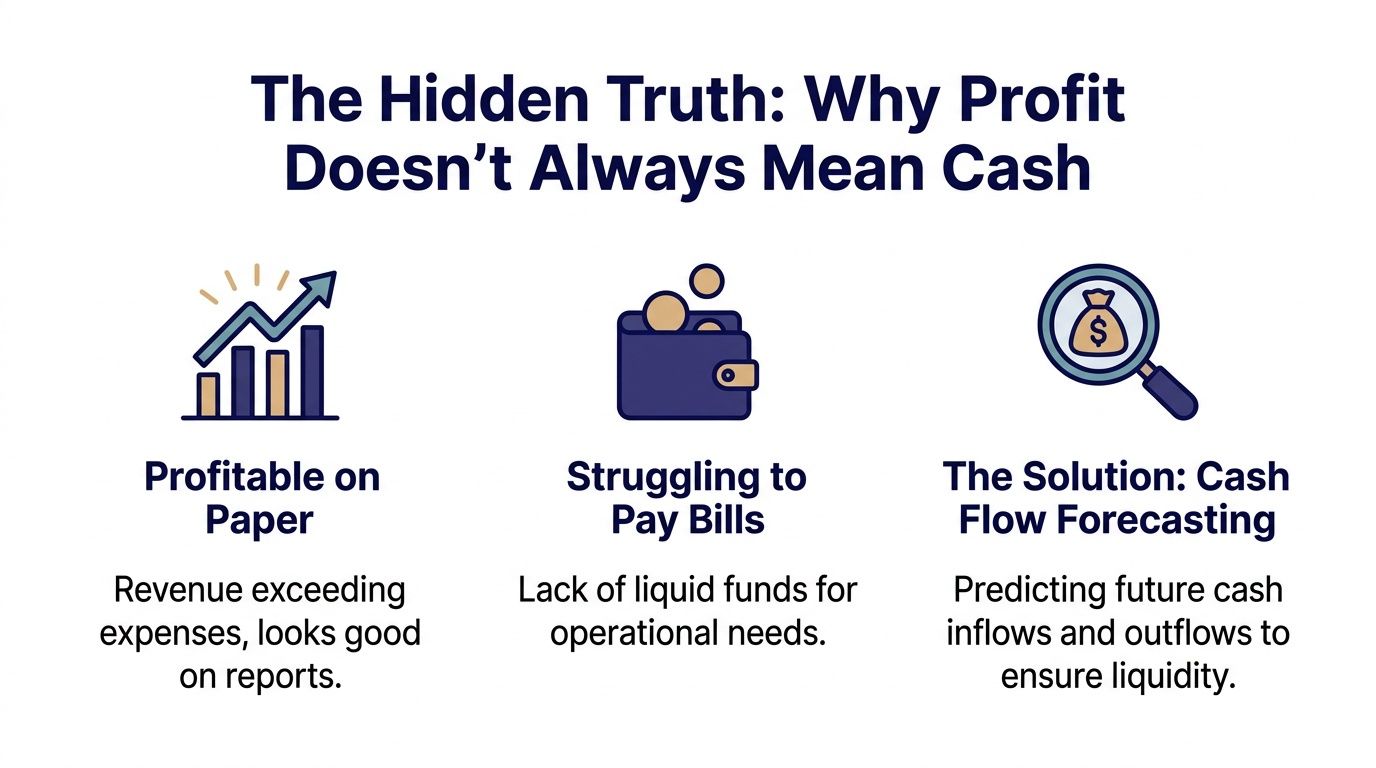

A business can post sales, show a profit in its accounts, and still struggle to pay wages, rent, suppliers, or VAT on time. That gap catches many trainees out at first, because profit is an accounting result, while cash is what keeps the doors open.

That's why cash flow forecasting matters so much in practice. In the UK, 82% of businesses that failed in 2023 did so specifically because of cash flow problems (Outbooks on UK startup cash flow forecasting). For a trainee aiming for roles such as Accounts Assistant, Bookkeeper, Business Analyst, or Data Analyst, that changes the subject completely. This isn't just another finance topic. It's a hiring signal. Employers want people who can look ahead, spot pressure early, and turn raw figures into action.

Why Cash Flow Forecasting Is a Critical Skill

A simple way to understand cash flow forecasting is to compare it with managing your own bank account.

You might know your salary is due at month end. You might also know your rent, travel costs, council tax, and groceries are due before then. If the timing doesn't line up, you can run short even if your income for the month is higher than your spending overall. A business works in the same way, just with more moving parts, more risk, and more people affected by mistakes.

Profit isn't the same as cash

A sale recorded today doesn't always mean cash received today. The invoice may not be paid for weeks. Meanwhile, payroll, rent, software subscriptions, supplier bills, and tax liabilities still need paying.

That's why a business can look healthy on a report and still face immediate pressure in its bank account. New trainees often focus on turnover and profit first. Employers need you to go one level deeper and ask, “When does the money arrive, and when does it leave?”

Practical rule: If you can explain the difference between profit and cash in plain English, you're already thinking like a useful finance professional.

Why employers value this skill

Cash flow forecasting sits across several UK job paths:

- Bookkeeping and VAT roles need accurate recording of sales, purchases, VAT timing, and payment patterns.

- Accounts Assistant roles often involve credit control, supplier payments, reconciliations, and weekly reporting.

- Advanced payroll work links directly to one of the largest regular cash outflows in many businesses.

- Final accounts training helps you understand the wider financial picture behind the cash movements.

- Business Analyst and Data Analyst roles use forecast data to support planning, reporting, and decisions.

The strongest candidates don't just process transactions. They understand what those transactions mean next week, next month, and next quarter.

How this translates into employability

When a hiring manager sees cash flow forecasting on your CV, they usually read it as evidence of several practical abilities:

- Commercial awareness: You understand that timing matters, not just totals.

- Attention to detail: You can track due dates, payment lags, and tax obligations.

- Software confidence: You can work in tools like Excel, Xero, or Sage without losing the logic behind the numbers.

- Decision support: You can help managers act before a cash issue becomes a crisis.

That's why this skill helps candidates stand out in entry-level and progression roles alike. It shows you can do more than post data. You can interpret it.

Core Forecasting Methodologies Explained

Two methods appear again and again in cash flow forecasting. If you understand when each one is used, you'll sound far more credible in interviews and team discussions.

One is practical and immediate. The other is broader and more analytical.

The direct method

The direct method tracks expected cash in and cash out. Picture checking your bank app and listing what money is likely to come in, then listing what bills are due to leave.

This method suits short-term control. It's the one most trainees meet first because it's intuitive and closely linked to bookkeeping records, sales invoices, purchase invoices, payroll dates, and bank activity.

A strong UK forecast often uses a rolling 13-week timeframe combined with driver-based modelling, with daily management of data hygiene and real-time monitoring of receivables and payables against actual bank statements (Julian Hobbs on UK cash flow forecasting). That's highly relevant if you're aiming for Accounts Assistant or Bookkeeper work, where the quality of day-to-day data drives the usefulness of the forecast.

The indirect method

The indirect method starts from profit-related figures and adjusts for non-cash items and working capital movements. A simple way to think about it is this: instead of checking what's in your wallet, you start from your payslip and adjust to estimate what cash position may result.

This method is more common in longer-range planning and analysis. It becomes more useful when you move into final accounts work, management reporting, or Business Analyst tasks where you need to connect the profit view with the cash view.

A trainee who understands both methods can move more easily between transaction processing, reporting, and analysis.

Direct and indirect compared

| Aspect | Direct Method | Indirect Method |

|---|---|---|

| Starting point | Expected cash receipts and payments | Profit or income-based figures |

| Best use | Short-term liquidity planning | Longer-term analysis and planning |

| Typical users | Bookkeepers, Accounts Assistants, finance officers | Final accounts trainees, Business Analysts |

| Main data source | Bank activity, receivables, payables, payroll, tax dates | Financial statements and adjusted accounting data |

| Strength | Clear view of near-term cash timing | Useful for linking operating performance to cash generation |

| Common challenge | Needs frequent updates and clean detail | Can feel less intuitive for beginners |

If you want a wider read on methods and practical options, Allied Tax Advisors' forecasting strategies are a helpful reference point. For a beginner-friendly foundation on related planning concepts, financial forecasting basics also support the bigger picture.

Why trainees should care about both

You don't need to master every variation on day one. You do need to recognise which method fits the task in front of you.

If a manager asks, “Can we cover payroll and supplier payments this month?”, that points you towards a direct, short-term cash view. If they ask, “How does our trading plan affect our future cash position?”, you're closer to indirect thinking.

That distinction helps in interviews because it shows judgement, not just memory.

Building Your First Cash Flow Forecast Step by Step

Your first forecast doesn't need to be complicated. It needs to be clear, realistic, and updated regularly.

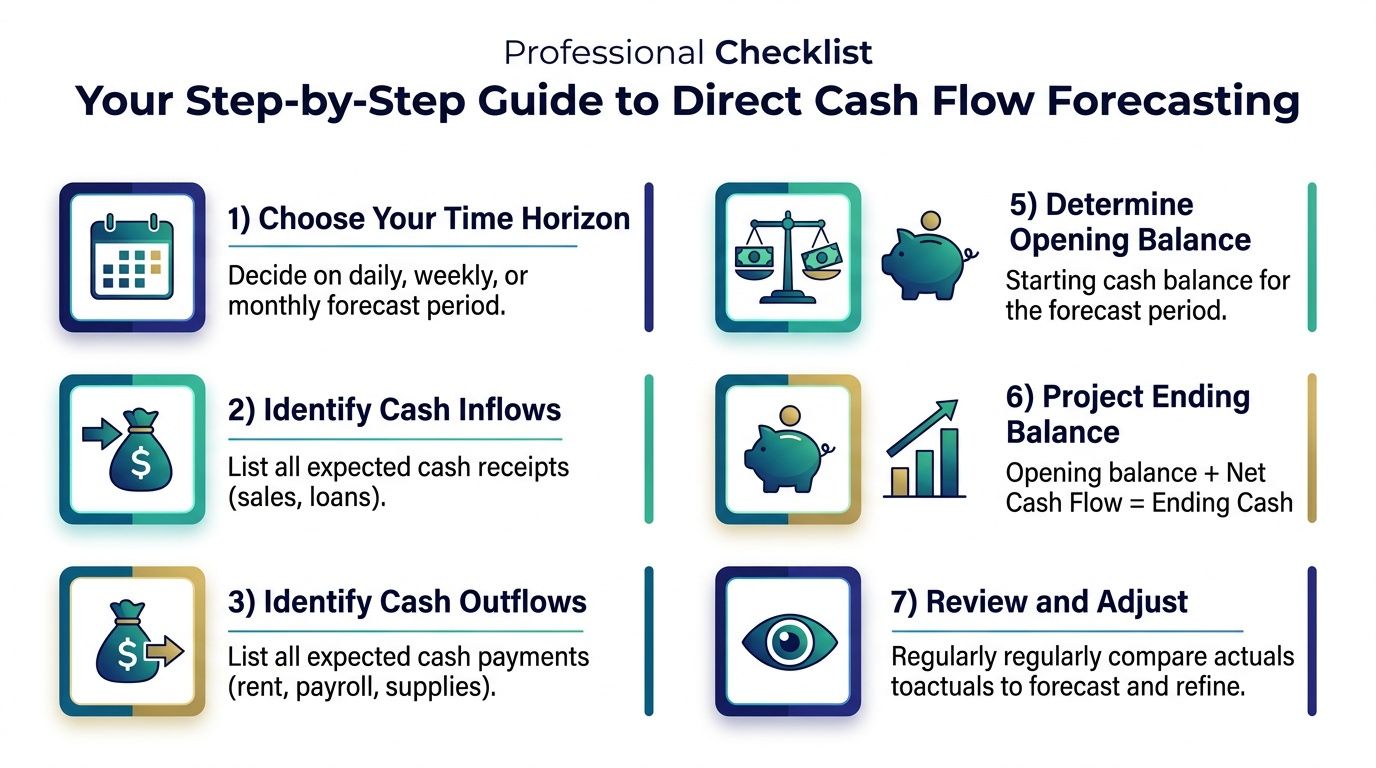

Start with a simple direct forecast. That's the best training ground because it teaches you how money moves through a business.

Pick a useful time horizon

For short-term control, a weekly format works well. Create columns for each week and rows for each type of cash movement.

Keep the layout simple:

- Opening bank balance

- Cash in

- Cash out

- Net movement

- Closing bank balance

That structure is easy to follow in Excel, Xero exports, or Sage reports.

List expected cash inflows

Many beginners make their first mistake by listing sales instead of cash receipts.

Include cash you expect to receive from items such as:

- Customer payments: Only include them when you expect the money to land.

- Loans or funding: Record them in the period the business will receive the funds.

- Other receipts: Refunds, rebates, or asset sale proceeds if relevant.

In the UK, small businesses wait an average of 29 days to be paid, so don't assume invoices turn into cash immediately (Xero's UK guide to cash flow forecasting). If you miss that timing issue, your forecast can look healthy on paper and fail in real life.

When you build a forecast, date the cash, not the invoice.

List expected cash outflows

Outflows are often easier to identify because they're more scheduled. Still, trainees often forget one-off and tax-related items.

Include items such as:

- Payroll and wages: Advanced payroll knowledge becomes commercially valuable.

- Rent and utilities: Usually fixed and easier to schedule.

- Supplier payments: Use agreed terms, not rough guesses.

- Software and subscriptions: Small recurring items can add up.

- Loan repayments: Include both timing and amount.

- VAT payments: These can create sharp pressure if ignored.

A key UK point is the VAT registration threshold of £90,000, which means VAT can become a major forecast item once taxable turnover crosses that level in a rolling 12-month period or is expected to exceed it in the next 30 days (Learn Direct's VAT UK guide). If you're training in bookkeeping and VAT, this is exactly the kind of detail employers expect you to notice.

For readers who want a visual structure to test their own model, this cash flow template for SMEs can help you compare layouts and line items.

Build the calculation

Once you have the inflows and outflows, the mechanics are straightforward:

- Start with the opening balance.

- Add total cash in.

- Subtract total cash out.

- Arrive at the closing balance.

- Carry that closing balance into the next period as the new opening balance.

That flow is simple, but don't let that simplicity fool you. Accuracy depends on assumptions, not formulas.

A short refresher on the statement itself helps here:

If you want to strengthen the accounting link behind the forecast, how to prepare a cash flow statement is useful background reading.

Apply realistic timing

A basic student exercise transforms into a useful business tool.

Check each line and ask:

- When does the invoice usually get paid?

- Are supplier terms fixed or negotiable?

- Does payroll leave at the end of the month or weekly?

- When is VAT due?

- Are there seasonal spikes or irregular costs?

A forecast is only as good as its timing assumptions. If your assumptions are lazy, your forecast will be tidy but misleading.

Forecasting with Professional Tools

At trainee level, tools matter because employers often shortlist candidates by software familiarity. But the software only helps if you understand the thinking underneath it.

A weak forecast in Xero is still a weak forecast. A strong one in Excel is still valuable.

Excel is still the training ground

Excel remains one of the best places to learn forecasting logic. It forces you to build the structure yourself, check your formulas, and think about assumptions line by line.

That's especially useful if you're moving towards Data Analyst or Business Analyst work. In those roles, people often need to adapt models, clean data, sort timing issues, and explain variance. Excel teaches that discipline well.

Good Excel habits for forecasting include:

- Clear tabs: Separate assumptions, input data, and forecast output.

- Simple formulas: Avoid building a model that only you can understand.

- Consistent date structure: Weekly columns should align cleanly.

- Variance columns: Compare forecast against actual once the period ends.

Xero, Sage, and QuickBooks in real workplaces

Accounting software changes the speed of the work. Xero, Sage, and QuickBooks can pull live accounting data into reports and help you monitor receivables, payables, and bank balances more efficiently.

For entry-level UK roles, employers often look for candidates who can move comfortably between:

- Xero for cloud bookkeeping and reporting

- Sage for day-to-day finance operations in many UK businesses

- QuickBooks where smaller firms or specific employers use that platform

- Excel for custom analysis beyond the standard software output

The key point is this. Software can automate data collection, but it doesn't replace judgement. You still need to decide whether an expected receipt is realistic, whether a payment should move to another week, or whether a large tax outflow has been omitted.

Software speeds up the mechanics. Skill shows in the assumptions you choose and the questions you ask.

What to put on your CV

When software training links to forecasting work, your CV becomes stronger because it shows application, not just attendance.

Useful CV phrasing often sounds like this:

- Built and maintained weekly cash flow forecasts in Excel using live sales and purchase ledger data

- Updated receivables and payables in Xero to support short-term cash planning

- Used Sage reports to review supplier payment timing and expected outflows

- Produced variance commentary between forecast and actual cash movements

That's more convincing than listing software names without context.

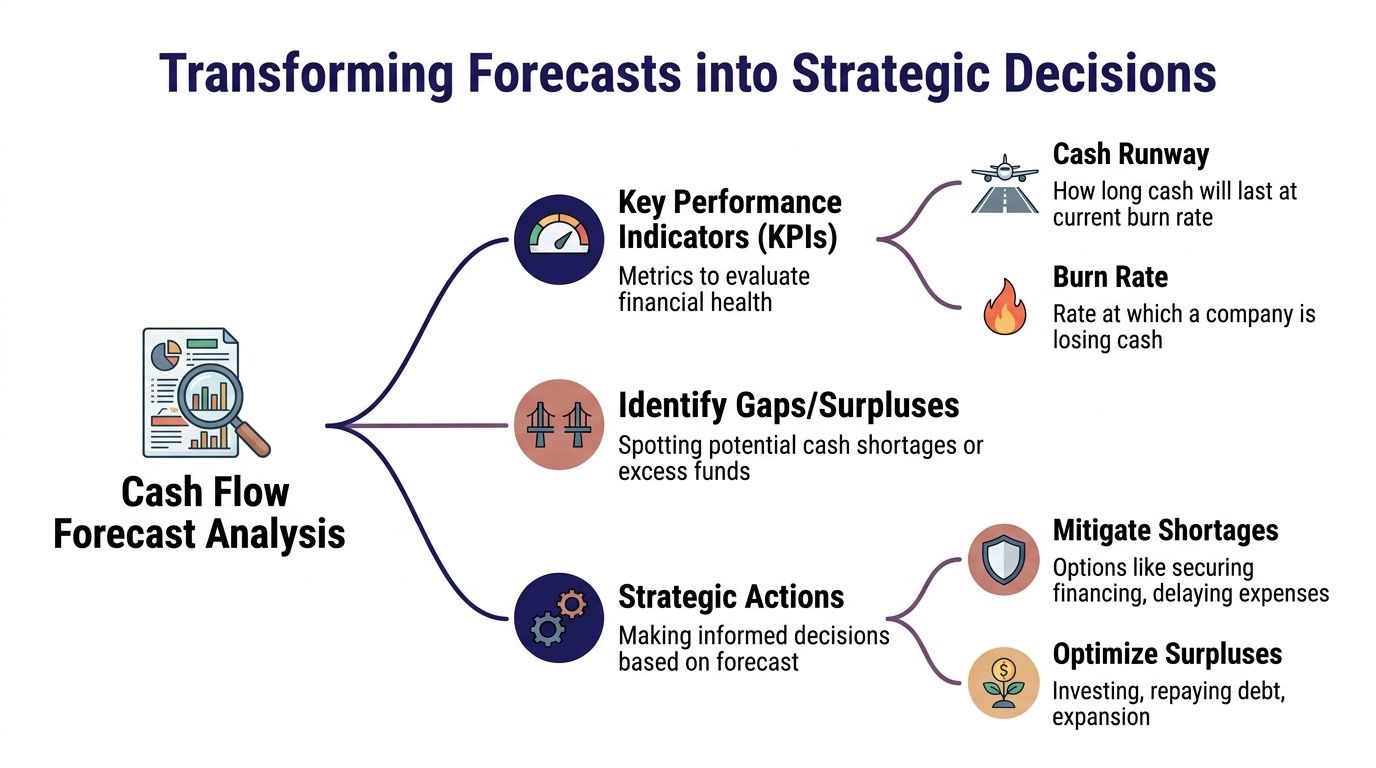

Analysing Your Forecast and Making Decisions

A forecast becomes valuable when it changes a decision.

If all you do is prepare the sheet and file it away, you've done half the job. The second half is reading the pattern, judging the risk, and helping someone decide what to do next.

What the forecast is telling you

Start with the closing balances across each future period. If one week dips sharply, ask why. If several weeks show pressure, look for the root cause.

Common issues include:

- Receipts arriving later than expected

- Payroll and rent landing in the same period

- VAT or tax dates creating a sudden drop

- Supplier payments clustering together

- Sales looking strong, but cash collection lagging

This kind of review is where Accounts Assistant work starts to blend into analyst work. You're no longer just recording events. You're interpreting them.

Use KPIs carefully

Teams often discuss cash runway and burn rate when reviewing forecasts. Even if a business doesn't use those exact labels, the ideas are practical.

- Cash runway asks how long current cash may last if conditions continue.

- Burn rate looks at how quickly cash is being used up.

For a trainee, the key skill isn't using jargon. It's being able to say, in plain language, whether the current pattern is sustainable and what may need to change.

A simple decision example

Suppose a small company's forecast shows a tight period ahead because customer receipts are expected later than usual while payroll and VAT fall close together.

That forecast can lead to several decisions:

- Delay non-essential spending

- Chase overdue customer payments earlier

- Review supplier payment timing

- Pause hiring

- Consider short-term funding support

None of those decisions come from the historic accounts alone. They come from the forward view.

A forecast is a management tool, not just a finance document.

Scenario thinking improves your value

Good analysts don't stop at one version of the future. They test assumptions.

You might model questions such as:

- What if customer payments slip further?

- What if a major cost arrives earlier?

- What if sales receipts improve because credit control tightens?

This approach matters for Business Analyst and Data Analyst roles because it shows you can move from reporting to decision support. You're helping a business prepare, not just react.

For broader financial context around liquidity and short-term operational funding, working capital management explained supports the link between forecasting and day-to-day business decisions.

Common Forecasting Mistakes to Avoid

Most forecasting errors aren't caused by complex formulas. They come from poor assumptions, missing detail, or weak habits.

That's good news for trainees, because these problems can be fixed early.

Confusing profit with cash

What not to do: Assume a profitable month means a safe cash position.

What to do instead: Check when cash is due in and out. A profitable business can still be short of liquid funds if customers pay late and bills are due now.

Being too optimistic about receipts

What not to do: Enter expected customer payments according to ideal terms.

What to do instead: Base timing on actual payment behaviour where possible. If a customer regularly pays later than agreed, your forecast should reflect that reality.

Forgetting tax and one-off costs

What not to do: Build a forecast around wages, rent, and suppliers only.

What to do instead: Include VAT, Corporation Tax, loan repayments, annual software renewals, insurance, and irregular costs that can hit a single period hard.

Failing to update the forecast

What not to do: Prepare the file once, then leave it untouched.

What to do instead: Replace forecasted figures with actuals as periods pass, then roll the view forward. A forecast that isn't refreshed loses decision value quickly.

Missing granular data across the business

This is a more advanced mistake, but it matters if you want to sound stronger than the average trainee.

A significant forecasting weakness is a lack of granularity. Only one-third of UK companies successfully integrate subsidiaries into cash forecasting, and 37% of UK CFOs operate with unreliable forecasts because this granular engagement is absent (Treasury Management on why forecasts fail). In practice, that means forecasts often miss what's happening in separate entities, departments, or local operations.

If you work in a multi-entity business, don't settle for one top-level figure. Ask:

- Which subsidiary owns this cash movement?

- Are credit terms standardised across entities?

- Do local teams submit consistent data?

That line of thinking is particularly useful for future Business Analysts, finance analysts, and management accountants.

Showcasing Your Forecasting Skills to Employers

You can learn cash flow forecasting well and still undersell it. Many candidates do. They describe tasks too vaguely, or they list software without showing what they did.

Employers respond better to evidence of applied skill.

Stronger CV wording

Instead of writing “knowledge of forecasting”, use practical statements such as:

- Prepared and updated a rolling cash flow forecast using Excel

- Reviewed customer receipt timing and supplier due dates to improve forecast accuracy

- Supported VAT and payroll planning by mapping expected cash outflows

- Used Xero and Sage reports to monitor receivables, payables, and bank activity

- Produced commentary on forecast versus actual cash movement for management review

These phrases connect the skill to real work, which is what hiring managers want.

Build a portfolio project

If you haven't done this in a paid role yet, create your own sample project.

Use a fictional UK business and build:

- A weekly forecast

- Assumptions for customer payment timing

- Key outflows including payroll, rent, and VAT

- A short note explaining risks and decisions

That gives you something concrete to discuss at interview.

Talk about the skill clearly in interviews

A good answer to “How would you approach forecasting our cash flow?” should sound practical.

You might say that you'd start with the opening bank balance, map expected receipts and payments by timing, include known obligations such as payroll and tax, compare forecast against actuals regularly, and adjust assumptions where payment patterns differ from plan.

If you've completed relevant training, don't hide it. Show it professionally online as well. This guide to displaying your professional certificates on LinkedIn is useful if you want recruiters to see your bookkeeping, VAT, payroll, Xero, Sage, Business Analyst, or Data Analyst learning more clearly.

Professional careers in finance and analysis are built on skills employers can recognise quickly. Professional Careers Training helps trainees build those skills through flexible accountancy and analytics training, 1-to-1 support from ACCA qualified Chartered Accountants and CPD-approved trainers, certification in Sage, Xero, and QuickBooks, plus career coaching, CV preparation, LinkedIn optimisation, and job search support for the UK market.